The Basics of Personal Finance

By

By

Despite what you learned in high school economics class, personal finance doesn’t have to be super complicated. (Or maybe you’re a student taking Foundations in Personal Finance right now—lucky you!)

You don’t need to get a finance degree or have some crazy investing strategy to manage your money well. But there are some basics of personal finance that everyone should know. Let’s dive into them!

Key Takeaways

- Personal finance is all the decisions you make to earn, budget, save, spend and give your money.

- Personal finance is 20% head knowledge and 80% behavior.

- The basics of personal finance include living on less than you make, getting and staying out of debt, planning for the future, and protecting yourself with insurance.

What Is Personal Finance?

Personal finance is all the decisions you make to earn, budget, save, spend and give your money. In other words, it’s what you choose to do with your money.

Personal finance is important because how you manage your money affects how you manage your life. From earning your first paycheck to investing for retirement, what you do with your money shapes your present and your future.

If you want to reach your financial goals, you need to get your personal finances in order. Because you’ll either manage your money or it will manage you.

The good news is, anyone can learn how to be better with their money. In fact, personal finance is only 20% head knowledge and 80% behavior. That means the hard part isn’t knowing how to manage your money—it’s actually doing it.

The Basics of Personal Finance

While personal finance is . . . well, personal, there are some fundamental principles that apply to everyone—no matter your age or stage of life. Here are eight basics of personal finance that’ll help you make the most of your money.

1. Do a Monthly Budget

2. Live on Less Than You Make

3. Save an Emergency Fund

4. Get Out and Stay Out of Debt

5. Plan for the Future

6. Have Insurance and a Will

7. Pay Your Taxes

8. Build Wealth, Not Your Credit Score

1. Do a Monthly Budget

The first basic of personal finance is to create and stick to a monthly budget. Budgeting is simply making a plan for your money. It’s the foundational habit you build all other money habits on. Because without a good game plan, you can’t get where you want to be with your finances. Start telling your money where to go. Do a monthly budget.

There are a lot of ways to budget, but the best method is a zero-based budget, where your income minus your expenses equals zero. This doesn’t mean you’re spending all your money every month. It means you give every single dollar a job to do inside your budget.

Here’s how you create a zero-based budget:

- List your monthly income.

- List your expenses (including all planned giving, saving and spending).

- Subtract your expenses from your income (which should equal zero).

- Track your expenses all month long.

- Make a new budget before the next month begins.

