By

By

Link copied!

Unable to copy link. Please try again.

Key Takeaways

- Living paycheck to paycheck means your money’s gone as fast as it comes in. There’s no breathing room and no savings, and you’re just surviving from one payday to the next.

- You can break the paycheck-to-paycheck cycle by getting on a budget, taking care of your Four Walls first, cutting extra expenses, building an emergency fund, and increasing your income.

- Even if you make more money, you have to intentionally live below your means and set financial goals to make progress.

You know the feeling: Payday hits, and the money's already spoken for. Bills, gas, groceries . . . maybe even a little Friday-night takeout to celebrate. And just like that, your bank account’s almost empty again.

That’s living paycheck to paycheck. It means you’re always counting down to the next payday, never getting ahead, and have nothing left to save. I’ve been there. And I want you to know, you don’t have to stay stuck.

I’ll show you how to break the cycle, take control of your money, and finally start moving toward the life you want.

How to Stop Living Paycheck to Paycheck

1. Get on a budget.

First things first: If you’ve been living paycheck to paycheck, you can’t afford not to know where your money’s going. I’m not talking about a rough idea—I mean knowing exactly where every single dollar lands.

A zero-based budget shows you the full picture, helps you take control, and gives you a plan to stop the money stress. So, if you’re not already budgeting, it’s time to start.

Trust me, you’ll notice spending habits you didn’t even know you had. (I spent how much on eating out last month?) Then, you can make the changes you need to not only cover the basics—but also plan for your future.

Another way to think about budgeting is that it’s custom organization for your money. And if you’re living the paycheck-to-paycheck life, your money needs some organizing. Don’t put it off. Create your first budget. Like, right now.

