Zero-Based Budgeting: What It Is and How to Make It Work for You

By

George Kamel

By

George Kamel

Key Takeaways

- A zero-based budget means your income minus your expenses equals zero every month.

- Zero-based budgeting is the best budgeting method because it gives every dollar a purpose, adapts to your real life, and keeps you focused on your goals.

- To make a zero-based budget, list your income, plan all your expenses, and subtract expenses from income to equal zero. Track your spending and make a new budget each month.

- A zero-based budget means you plan how you will give, save and spend before the month starts.

- Zero-based budgeting takes more effort than other methods, but that effort is what makes it work.

Does your paycheck show up in your bank account and then just vanish? Yep, been there. But zero-based budgeting can fix that!

Here's a Tip

A zero-based budget is a budgeting method where your income minus your expenses equals zero. You give every dollar you make a purpose, whether that’s giving, saving or spending. That’s it—you’re telling your money where to go before you spend it.

With a zero-based budget, you’re giving every single dollar a job on purpose. It’s hands down the best way to take control of your money and feel confident every time you spend.

I’ll walk you through exactly how a zero-based budget works and how to create one—so you can stop wondering where your money went and start telling it where to go.

What Is a Zero-Based Budget?

The zero-based budget method works when your income minus your expenses equals zero. Basically, every dollar has a job, whether that’s giving, saving or spending. That’s it—you’re telling your money where to go before you spend it. Some folks also call it zero-sum budgeting, but the principle is still the same.

Now this doesn’t mean you drain your bank account to $0 every month. It just means every dollar is accounted for and has a job to do. (We actually recommend keeping a buffer of at least $100–300 in your checking account as your built-in budget safety net.)

Zero-based budgeting isn’t a new concept, either. Peter Pyhrr, a manager at Texas Instruments, developed zero-based budgeting in the early 1970s. Former President Jimmy Carter even tried to bring it to the federal government, but D.C. being D.C., it didn't stick.

How Do You Make a Zero-Based Budget?

Zero-based budgeting is pretty easy once you’ve done it a few times. Here’s the step-by-step process for building a zero-based budget from scratch each month:

- List your monthly income.

- List your expenses.

- Subtract your expenses from your income to equal zero.

- Track your expenses (all month long).

- Make a new budget (before the month begins).

