By

By

Key Takeaways

- To track expenses: Create a budget that includes all your monthly expenses, track any money you earn and spend throughout the month, and set a regular rhythm for tracking.

- There are several ways to track expenses, including pencil and paper, the envelope system, computer spreadsheets and budgeting apps.

- The best way to track expenses is with a budgeting app because it’s more convenient, does the math for you, can connect to your bank, and allows married couples to track expenses together.

Tired of constantly overspending? Budgeting can help you take control of your money. But if you want to actually stick to your budget every month, you have to track your expenses.

Why is tracking expenses throughout the month so important? Because it helps you know where your money is going and how much you have left—so you don’t overspend and send yourself into overdraft.

That said, let’s talk about how to track expenses—step by step—as well as the different expense-tracking methods out there.

How to Track Expenses in 4 Steps

Tracking your expenses isn’t hard, but you do have to make it a habit. And just like other important habits (for example, flossing), it takes repetition to go from trying to remember to do it to doing it regularly.

Here are four steps to help you get into the habit of expense tracking:

1. Create a Budget

Before you can track your expenses, you need to create a budget.

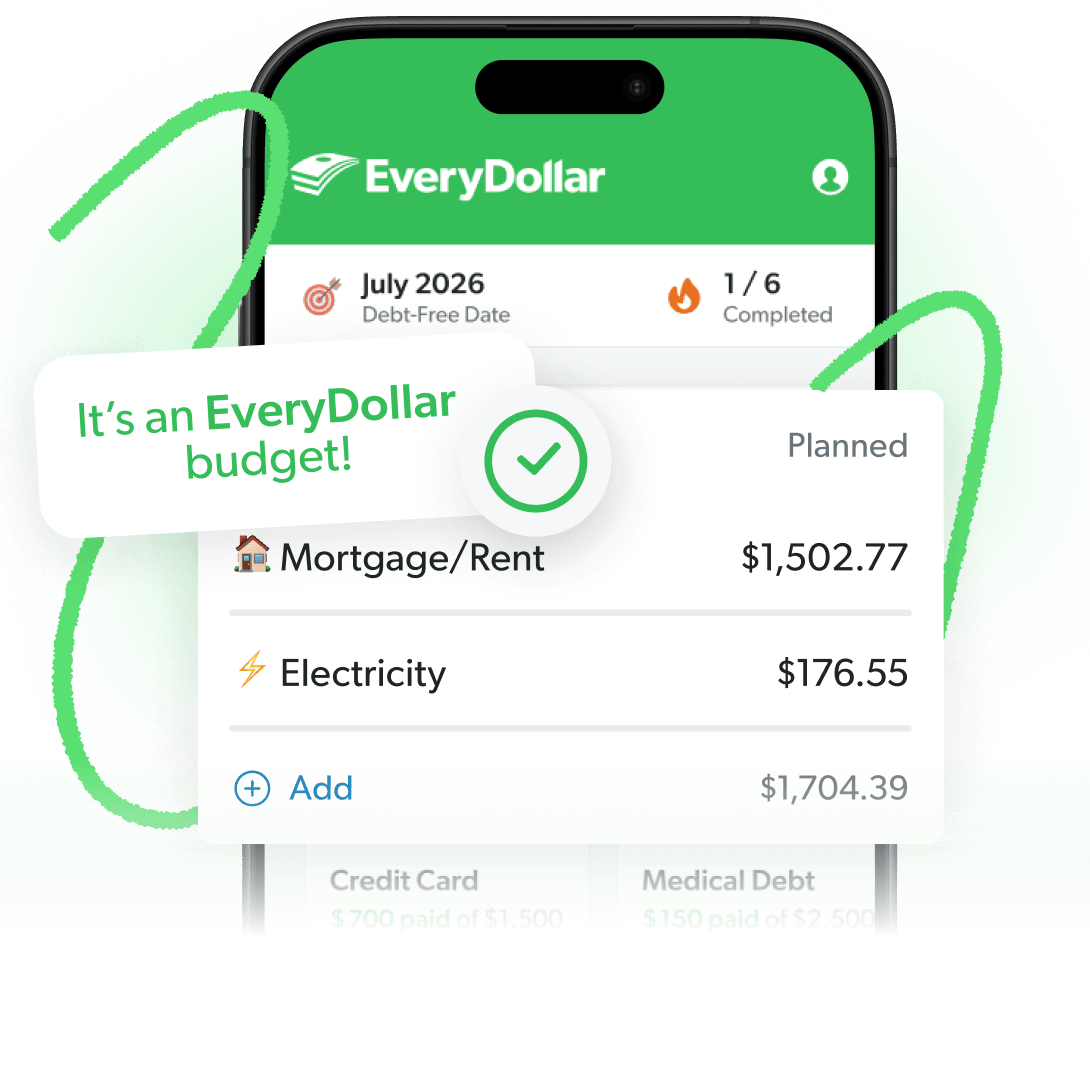

A budget is simply a plan for your money that you make every month. And listen, there are a lot of budgeting methods out there. But the best is a zero-based budget, where you give every dollar that comes in during the month a job to do—whether that’s giving, saving or spending.

If budgeting is new to you, you might be a bit confused. So, let’s talk real quick about how to set up your budget.

List your monthly income.

List out all the money you plan on making this month (that means your regular paychecks and any extras, like that side hustle). Add it all up. This is how much money you have to work with this month!

Got an irregular income? Just look back at what you’ve made the last few months. List the lowest amount as this month’s planned income. We’ll talk more about this in a moment.

List your monthly expenses.