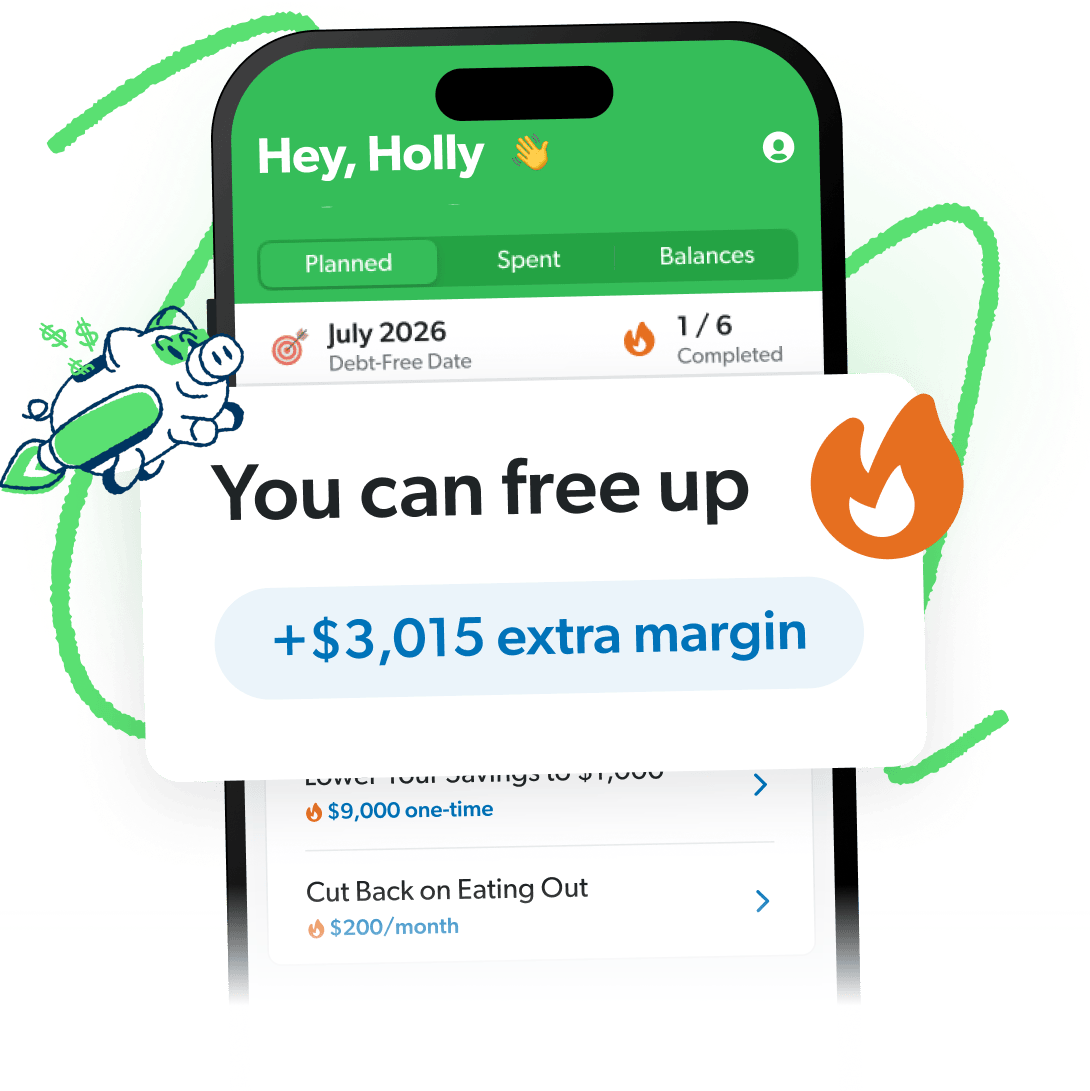

The Budgeting App That Finds Hidden Margin

You’ve got more margin than you think. EveryDollar helps you find it in minutes so you can start making real money progress, really fast.

2. Take care of your Four Walls first.

When setting up your budget, write down your monthly income first. Then you’ll subtract your monthly expenses—starting with the essentials. The Four Walls are your top priority, so make sure your budget is ready to cover these things before anything else (in this order):

- Food

- Utilities

- Shelter

- Transportation

When you start with your Four Walls, you’re making sure your family gets fed, your lights stay on, you have a roof over your heads, and you’ve got gas in the car to get to work. Once you’ve covered those things, then you can make a list of everything else you need to pay for, in order of importance.

So, instead of hitting the end of the month panicked and coming up short, you’ll breathe easy knowing the essentials are already covered. Because you had a plan.

3. Cut extra expenses.

Once you’ve made a budget, you might be shocked to see just how much is slipping through the cracks. That’s the wake-up call and the breakthrough.

Cutting back your spending (or cutting things out completely) is how you start freeing up money so you’re not stuck in survival mode every month. This is where the real change begins. So, comb through your budget and see what you can do without.

Here’s a big one: Stop eating out. (Yes, I’m coming directly for you.) But seriously, meal planning will help you avoid the temptation of ordering food because you know what’s for dinner back home. Plus, you’ll spend less on groceries when you know exactly what you need to buy for the week, which frees up space in your budget and your fridge.

I know making sacrifices hurts, especially if you’re not used to telling yourself no. But this is a short-term sacrifice for a long-term gain. We are learning good money habits and going after big goals—so that later, you can do as much of that fun stuff (like eating out and traveling) as you want! And I predict you’ll realize during this journey that you can actually be content with less.

4. Build an emergency fund.

If you’re living paycheck to paycheck, chances are, you’re only one layoff or broken HVAC away from a full-blown crisis. That’s why you need an emergency fund! It’s your safety net for those “life happens” moments.

Start by saving $1,000 as fast as you can. That might seem like a lot right now, but once you’ve cut some expenses out of your budget, you’ll be able to save up faster than you think. In fact, most folks are able to save $1,000 in 30 days!

And take it from me, knowing you have this buffer between you and life will help you sleep waaay better at night. Because you know if you get into a jam, you can pay cash—instead of going into debt to cover it . . . which brings me to my next point.

5. Pay off your debt.

Debt keeps you stuck, paying for last year’s Christmas in June and that beach trip in December. It’s one of the biggest reasons you’re living paycheck to paycheck—those payments are eating up your income. But you don’t have to stay in that cycle. It’s time to break free!