1. List your monthly income.

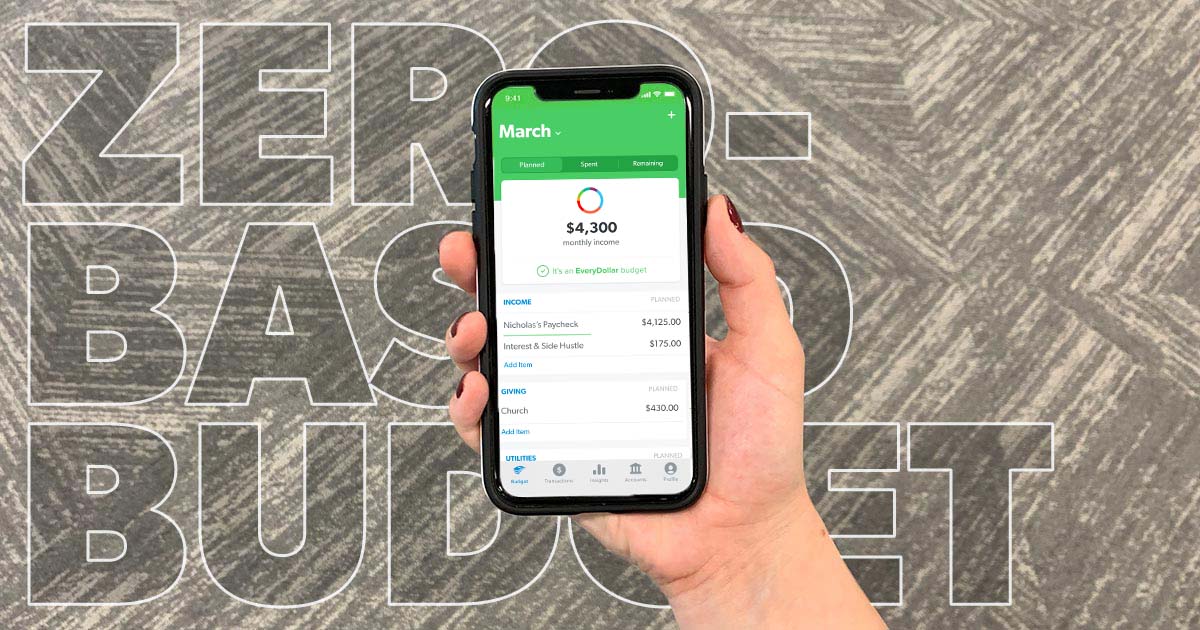

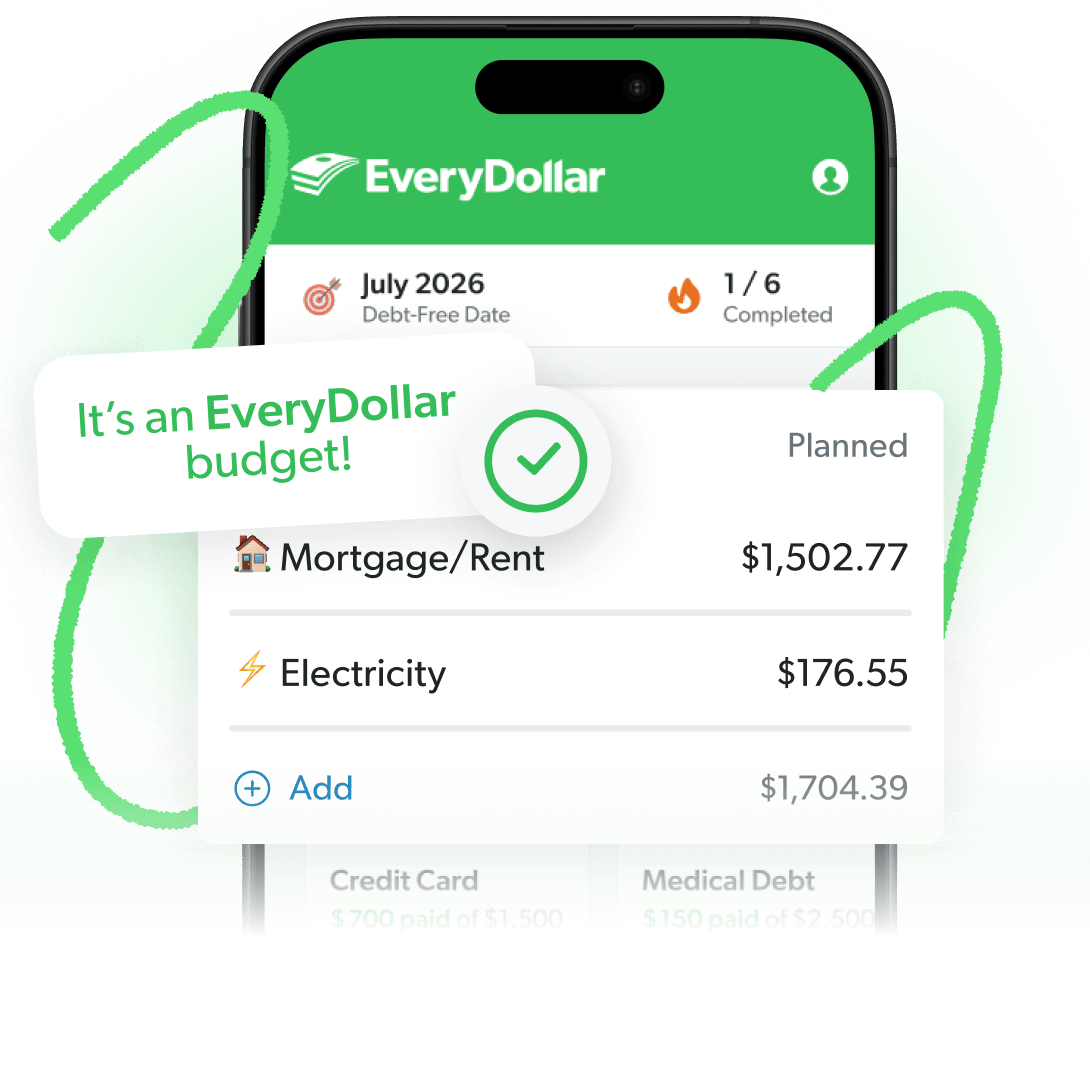

You can list your income the old-fashioned way with a sheet of paper (or several sheets, if you want to practice). But I like to use a budgeting app like EveryDollar, where I can easily plug in and change the numbers in my budget (and hey, it kills fewer trees, too!).

