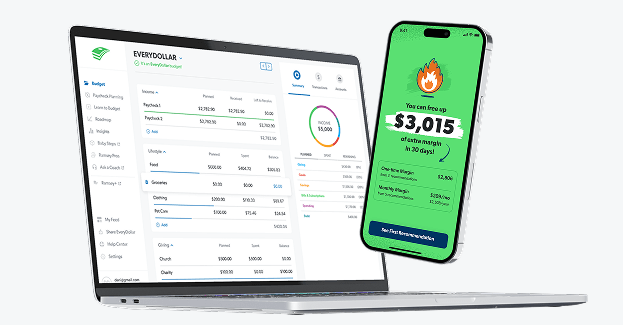

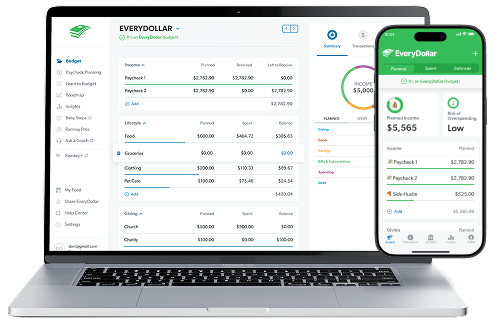

EveryDollar Budget App

With EveryDollar, you’ll find extra margin every month and get a personalized plan to make the most of it. Every day.

Guide Contents

If you're wondering how to start a budget—and actually stick to it—you're in the right place.

A budget is a plan for your money: tracking every single dollar that’s coming in (income) and going out (expenses). When you learn how to budget—and when you make one every month—you give your money purpose. You take control.

These five steps will walk you through budgeting for beginners so you know exactly how to get started.

Let’s put some breathing room in your budget. With EveryDollar, you’ll keep tabs on your spending and find extra margin every month—starting with $3,015 in just 15 minutes. You’ll feel like you got a raise!

No matter if you’re a beginner budgeter, no matter what money goals you have, and no matter what your income is, you can create (and keep) a budget.

Seriously! Learning how to set up a budget is simpler than you think—and these five steps will help you build it.

But first: Before you start, open up your online bank account or pull out those hard copy bank statements from the past couple months. Trust us—it makes the process way easier when you can look back at your numbers.

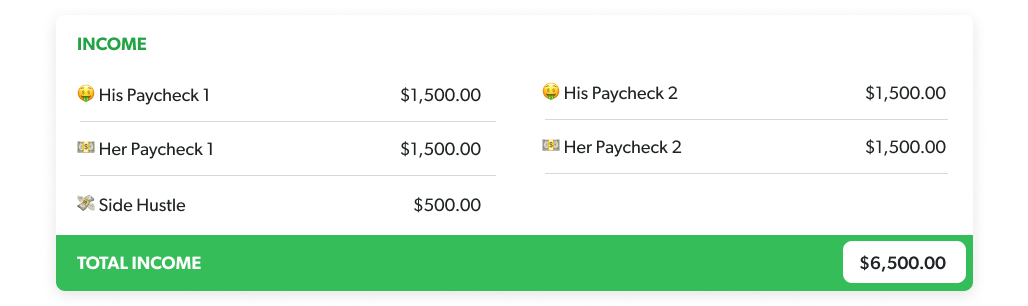

Income is any money you plan to get during that month.

Create separate income budget lines for every paycheck you (and your spouse, if you’re married) make, plus anything extra coming in (like a side hustle).

Do you have an irregular income?

If you’ve got an irregular income, take a look at what you’ve made the last few months and list the lowest amount as this month’s planned income. You can adjust later in the month if you make more and add that extra money to your current money goal or another budget line. Check out our Irregular Income Budget Planning form for more help!

Now that you’ve planned for the money coming in, you can plan for the money going out. It’s time to list your expenses and assign each category a dollar amount! (Yep, this is when that bank account or statement gets super helpful.)

Make a budget category for each expense, and then you can create budget lines underneath each category.

Think of a budget category like a folder and the budget lines like the files inside it. For example, Food is a budget category, and Groceries and Eating Out are budget lines that go under it.

Think through these main areas as you’re jotting down expenses:

Before you put the things you pay for every month into your budget, set aside money for giving. We believe in putting 10% of your income here and always having a spirit of generosity!

Also, if you don’t have an emergency fund yet, you need to make saving one of your priorities—starting with Baby Step 1. We talk about this more in the How to Budget for Your Money Goals section.

Next, cover your Four Walls. That’s food, utilities, shelter and transportation.