Here’s how: First, stop taking on any kind of new debt. Cut up those credit cards. Say no to the buy now, pay later option at checkout. (If you have to split up that sweater into “four easy payments,” you can’t afford it.)

Next, knock out your current debt using the debt snowball. It’s the fastest way to build momentum because you start with your smallest debt and stack up wins quick. I used this method myself to pay off a mountain of debt, and let me tell you, it works.

And just think: How much of your money goes to debt payments every month? That’s how much extra you can have in your budget when your debt is gone! Goodbye, payments. Hello, progress.

6. Increase your income.

If you’ve set a budget and dialed back the spending, but you’re still barely able to make ends meet, you probably need to increase your income.

Are you able to work extra shifts or longer hours? Are you a freelancer who can take on more clients? Do you need to look into getting a better-paying job altogether?

Maybe the answer is taking on a side hustle (or two). Some great options for making extra money are waiting tables, driving for Uber or Lyft, being a barista, or working at a call center. It’s even better if you can use your own skills and interests to serve people.

My favorite side hustles while paying off debt were babysitting, cleaning houses, giving music lessons, dog sitting, building websites, and making wedding cakes. The best part about side hustles is that you can set your own price. And who knows? That side hustle could turn into your full-time hustle. Whatever you choose, the point is to get more cash flowing into your budget.

7. Live below your means.

This one may seem like common sense, but don’t skip over it! Earning more money doesn’t make you a better manager of your money.

Don’t increase your income just to keep living a lifestyle you can’t afford. If you aren’t careful, a bump in pay can make you bump up your standards of living (that’s called lifestyle creep). When you suddenly have more money in your bank account than you’ve ever had before, you start spending more than you ever have before.

Living below your means starts with telling your money what to do—on purpose, every single month. That means making a plan for every dollar, sticking to your budget, and choosing contentment over comparison.

8. Save up for big purchases.

Nothing keeps you stuck in the paycheck-to-paycheck cycle like letting impatience call the shots. When you chase instant gratification (dropping cash on big purchases you didn’t plan for), you’re robbing your future self of peace and progress.

Instead, slow down. If you know something’s coming up (like a tire upgrade or back-to-school expenses), set up a sinking fund and save for it little by little. That way, when the time comes, you’re ready—and your budget isn’t wrecked.

And listen, if you’re still getting your emergency fund in place or working on paying off debt, now’s not the time for pricey vacations, impulse buys or “but it’s on sale!” splurges. You don’t need it right now. Say no today so you can say yes to something better later.

9. Set specific financial goals.

I know firsthand just how hard it is to stop living paycheck to paycheck. But when things get hard, remember your why. I always say: the stronger the why, the stronger the try.

If you’re not already, get clear on your money goals. Whether you want to travel during retirement, give your children a better life, or buy that condo on the beach—having a specific goal in mind keeps you motivated to keep going.

For my husband and I, we knew we had to break the debt cycle because we wanted to create a home for our kids and ourselves where money didn’t create angst. We wanted money to create ease. But maybe you just need to think more short term right now and imagine a life where there’s no fear of overdraft fees or your card getting declined.

Remember your why when you’re working that extra shift delivering groceries, holding back from hitting Add to Cart, and making your own coffee at home. Making big changes with your money and your life is tough. But you are tougher. Let your vision of where you want to be push you to keep going. I promise it’s worth it.

Stop Living Paycheck to Paycheck and Start Getting Ahead

You don’t have to stay stuck in the stress of just getting by. You can break the paycheck-to-paycheck cycle.

Start by giving every dollar a job, cutting spending where you can, and finding ways to boost your income. I’ve been where you are, and I’m telling you: When you get intentional with your money, everything changes.

No matter where you’re at with money, you can get better. That’s why we made the EveryDollar budgeting app!

EveryDollar helps you find extra margin every month so you can start making real money progress, really fast.

Just download the app, answer a few questions, and we’ll build you a personalized plan, based on your situation, to free up margin and make the most of every dollar. Every day. (See where we got the name?)

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Jade Warshaw

Get proven Ramsey answers fast.