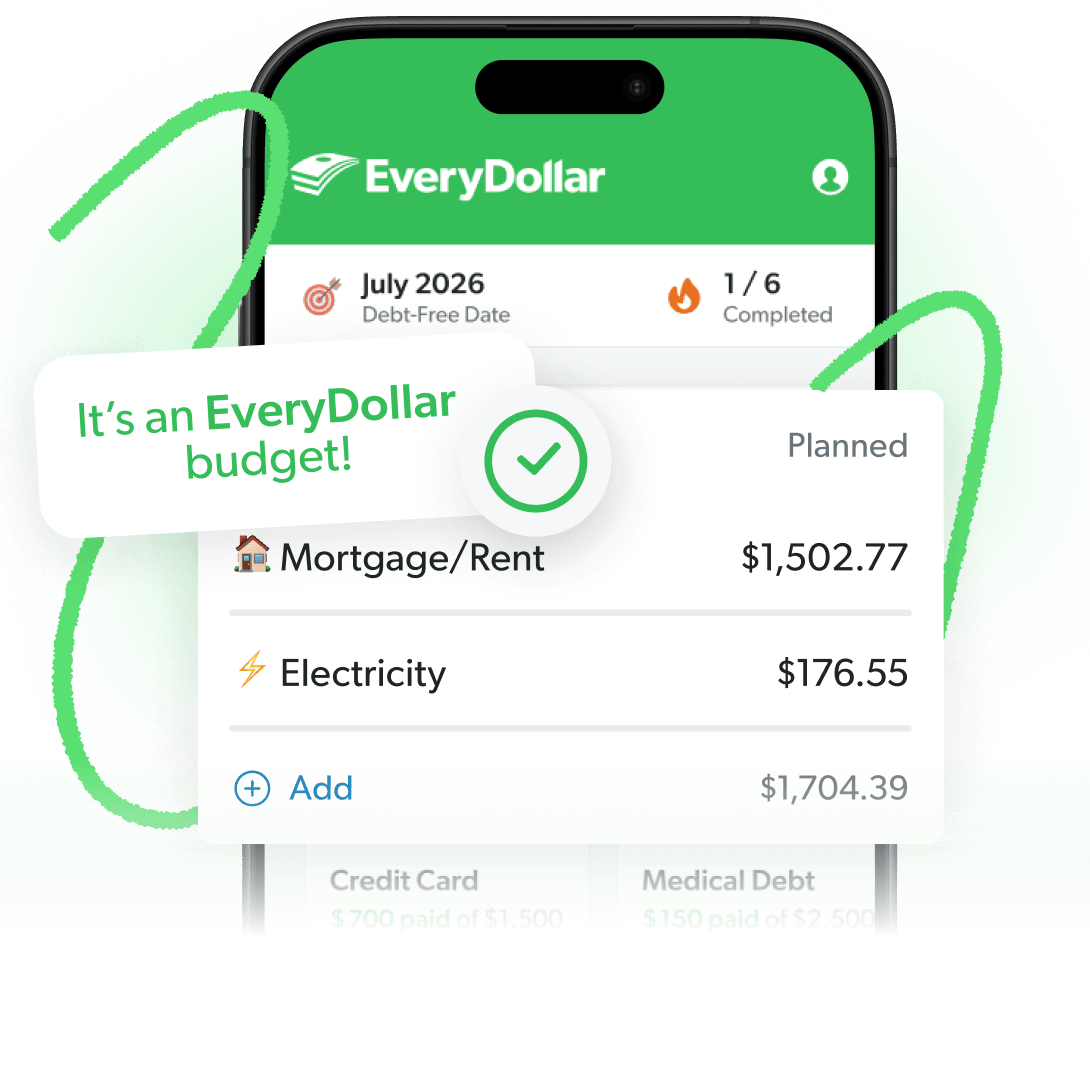

The easiest way to create and stick to a monthly budget is with the EveryDollar budget app. But if you’re not sure where to start, plug your numbers into our budget calculator.

Find Margin You Didn’t Know You Had With EveryDollar

The EveryDollar budgeting app helps you find extra money every month so you can beat debt, build wealth, and make progress. Every. Day.

2. Live on Less Than You Make

It’s easy to spend now and think later, especially if you rely on credit cards to get by. But pretty soon, you’re living paycheck to paycheck—or worse, falling deep into credit card debt.

An important basic of personal finance is to spend less than you make. So, if you realize you have more money going out than coming in every month, you need to adjust your spending. Make sure you cover your Four Walls (food, utilities, shelter and transportation) first and then any other essentials (like insurance or childcare). Then go through your budget and see where you can cut expenses and save money.

We know it’s hard to stick to a budget every month. But if you want to actually get ahead with your money, you’ve got to get your spending under control. And if you create more margin in your budget, you can create more margin in your life for what really matters to you!

3. Save an Emergency Fund

You need to save for a rainy day. Why? Because it rains. You get a flat tire, the HVAC goes out, you take a trip to the ER. Those are the moments an emergency fund comes in real handy.

First, you need a $1,000 starter fund—enough to cover those ankle-biter emergencies. You’ll want to save that $1,000 ASAP to keep you from going into debt (or more debt) if you get in a pinch. Then, you’ll need enough to cover 3–6 months of expenses in a fully funded emergency fund.

When you’ve got an emergency fund in place, you’ll be ready for whatever comes your way. If you or your spouse gets laid off or you need to take some unpaid time off to deal with a medical situation, you won’t have to worry about how to pay the bills on top of everything else. Phew, talk about peace of mind!

4. Get Out and Stay Out of Debt

Many people think of debt as a tool or something you just have as an adult. But here’s the truth about debt: It’s a weight that stresses you out and keeps you from getting ahead.

Your income is your greatest wealth-building tool. And when you pay off your debt, you take back your paycheck—and your life!

So, if you’ve got debt, the best way to pay it off is with the debt snowball method. Here’s how it works:

Step 1: List your debts from smallest to largest (regardless of interest rate).

Step 2: Make minimum payments on all your debts except the smallest debt.

Step 3: Throw as much extra money as you can on your smallest debt until it’s gone.