Time to plan for everything you’re paying for this month—both your needs and wants. Don’t know where to start? Open up your bank account and take a look at your transactions from the past couple of months. That’ll give you a good idea of what your monthly expenses are.

When you’re ready to create your budget, list your expenses in this order:

- Giving (10% of your income)

- Savings (depends on your Baby Step)

- Four Walls (food, utilities, shelter/housing and transportation)

- Other essentials (insurance, debt, childcare, etc.)

- Extras (entertainment, restaurants, etc.)

You’ll want to break those categories (giving, savings, food, utilities, etc.) down into individual budget lines that accurately reflect your expenses for the month. For example, under the category Food, you could include a line for groceries and a line for eating out.

The more detailed you are when creating your budget, the easier it’ll be to track your expenses!

Find Margin You Didn’t Know You Had With EveryDollar

The EveryDollar budgeting app helps you find extra money every month so you can beat debt, build wealth, and make progress. Every. Day.

Subtract your income from your expenses.

This should equal zero. If you’ve got money left over, that’s awesome! Put it toward your current Baby Step (the Baby Steps are the proven, guided path to saving, paying off debt, and building wealth). If you’ve got a negative number, lower your planned totals or cut extras until you get zero.

Like we said before, it’s all about giving every single dollar you make a job to do. That way, your money’s working as hard as you.

Now that you’ve set up your budget, you’ve got to keep up with it. That’s where the tracking comes in!

2. Track Any Money You Earn

When your regular paychecks come into your bank account, enter that amount in the income part of your budget. If you make money through a side hustle or you sell some stuff you no longer need, log that income too.

This step is super important if you have an irregular income. Remember, you planned low when you listed your income. So if your income turns out to be more than you planned, this is when you’ll adjust the number. You can add that money to your current money goals or cover some extras in the budget.

Even if you’ve got a steady paycheck, you still need to track your income! For one thing, you can make sure nothing’s off with your paycheck. For another, you’re creating that habit of tracking.