So, what counts as income? Your regular paychecks and anything extra you plan to bring in during the month—like cash from your side hustle as a delivery driver or balloon artist for kids’ parties. Write it all down and add it up! That’s your total monthly income, aka what you’ve got to work with this month.

What if you have an irregular income?

Even with an irregular income like commission or freelance work, you can still get in on zero-based budgeting. Just break out your bank statements from the last few months, take the income from your lowest month, and list it in the budget as this month’s planned income. You can adjust the income later in the month if you make more.

Here's a Tip

Need help getting started? Use our budget template to get your numbers down and then switch over to EveryDollar.

2. List your expenses.

All right, now you know what’s coming in, so it’s time to plan what’s going out. List everything you spend money on in a typical month. And I mean everything. Not just the bills, but things like that oversized Yahtzee set you’re buying for the backyard, too (yes, I’ve seen them at Costco). Scroll through your bank account or check your latest bank statement to see where your money’s really going.

List your expenses in this order:

- Giving: Start with generosity. I recommend giving 10% of your income to a church or local charity. It sets the tone for your budget and keeps you focused on what really matters.

- The Four Walls: This is what I call the basics of life, the expenses you should cover before anything else—food, utilities, shelter and transportation.

- Saving: Whether it’s building your emergency fund or saving for something big, make this a priority. (Quick note: If you’ve got debt and already have $1,000 in a starter emergency fund, throw that savings money at your debt snowball first. Knock out your debt before you build savings!)

- Other expenses: Once the big stuff is covered, add in things like insurance, clothing, childcare and all the other stuff—fun money, subscriptions, random Amazon orders.

This helps you avoid the trap of spending everything you make, then trying to save and give whatever’s left (which, let’s be honest, ain’t going to be much, my friend). Being intentional about giving and saving is a healthy money habit that leads to long term financial peace. And we all want that, right?

Here's a Tip

Make sure you add a miscellaneous category to your zero-based budget. That way, when random expenses pop up, you don’t have to panic because you’re covered!

3. Subtract your expenses from your income to equal zero.

Once you subtract all those expenses from your income, the goal is simple: Hit zero. Didn’t get it right on the first try? Welcome to the club. No one nails it on the first pass, and that’s totally fine.

Here’s how to fix it so you’ve got a zero-based budget:

Got money left over?

Put that money straight to work on your current Baby Step.

What’s a Baby Step? Glad you asked. The 7 Baby Steps are your proven, step-by-step plan to save money, pay off debt, and build real wealth.

So if you’ve got any extra cash in your budget, throw it at whatever Baby Step you’re currently on. That’s how you make serious progress toward your money goals.

Then toss some confetti and do a victory dance (or if you’re a terrible dancer like me, a solid fist pump will do). You’re doing great!

What if you’re in the red?

If your expenses are higher than your income, that’s a red flag, but don’t panic. You just need to make some cuts. So grab those metaphorical clippers and start trimming your budget.

You can lower some spending categories or cut others entirely. I’d start by slashing that restaurant budget. Learn to meal plan and keep yourself out of the drive-thru. Your wallet will thank you.

Still not enough to cover your expenses? Time to boost that income. Pick up a side hustle, sell some stuff, or get creative. Be a sign spinner, car detailer or neighborhood dog walker—I don’t care. If it pays, it plays.

That’s how you build a zero-based budget. But I’ve got two more steps that’ll help you actually stick with it.

4. Track your expenses (all month long).

For your zero-based budget to work, you can’t just set it and forget it. That budget you built is a tool. And tools only work if you use them.

So, track every transaction. Every single one.

When money comes in—log it. When it goes out—track it in the right budget category. Made $100 from a side hustle? Drop it in your income. Paid rent? Subtract it from housing. Filled up your tank? That goes under transportation.