By the way, that Grocery budget line is super hard to guess at first, so just start with your best estimate based on your past spending. You’ll learn what you actually need to budget after a few months.

Next up, list all other monthly expenses.

Okay, that was a lot. To recap, here are those common expenses. We’ve got things in here that might not apply to you, but it should give you a good idea of what your budget categories might look like.

Now that you’ve organized every expense and given each category a dollar amount, subtract all your planned expenses from your income. This number should equal zero. We call this a zero-based budget.

Now, a zero-based budget doesn’t mean you let your bank account reach zero. Leave a little buffer in there of about $100–300. It also doesn’t mean you blow all your money.

And here’s the reason we love this method: Zero-based budgeting just means you give every dollar a job to do—giving, saving, spending. It’s all accounted for and has a purpose.

Don’t leave it there. You’ll end up mindlessly spending it on dollar bin items and one-click wonders. Put those dollars to work by putting any “extra” money toward your current money goal.

You just need to cut expenses until your income minus your expenses equals zero. (Hint: Start with those Eating Out and Entertainment budget lines.)

You can also get a side hustle or work overtime. Just remember—if you increase your income, don’t increase your spending! The extra cash should cover your budgeted expenses.

Tracking your transactions means you account for everything that happens with your money all month long.

That means when you make money, you track it in your budget. When you buy absolutely anything, you track it in your budget. This step gets your eyes on your spending so you don’t overspend.

Tracking transactions is such a huge key to winning with budgeting (and money) that we have a whole section below about how to do it and why it’s important.

While your budget shouldn’t change too much from month to month, the fact is, no two months are exactly the same. That’s why you create a new budget every single month—before the month begins.

Start by copying over this month’s budget to the next. Then make changes for anything new that’s coming.

Where does the money come from? You can cut back spending somewhere else and move that money over to this category or crank up your income for the month. (Time for an extra freelance gig!)

P.S. Having an accountability partner really helps during those first months of budgeting (and during the whole journey).

If you’re new to budgeting, this calculator is a solid starting point. Just type in your monthly take-home pay, and you’ll get an example budget to help you begin.

The calculator gives you a quick snapshot. The EveryDollar budget app brings your money into full clarity with a personalized plan that helps you beat debt and build lasting wealth.

With EveryDollar, you’ll find extra margin every month and get a personalized plan to make the most of it. Every day.

Use our envelope system to pay cash for those hard-to-wrangle budget lines (like Groceries, Restaurants and Entertainment).

With six colors to choose from, this leather wallet is the most stylish way to organize your spending.

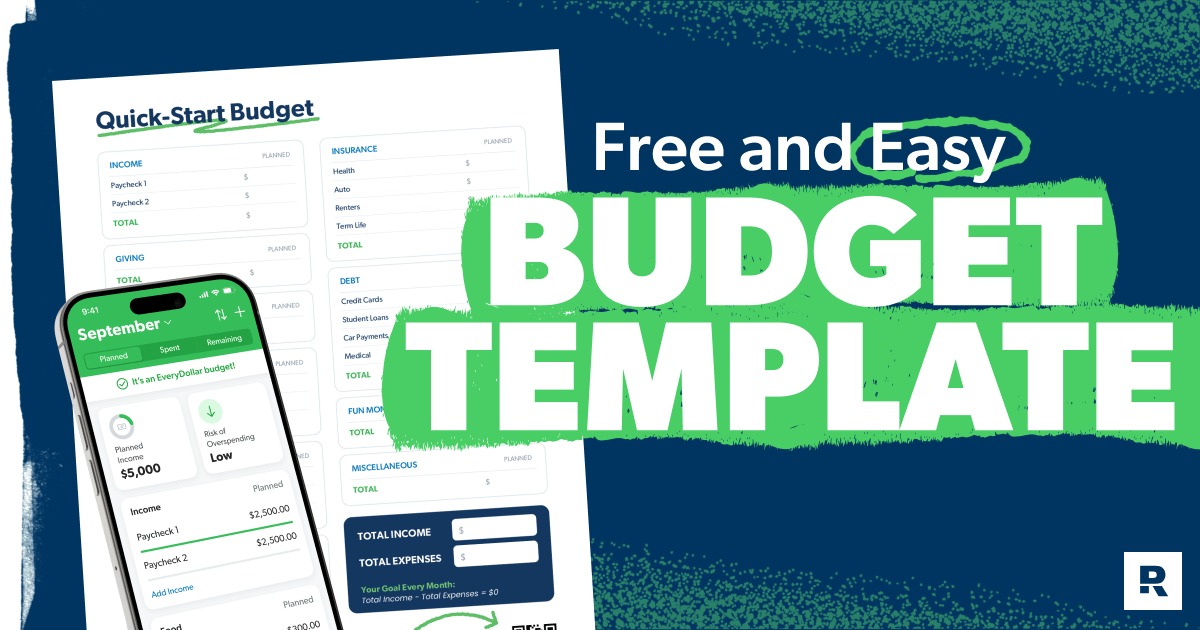

Want to try the pen and paper method first? Download our budgeting forms to help you get started—including our free and easy starter budget template.

