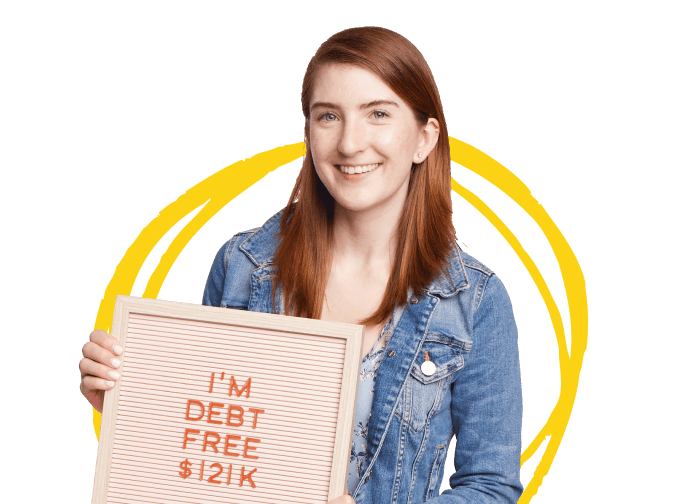

"I paid off $121,000 in 28

months. I feel strong! The

burden is gone!"

All your life, you've been told debt is normal—even good! And that lie has kept you stuck in a cycle of monthly payments. The truth? Debt is normal. And normal is broke. Be weird! Learn how to get rid of debt for good, build lasting wealth, and live and give like no one else.

In Baby Step 2, you’ll kick debt out of your life for good. You’ll knock out every loan and credit card one by one so you can take control of your most powerful wealth-building tool—your income.

On average, families become debt-free in 18–24 months when they use their EveryDollar budget to follow the debt snowball method. You’ll pay off debt from smallest to largest, regardless of interest rates.

Quick wins create momentum. The moment you crush that first debt, something changes inside—you gain traction and you’re unstoppable!

What could you do with your money if you didn't have any payments? Anything you want! You’re free to save for your future and build the life you dream of. Millions have changed their money habits and their legacy. You can too!

The debt snowball method, combined with your EveryDollar budget, is the fastest way to pay off debt. Whether you’ve got student loans, credit card debt, car payments or all of the above, you can get rid of debt—one step at a time.

Save $1,000 for your starter emergency fund—Baby Step 1.

List your debts from smallest to largest, regardless of interest rates.

Throw any extra money you find in your EveryDollar budget at your smallest debt.

Make minimum payments on your other debts until the smallest is gone.

Take what you were paying on the smallest debt and add that to your payment on the next-smallest debt until it’s gone too.

As your debt snowball payment grows, it flattens every debt in its path until you're debt-free!

Pop your numbers into the Debt Snowball Calculator to see your debt-free date. And stay with us—we have a few smart tips below to help you knock it out even faster.

You can’t climb out of a hole by digging out the bottom. That means saying no to more debt! Cut up the credit cards and stop borrowing so your income can finally start working for you.

If you don't tell your money where to go, you'll always wonder where it went. When you budget with EveryDollar, Ramsey’s budgeting app, you could find an average of $3,015 hiding in your spending. That margin gives you more money to throw at your debt.

If you tend to overspend on food, you’re not alone. Now, with grocery prices on the rise, it’s even more important to be intentional about your food budget. Meal planning tames your food budget in two big ways: First, you head to the store with a plan—only buy what you need for the meals you’ve planned. And since you know what you’ll be having for each meal, you’re less tempted to swing by the drive-thru.

Do you have a few things sitting around collecting dust while your debt is collecting interest? Sell what you’re not using and turn all that clutter into cash. You’ll lighten up your space and knock out a balance at the same time.

We’ll be honest: Paying off debt can feel like a grind. But the extra dollars you earn from a side hustle like pet sitting, tutoring or grocery delivery can move your debt-free date closer than you think.

We know it sounds weird to dip into your savings, but that’s what paying off debt is all about—to be weird! Use any nonretirement savings above your $1,000 starter emergency fund (Baby Step 1) to knock out as much debt as you can. Once you’ve kicked debt to the curb, you’ll rebuild your savings in Baby Step 3.

When you’re bogged down with debt and have more month than you do money, it doesn’t make sense to keep investing in your 401(k). Push pause on your contributions and free up your income to throw at your debt. Don’t worry—once you’re debt-free, you can invest even more when you get to Baby Step 4.

Paying off debt is hard work, and not everyone will understand your goal. Make sure you have a few people in your life to cheer you on. And remember—we’re right here to guide you every step of the way. With encouragement on both sides, you’ll stay motivated until you’re debt-free!

"I paid off $121,000 in 28

months. I feel strong! The

burden is gone!"

“Now, we talk more about our money, we make decisions together, and it’s not stressful anymore.”

“Budgeting gives you a true picture of your finances—of your life—so you can pick what you can do and plan all the good stuff.”

“I cried the first time we finished a month and actually had money left over. That had never happened before.”

“We're not stressed anymore. Our journey's in our hands now. We get to choose what we want to do."

"There’s freedom on the other side of debt. You don’t have to live like everyone else. I wanted something different for my family."

Debt payments and a guess-as-you-go budget aren’t getting you where you want to be. It’s time to commit to a better plan. Baby Step 2 is part of Ramsey’s 7 Baby Steps plan that millions of families have used to escape debt and build wealth that lasts. No more guessing about what to do next. The Baby Steps put you in control so you can win with money.

The debt snowball is all about motivation. By paying off your smallest debt first, you get a quick win! Plus, you immediately free up money to tackle the rest of your debt. The debt snowball creates unstoppable momentum to knock out the rest of your debts—like a snowball rolling down a hill!

No. While on Baby Step 2, commit all your energy and resources to getting out of debt—that includes the money you’ve been setting aside for retirement. Concentrate on one goal at a time, and you’ll be more likely to knock out your debt.

Even if you get a company match, push pause on all investing while you're eliminating your debt. Remember, this is only temporary. Once you’re debt-free (and have your full emergency fund), you’ll more than make up for taking a year or two off from investing

If you have two debts that have the same interest rate, just pay off the two bills in order of smallest balance to largest. Bottom line: Pay off the smallest debt first.

The debt snowball method is the best way to get rid of credit card debt. But you also need to stop using credit cards (cut those suckers up!), get on a budget, control your spending, and do whatever you can to pay off your credit cards ASAP. Also, avoid things like balance transfers, personal loans and more credit cards—those will only make your problem way worse.

When prioritizing your debt, tax debt should always be at the very top—even if it’s not the smallest balance. Since the government can take money from you first and ask questions later, you want to get them off your back ASAP! So deal with your back taxes first before you tackle the rest of your debt snowball.

If you have nonretirement money saved up, keep $1,000 of that for a starter emergency fund—Baby Step 1. Then use the rest to pay off nonmortgage debt. Never use retirement funds, because those come with a huge tax hit and early withdrawal penalty.

As soon as your snowball is complete, start piling up cash to build the full emergency fund as quickly as possible

Yes. You should temporarily pause the debt snowball if you use your emergency fund. Just make your minimum payments and rebuild your emergency fund as fast as you can. Once your emergency fund is back to $1,000, restart your debt snowball.

If you’ve got a unique question about paying off debt or working the Baby Steps, try our Ask Ramsey tool, powered by Ramsey AI. And to boost your debt payoff journey even more, create your budget in EveryDollar and get personalized recommendations to speed up your progress!