Tracking your expenses is how you stay on top of your money throughout the month. This is how you avoid overspending and wrecking your budget. And if you do overspend in one category, no worries! You’ll just need to move money over from a different budget category to maintain that zero balance. For example, if you spent $50 more on groceries than you planned, you can pull $50 from your clothing budget or your fun money line. The total still equals zero.

Want to make tracking easier? Use the EveryDollar app! It links to your bank so your transactions stream right in. Then it’s just drag, drop, done.

Find Margin You Didn’t Know You Had With EveryDollar

The EveryDollar budgeting app helps you find extra money every month so you can beat debt, build wealth, and make progress. Every. Day.

5. Make a new budget (before the month begins).

While the basics of your budget might not change a lot month to month, some expenses will fluctuate. December’s budget looks nothing like July’s budget (less fireworks, obviously). And that’s the point: Zero-based budgeting works because it matches your actual life, not a template you set and forget about.

That’s why you need to create a brand-new zero-based budget. Every. Single. Month.

Plan ahead for month-specific expenses (birthdays, holidays, school supplies) so they don’t sneak up and wreck your plan. If you came in under budget in a category last month, congratulations! Adjust the budget amount and add the margin to another category that needs it. Or, put it toward your current Baby Step!

And don’t wait until you’re halfway through the month to do this. Make a plan for your money before the month starts—so you’re in control from day one.

If you still need some help getting started, try our Budget Calculator. It’ll help you see how you could divide your income into recommended budget categories. Then take those numbers to EveryDollar to build your actual plan.

What Does a Zero-Based Budget Look Like?

Just to recap, a zero-based budget lists all your income at the top and all your expenses below it, and the difference between them should equal zero. Every dollar is assigned to a category before the month starts.

Let’s break this down so you can see exactly how it works in real life with a super simple zero-based budget example. We’ll use a $5,000 monthly income.

Income

|

Paycheck 1 |

$2,200 |

|

Paycheck 2 |

$2,200 |

|

Side Hustle |

$600 |

|

Total |

$5,000 |

Expenses

|

Giving |

$500 |

|

Food |

$650 |

|

Utilities |

$200 |

|

Housing |

$1,250 |

|

Transportation |

$300 |

|

Insurance |

$850 |

|

Debt |

$1,110 |

|

Fun Money |

$40 |

|

Miscellaneous |

$100 |

|

Total |

$5,000 |

Income ($5,000) - Expenses ($5,000) = $0

Now let’s take a look at an irregular income example with a $3,200 monthly salary. (We’ll assume you’ve already set aside 25–30% for freelance taxes.)

Income

|

Freelance Job 1 |

$900 |

|

Freelance Job 2 |

$1,500 |

|

Freelance Job 3 |

$500 |

|

Side Hustle |

$300 |

|

Total |

$3,200 |

Expenses

|

Giving |

$300 |

|

Food |

$650 |

|

Utilities |

$200 |

|

Housing |

$1,000 |

|

Transportation |

$300 |

|

Insurance |

$150 |

|

Debt |

$500 |

|

Fun Money |

$20 |

|

Miscellaneous |

$80 |

|

Total |

$3,200 |

Income ($3,200) - Expenses ($3,200) = $0

What are the Advantages and Disadvantages of Zero-Based Budgeting?

Now there are upsides and downsides to everything, including zero-based budgeting. The biggest advantages are knowing where all your money goes, flexibility, and a focus on long-term goals. The biggest disadvantage is that it takes a little more time and effort than other methods. You build a new budget every month and track every transaction. But that extra effort is exactly what makes it work!

Advantages of Zero-Based Budgeting

- It makes you aware of your spending. A zero-based budget is a real eye-opener to how much money you actually spend, like the five streaming services you don’t watch.

- It adapts to real life. This budget can stretch like Mister Fantastic, changing each month to match how you really use your money—an oil change, a vacation or even a dental appointment—so you can move money where it needs to go.

- It prevents impulsive spending. Knowing how much you have to spend helps you say no when your Instagram algorithm happens to serve up an ad for that air fryer you and your friend were just chatting about, or when your favorite 90s band announces a reunion tour. You can have fun with your money—just budget for it.

- It helps you prioritize your goals. Want to pay off debt, save for a house, or pay off your mortgage? A zero-based budget allows you to intentionally plan for those goals rather than just hope there’s money left for them at the end of the month.