Ready for one of the biggest secrets for how to make a budget—and do it really, really well? Good, because we don’t want to keep it a secret. Here it is: Track. Your. Transactions.

Every single one.

It’s the fourth step in our five-step budgeting breakdown, and now we’ll dive into the how and why of this “secret” way to level up your budgeting.

Pro tip: With EveryDollar, tracking is a breeze. You can connect your budget to your bank so transactions stream right in. You just drag and drop them to the right budget line. Boom.

Tracking your transactions helps you:

Every money goal starts with a budget. Because a budget is how you tell your money where to go. And if you want that money going toward paying off debt, saving for vacation, or prepping for emergencies . . . well . . . you need to budget for it.

Here are some tips for how to make budget for your money goals:

If you don’t know which money goal to go after first, check out the 7 Baby Steps (aka the proven plan to save money, get out of debt, and build wealth).

Pro tip: If your goal is to pay off debt or save for emergencies, it’s best to work on those one at a time. After you free up your income and have the security of that stacked emergency fund, you’ll have margin to multitask on other goals like investing, saving for the kids’ college, or paying off your house.

If you’re trying to save money for a big expense, create a sinking fund. This is a way to save up by setting aside money each month. You just divide the amount of money you need by the months you’ve got to save. Voilà. Now you know how much to put in your monthly budget for this money goal.Like if you need $1,200 for a summer vacation in four months, you’d need to save $300 a month.If you want to pay off debt, check out the Debt Snowball Calculator.

If you want to save up an emergency fund, you only need two things: a budget line for emergency fund savings and the mindset that this is a priority with your money!

Okay, but were does that money come from? The extra for your vacation savings or debt snowball momentum or emergency fund growth? Good question. Here are a few ways to get more money to put toward your goal:

Some money goals take longer than others. Don’t. Give. Up. You have what it takes to pay off your debt, save for the future, build yourself legit financial security . . . the list goes on. Keep budgeting. Keep working. You got this!

From groceries to summer vacations and everything in between—a budget helps you spend and save on purpose. And these tips will help you do it all with confidence.

One of our top budget tips is to pick the best method out there: zero-based budgeting.

Zero-based budgeting is how you get intentional with your money. All of it. Any “extra” money left after you list out your expenses doesn’t stay extra—it’s given a purpose and a job. Put it into a budget line so it doesn’t get spent accidentally.

And it doesn’t matter if you get paid weekly, biweekly or monthly. Zero-based budgeting will work for you.

Remember, you work hard for your money. Every single dollar should work hard for you. That’s the power of the zero-based budget!

Have you ever made a goal that was totally setting you up for failure? Like saying you’ll read ten books a month when you barely have any free time? If you want to succeed, you have to push yourself—but you also have to be realistic.

The same is true with your budget. Push yourself to spend better and save more, but be realistic for your life. When you keep it real, you can really win.

You may want to break some of your budget lines into weekly portions to help you spread out your spending. This is super helpful if you get paid more than once a month—but it’s a great trick for any budgeter.

For example, if you give yourself $200 for Personal Spending, think of it as $50 a week. If you plan for $600 on groceries, that’s like spending about $150 a week.

Sometimes thinking in these bite-size amounts makes it easier to stick to your budget.

We mentioned this before, but you need a little space for anything that pops up or you forget (like school photos or your anniversary—wait, don’t forget that!). A Miscellaneous budget line helps you cover these expenses without busting your budget or running to the credit card. Speaking of which . . .

We’ve got about a million reasons (at least) to stop using your credit cards, but here are just two.

First: If you’re using credit cards to pay for normal monthly expenses and making a bulk payment at the end of the month—that’s a bad money management system.

Paying that lump sum means you don’t see how often you buy breakfast biscuits on the way to work. What if you’re literally eating away at what could be a healthy retirement fund? When you track every expense, your expenses can’t hide from you.

Second: If you get behind on payments, you rack up interest. (Research done by Ramsey Solutions shows 4 out of 10 credit card holders fall in this category, by the way.) And you’re getting stuck in the cycle of paying off last month’s expenses this month.