Step 4: Take what you were paying on your smallest debt and add that to your payment on the next-smallest debt until it’s gone too.

Step 5: Repeat until each debt is paid in full and you’re completely debt-free!

The debt snowball gives you quick wins that keep you motivated to pay off the rest of your debt. Trust us, we’ve seen millions of people use the debt snowball to pay off some serious amounts of debt—so this stuff works.

5. Plan for the Future

First, let’s talk about investing for retirement. We recommend investing 15% of your income for retirement once you’ve paid off all your debt and saved up that fully funded emergency fund we talked about.

When it comes to where to invest, remember this rule of thumb: match beats Roth beats traditional. If your employer offers an employer match on your 401(k) contributions, start there—that’s free money! Then, you can open a Roth IRA (which you fund with after-tax dollars) and max it out. And if you still haven’t hit 15% yet, just go back to your 401(k) and increase your contributions.

And as far as investment strategy goes, you want your money evenly spread across the four kinds of mutual funds: growth, growth and income, aggressive growth, and international. That way, you’re not investing your entire nest egg into one basket.

Once you’re investing for retirement, you should think about saving for your kids’ college fund (if you’ve got kids, that is). But remember, while it’s great to set your children up for success, there are plenty of ways your child can help pay for college themselves—without student loans.

6. Have Insurance and a Will

Another personal finance basic is to protect your stuff. And you do that by having the right insurance and having a will.

We know insurance can seem confusing and expensive, but transferring the risk to someone else saves you from having to shell out the big bucks if something happens. You can’t afford to not have insurance.

Here’s a quick rundown of the eight types of insurance you need:

- Auto Insurance

- Health Insurance

- Life Insurance

- Homeowners Insurance or Renters Insurance

- Long-Term Disability Insurance

- Long-Term Care Insurance

- Identity Theft Protection

- Umbrella Insurance

Also, you need a will. We know it isn’t a fun thing to think about, but it’s an important part of getting your personal finances in order. Having a will and a good estate plan can save your family a lot of financial and emotional pain—and keep the government from deciding what happens to your stuff.

7. Pay Your Taxes

Taxes are so fun, right? Right? Okay, no one likes paying taxes. But that doesn’t make them any less important. And your tax money helps pay for a lot of things we take for granted, like schools, roads and national parks (who doesn’t love national parks?).

If you earn an income, you have to pay taxes. And unless you want to owe the IRS a huge chunk of change all at once, you should set aside a portion of each paycheck for taxes. Ever filled out a W-4 form? That’s what it’s for. Then you have to actually file your taxes each year by Tax Day (April 15).

Most people are able to file their taxes with a basic online tax software, while others with more complicated taxes may need to hire a professional. Either way, here are some tax basics you should figure out if you haven’t already:

- How much taxable income you have

- What tax bracket you’re in

- How much of your paycheck to withhold for taxes

And just so we’re clear, getting a huge tax refund is not a good thing. It just means you’ve loaned the government too much of your hard-earned money throughout the year (interest-free!). Your goal should be to pay exactly what you owe (or close enough to it), so you can keep more of your paycheck!

8. Build Wealth, Not Your Credit Score

A lot of people say you need a good credit score if you want to do well in life. But we’re here to debunk that myth. Not only can you survive without a credit score—you can thrive without one!

You see, a credit score (also called a FICO score) is just an “I love debt” score. It’s a history of your relationship with debt. It has nothing to do with how much money you have in the bank or how well you manage it.

Instead of focusing on improving your credit score, focus on saving money, building wealth and being outrageously generous. That’s how you win with money—not by playing the credit game.

And if you follow the other seven personal finance tips we’ve given you, you won’t have to worry about your credit score. (You won’t even have a credit score if you steer clear of debt—which, again, you should!)

Learn the Best Way to Manage Your Money

We know that was a lot of info to cover. But you can make better decisions with your money, big and small. You just need the right game plan.

If you want a deeper dive into how to manage your money the right way, check out Financial Peace University (FPU) —America’s #1 personal finance class.

FPU walks you through all the basics of personal finance, from creating a budget and paying off debt to saving for emergencies and investing for the future—without the confusing financial blah blah blah everyone else is dishing out.

This class has helped nearly 10 million people take control of their money. And now it’s your turn. Find an FPU class near you!

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.