Disadvantages of Zero-Based Budgeting

- It takes more time than other methods. Building a new budget every single month and tracking every transaction takes time. This is not a set-it-and-forget-it system.

- It requires discipline, especially in the first few months. Just like any time you try something new, it’s going to be hard at first. Your first budget will feel clunky, and you’ll probably leave out some expenses. The second one will be better. And by month three, it’ll become routine.

- It can feel restrictive if you’ve never budgeted before. When you start telling every dollar where to go, it can feel like you’re losing freedom. But in reality, you’re gaining the freedom to spend!

- Couples may disagree on category amounts. When every dollar has a job, both you and your spouse need to agree on those jobs. Budgeting forces couples to talk about money, but it can create friction early on. That’s why you need to make it part of something fun, like a date night.

Yes, zero-based budgeting can take a little more time than other methods. But thinking things through always takes more time than just guessing (do you want to step foot in a building that an architect just eyeballed when he designed it?). It’s about being intentional. That’s why zero-based budgeting works and why I’ll keep talking about it until everyone’s doing it.

How Does Zero-Based Budgeting Compare to Other Methods?

Now here’s how zero-based budgeting stacks up against other budgeting strategies.

How does zero-based budgeting compare to traditional budgeting?

The traditional method of budgeting is basically: Write your income and expenses down once . . . and hope for the best. Yeah, good luck with that.

With traditional budgeting, there’s no tracking, no adjusting and no accountability. Your stray dollars don’t have a job and get lost in the shuffle. Then you find yourself overspending and your budget falls apart.

Zero-based budgeting is the total opposite. You track, adjust and stay engaged all month long.

How does zero-based budgeting compare to the 50/30/20 rule?

The 50/30/20 rule splits your income into fixed percentages: 50% for needs, 30% for wants and 20% for savings. It sounds simple, but it doesn’t adapt to your situation or prioritize debt payoff.

Here are some of the problems with the 50/30/20 rule:

- This rule teaches you to always save. But if you’re following the Baby Steps, you’re not always saving—you might need to be paying off debt. You win by being laser-focused on one goal at a time.

- This method includes debt in the “needs” category but only suggests you make minimum payments. That won’t get you anywhere fast.

- It doesn’t adapt to your situation. Whether you’re drowning in student loans or debt-free and investing, the ratios stay the same. That’s not helpful.

- The math is way off. Most Americans spend more than 50% of their income on needs.

Bottom line: 50/30/20 sounds cute, but it doesn’t reflect real life or real money goals. Zero-based budgeting assigns every dollar a specific job based on your actual life and goals.

How does zero-based budgeting compare to the 60% solution?

This method says to live on 60% of your income and save the other 40%. That 40% gets split up into retirement, long-term savings, short-term savings and “fun.” Sounds really vague—unlike zero-based budgeting, where each and every dollar is accounted for.

What if you’re in Baby Step 2? Saving isn’t your priority—debt payoff is. Once debt is gone, then you should build your savings, then you should invest 15% in retirement. There’s a clear order that the 60% method doesn’t account for (but zero-based does).

And again, this plan doesn’t work for most people’s real-world budgets.

How does zero-based budgeting compare to reverse budgeting?

Reverse budgeting prioritizes savings first, then spending. Cool idea in theory, but not always in practice. Like most budgeting methods, it assumes a one-size-fits-all approach. Zero-based budgeting adapts to you.

I love the savings-first mindset, but if you’re focused on killing debt, this doesn’t match your goal. However, once you’re debt-free, combining a zero-based budget with automatic saving is a great way to build wealth.

How does zero-based budgeting compare to envelope budgeting?

Envelope budgeting (where you put real cash in envelopes designated for each budget category) works hand in hand within a zero-based budget. In fact, it’s just another way to do zero-based budgeting.

Here’s what I mean: You can use the envelopes as a tool to execute your zero-based budget, especially for variable spending categories like groceries and dining out. Once the money is gone, it’s gone, baby.

|

Budgeting Method |

How It Works |

Main Limitation |

|

Zero-based budgeting |

Every dollar is assigned a job each month. |

Requires active tracking. |

|

Traditional budgeting |

Income and expenses are listed once. |

Easy to lose track of spending. |

|

50/30/20 rule |

Income is split into fixed percentages. |

Doesn’t adapt to real-life goals. |

|

60% solution |

Live on 60% of your income and save the other 40%. |

Doesn’t focus on paying off debt. |

|

Reverse budgeting |

Budget for savings first, then for spending. |

Doesn’t focus on paying off debt. |

Is Zero-Based Budgeting Right for You?