You can never get ahead that way. Budget this month’s money to pay for this month’s expenses—and to save for the future! That’s how you stay in control of your money.

The decisions you made yesterday don’t have to determine today. When you make mistakes with your money (and you will—everyone does) don’t throw a pity party. Keep. Moving. Forward.

Don’t worry about what everyone on social media appears to have. Some of them are lying. Some are in debt up to their designer sunglasses. And a few really do have their lives together. But those people worked hard for it—and that’s what you’ll do too.

Work hard defending your budget and say no or not now when you need to. Being true to yourself, your budget and your money goals is more valuable than anything you could ever buy.

It usually takes three months to get a handle on this whole budgeting thing. It won’t be perfect the first time or the second time. But you’ll get there! Give yourself grace as you go.

Budgeting isn’t a sprint. It’s a marathon, a commitment, a lifestyle! Keep all these tips for staying motivated in your back pocket, and pull them out whenever things get hard.

And when it does get tough, remember: You’re tougher.

Do yourself a huge budgeting favor and get an accountability partner.

Here’s why: When you’re in the thick of making any goal happen, knowing you’ve got someone checking in makes all the difference. And budgeting regularly is not only a great goal—it’s also the foundation for hitting all your other money goals!

Listen, there’s no shame in asking someone to help you keep your eye on the goal. Just the opposite. There’s incredible strength in seeking accountability.

Here's some info to help when you're looking for and working with your accountability partner.

Got a spouse? Boom. You’ve got a built-in accountability partner, which brings its own challenges (and we’ll get to that in a second).

But if you need to handpick your accountability partner—or if, as a couple, you want to find another couple to check in with—this list of characteristics will help you find a top-notch one:

Get with your accountability partner every month to check in and set up the next budget. If you’re married, you and your spouse will do this together and in person at a monthly budget meeting. If you’re working with a friend or family member, you’re welcome to make your budget alone, but never skip the check-in.

If you aren’t sure what to actually do in these meetings, grab yourself a copy of our budget meeting guides (we’ve got a classic and couples edition).

So, get with your accountability partner and start planning those budget meetings. Today!

Yeah, if you're married you’ve got a built-in accountability partner, but that doesn’t mean you can skip being a high-quality accountability partner. Look back over all those characteristics we just mentioned.

Be encouraging, empowering, honest, judgment-free, vulnerable, trustworthy and present with your spouse! Always—but especially when you’re talking about money.

And what if you feel like you’re miles away from being able to have successful budget meetings with your spouse, because you’re not even on the same page about money? Have a conversation together that follows these four guidelines from money expert Rachel Cruze.

1. Be honest.

When you’re talking about money, dreams and building your life together, it’s important to be vulnerable and honest with your partner. These types of conversations are the ones that strengthen the foundation of your relationship and ultimately your life together.

Be honest about what you believe and how you feel, then allow your spouse to do the same.

2. Listen.

Really listen to your spouse. Don’t just listen to think up a response of your own.

Here’s an idea: When your spouse is talking, you can only ask questions. This will help you understand why they feel that way. Then, when they’re finished, you can share your thoughts about what they said.

3. Stay calm.

When you raise your voice, your spouse will likely raise theirs to match. Then you’re both talking loudly (or yelling) just to be heard. If you’re listening intently and asking questions, you won’t need to yell. So stay calm no matter what.

4. Show grace.

Being too hard on yourself or your spouse won’t help. Find a way to bring grace and truth together, and live in the center of the two. You’ll both have to sort through hard truths, but learning how to respond to each one with grace will go a long way.

If you want even more help with this, take Financial Peace University together. This nine-week class is perfect for any couple—whether you’ve been married five minutes or 50 years. You’ll learn how to have healthy conversations about money, set goals together, and budget as a team.

Let’s be honest—sometimes all this budgeting stuff gets . . . well . . . exhausting. It can be tough to keep that financial drive alive.

Here are eight tips and tricks to keep the motivation going along the way.

If you hang out with senseless spenders, you can be tempted to do the same. Find some friends who won’t pressure you to do stuff outside of your budget.

Okay, not just any app. Our app: EveryDollar. Because you can try to keep up with pencil and paper or spreadsheets, but they aren’t as easy. Budgeting made easy is the whole point of EveryDollar! And let’s face it, an easier budget is one you’re way more likely to stick to.

Dig deep and be honest about the reasons you want to take control of your money once and for all. That’s your why. And when things get tough or boring, remember your why!

Hang up images around the house that represent your goals. Paying off that car? Put a picture of it on your fridge to remember why you’re cooking at home instead of ordering that delivery pizza.

Lower the risk of budgeting burnout by budgeting for fun. Now, if you’re saving for an emergency fund or paying off debt, that fun money will be small. But it’s just for a season. You’ve got this!

When you reach a goal—even a small one—celebrate! After you budget three months straight, pay off a debt, or cut extra spending for 30 days, treat yourself to a free or budget-friendly reward.

If you respond to stress by impulse buying things, replace that habit with a better one. A nice relaxing bath, a walk or run outside, a card game with your family, a cup of chamomile tea—these are all great (and inexpensive) ideas.

Hey, burnout happens to us all. Go ahead and decide now what you’ll do when it comes. Just don’t give up on budgeting. It’s how you’ll make your money goals happen, and that’s worth fighting for!

If you’ve never budgeted before (or it’s been a while) jumping in can be challenging. You know what'll help you feel confident as you start? A budget template!

Is your paycheck different from month to month? Learn how to manage irregular income and create a budget that keeps you in control—no matter how much you earn.

Whether you're new to budgeting or looking to improve, these budgeting tips will help you take control, stay on track, and feel confident with your money.

A budget is a plan for your money—every single dollar that’s coming in (income) and going out (expenses).

Cover your Four Walls—food, utilities, shelter and transportation—before you budget for other essential expenses and fun.

This depends on what Baby Step you’re on (aka the proven path to saving money, ditching debt, and building wealth).

Once you’re debt-free and have a fully funded emergency fund, start investing 15% of your gross household income in retirement accounts.

There are plenty of ways to budget: pencil and paper, spreadsheets, budgeting apps. Just make sure you budget every dollar, every month. If you want an easy way to create and keep up with your budget, check out our EveryDollar budget app!

You’ve probably heard of the 50/30/20 rule or the 60% solution, but we use the zero-based budgeting method. This is when your income minus your expenses equals zero—meaning you’re giving every dollar you make a job to do so none of it gets accidentally spent! It’s simple math that works no matter your household income.

It’s really easy for anyone to get started budgeting, even if you’ve never done one before. All you do is:

The real trick for beginners is keeping to the budget. Many temptations will come to throw you off track. But stick to the plan, give yourself grace, and keep going.

It’s completely normal to have a few rocky budgets to start. It usually takes around three months to get comfortable and stick to a budget. You’ve got this.

Absolutely! When you’re listing your income, look over the last few months and pick the lowest amount you made for this month’s planned income budget line. You can adjust later in the month if you make more!

Budgeting is simply making a plan for your money before you spend it—so you’re telling your money where to go instead of wondering where it went. At Ramsey, we use a zero-based budget, where your income minus your expenses equals zero.

Include every category where your money goes each month.

For example:

Every budget should be as personal as possible, created to suit your life, income and money goals. Customize your categories so they make sense to you to make sure every dollar has a job at the beginning of the month. But don’t get too in the weeds. Maybe you don't need to specifically budget for plant seeds, but your gardening hobby overall might get its own budget line.

Make a new budget every month before the month begins. Each month will look a little different, so your budget should flex with it.

If you get paid weekly, biweekly or monthly, just plan your expenses around each paycheck and adjust as needed.

The best way to budget with irregular income is to use your lowest earning month from the past few months as your estimated income for the next month. This helps you avoid overspending and keeps you living within your means.

Keep it simple: Plan your spending, track transactions as you go, and adjust when needed. It’s also important to remember your why—the reason you need to stick to your budget (getting out of debt, saving for a vacation or a house, etc.).

Before you jump into the bills and other expenses, set aside money for giving. We believe in putting 10% of your income here. And if you don’t have an emergency fund yet, make savings one of your priorities.

Next is the Four Walls: food, utilities, shelter and transportation. Create a budget category for each of these. Do the same with your remaining essentials like insurance, childcare and debt (if any).

Finish with nonessentials like personal spending, entertainment, dining out, subscriptions and miscellaneous.

If you go over in a category, that’s okay! Just cut back somewhere else to keep your budget balanced. Then, for your next month, update that category based on what you learned about your spending.

Yes. It doesn’t matter how much you make—budgeting is about what you do with what you make. Some people making six figures a year live paycheck to paycheck because they don’t manage their money well. A budget gives you clarity, direction and peace with your money, no matter your income.

The best tool is the one you’ll actually use and stick with. Start with a simple budgeting app, like EveryDollar, or a template that helps you easily plan, track and adjust as you go.