Zero-based budgeting works for anyone who wants to take control of their money—whether you are budgeting for the first time, paying off debt, managing an irregular income, or building wealth. Let me put it another way: If you earn money and spend money, this method works for you. The only requirement is willingness to be intentional.

- Beginners who’ve never budgeted before: Zero-based budgeting gives you a clear framework so you’re not guessing.

- People paying off debt: Every extra dollar goes straight to your debt snowball—no leftover money sitting on the sidelines.

- People with irregular income: You budget based on your lowest recent month and adjust if you earn more. It’s built for unpredictability.

- Couples managing money together: Every dollar gets assigned a job, which means both you and your spouse agree on the plan before the month starts.

- High earners who feel like their money disappears: Making more money doesn’t fix a spending problem. But Zero-based budgeting does.

Zero-based budgeting is about making smart choices with what you have regardless of your income.

What Is the Best Tool for Zero-Based Budgeting?

I’ll cut to the chase: The best tool for zero-based budgeting is EveryDollar—Ramsey’s budgeting app built specifically for the zero-based method. You set up your budget, connect your bank account, and track every transaction by dragging and dropping it into the right category. It resets every month so you can start fresh.

Some of the app’s features that’ll help you become a zero-based budgeter include:

- Bank connection: Transactions stream in automatically so you don’t have to manually enter every single coffee and gas fill-up.

- Drag-and-drop tracking: You drag each transaction into the right budget category.

- Monthly reset: EveryDollar prompts you to build a new budget every month . . . because that’s how zero-based budgeting works.

- Personalized plan: After a few setup questions, EveryDollar builds a starting budget based on your income and situation, and it can even help you plan out your long-term money goals.

Just download EveryDollar, answer a few questions, and it’ll help you make the most of every dollar, every day (see where we got the name?).

Next Steps

- List every source of income you expect next month: paychecks, side hustles, everything. Add it up. That’s your starting number.

- Write down every expense you’ll have next month: bills, groceries, gas, subscriptions, fun money, whatever else. Assign every dollar to a category until income minus expenses equals zero.

- Download EveryDollar and build your first zero-based budget in the app. Connect your bank account so transactions stream in automatically.

- Track every transaction to a category for the entire month.

Zero-Based Budgeting FAQ

-

What does “zero-based budget” mean?

-

A zero-based budget is a budgeting method where your total income minus your total expenses equals zero. Every dollar you earn is assigned a specific job (giving, saving, spending or paying off debt) before the month begins. It doesn’t mean your bank account hits zero at the end of the month.

-

What are the pros and cons of zero-based budgeting?

-

The main pros of zero-based budgeting are knowing where all your money goes, flexibility, and a focus on long-term goals. The main con: It requires more time than other methods and takes discipline to maintain.

-

What tools work best for zero-based budgeting?

-

EveryDollar is the best app for zero-based budgeting. It connects to your bank, lets you drag and drop transactions into budget categories, and resets every month so you can build a fresh budget.

-

Can you make a zero-based budget with an irregular income?

-

Yes. If your income changes month to month, pull up your bank statements from the last few months, find the lowest-earning month and use that number as your planned income. Budget your expenses, starting with the most important categories first: first giving, then food, utilities, shelter and transportation. If you earn more than planned, assign the extra to your current financial goal.

-

How is zero-based budgeting different from envelope budgeting?

-

Envelope budgeting is a spending-control tactic where you put cash in labeled envelopes for each category. Zero-based budgeting is a complete budgeting method where every dollar of income is assigned a job. You can use envelopes inside a zero-based budget.

-

How long does it take to get good at zero-based budgeting?

-

Most people need about three months to hit their stride with zero-based budgeting. The first month feels clunky—you’ll probably forget expenses and have to adjust midmonth. The second month is smoother. By month three, building your budget takes 15–20 minutes and tracking becomes second nature.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

George Kamel

Get proven Ramsey answers fast.