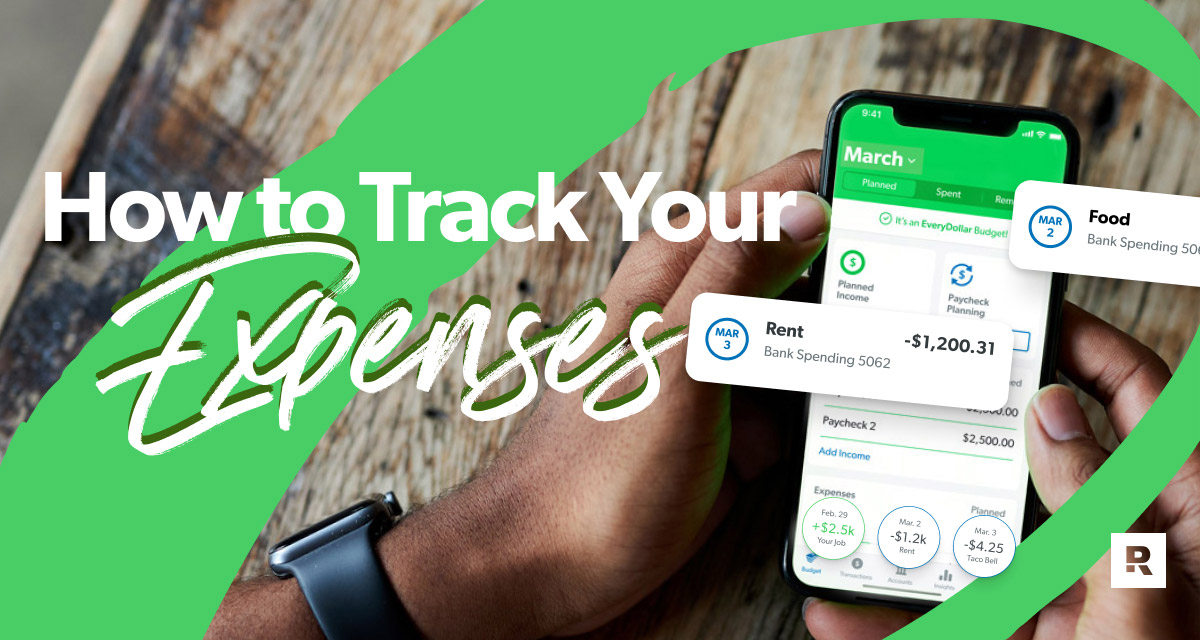

3. Track Any Money You Spend

Track every single transaction. All month long.

When you fill up the gas tank, subtract that expense from your gas budget line. When you pay the rent, subtract that expense from your housing line. When you buy tickets to see your favorite boy band’s reunion tour, subtract that expense from entertainment (or maybe you’ve got a specific budget line just for concerts).

If you spend it, track it. Whether the money’s coming out of your wallet, bank account, PayPal, cash envelope, coin purse or old-fashioned piggy bank . . . you get the picture.

As you track your spending, make sure you’re subtracting too (even better if you’ve got a budgeting app that does the math for you). Then you can see how much you have left in your different budget categories for the month. This is a super important part of tracking—because it’s how you keep yourself from overspending!

4. Set a Regular Rhythm for Tracking

Track your expenses regularly. That might be weekly, daily—or before you leave the grocery store parking lot.

Do whatever works for you and helps you keep up with all your expenses for the month. (If you know those paper receipts are just going to get lost in the bottom of your purse, don’t set yourself up to fail.)

Also, if you’re married, make sure you’re both working from the same budget and tracking expenses. This is great for accountability and communication. That way, neither one of you can say, “I didn’t know you spent most of the entertainment budget on zip-lining tickets. I wanted to sign us up for a couples hip-hop dance class.”

The more you track expenses, the more aware you’ll be of your spending. No more surprise transactions derailing your budget—you’re the one in control.

Expense-Tracking Methods

Okay, so now you know the basic steps to track your expenses. But there are several expense-tracking methods you can use to do these steps. Here are four ways to track your expenses:

Pencil and Paper

Don’t dismiss old-school methods. Whether it’s filling out a budget template or freestyling it on a yellow legal pad, plenty of people love a good paper budget to track expenses.

Pros

- You don’t need access to technology.

- Physically writing things down requires an active brain. (And active brains are really helpful when you’re dealing with money.)

Cons

- It’s a lot having to constantly write down and keep up with the math.

- If you misplace receipts, mix up your numbers, or forget to record some spending, that can lead to a busted budget.

Conclusion

Hey, tracking expenses with pencil and paper is way better than not tracking expenses at all. If it’s the only way you want to go, then go for it!

Here's A Tip

If you want to start out on a paper budget and then move on to some other method, check out our Quick-Start Budget template.

The Envelope System

The envelope system focuses on paying cash for as many things in the budget as you can. You can autodraft expenses like retirement contributions, mortgage payments and some utility bills, and you might send checks or make a debit card payment online for other bills. But you’ll use physical cash for all the expenses you pay for in person.

For this method, you start by labeling some envelopes with the budget lines you want to pay for in cash—like groceries, entertainment and restaurants. (You can also use a special divided wallet.) Then, fill each envelope with the amount of money you budgeted for that particular line.

Pros

- You know exactly when to cut back on spending because you see when the cash in the envelope starts getting low.

- You don’t overspend because when the envelope is empty, you’ve got nothing left to spend. (Your money is essentially tracking itself!)

Cons

- Sometimes paying in cash is inconvenient.

- With the rise of e-commerce, paying cash isn’t always an option.

Conclusion

Physically watching the money leave the envelope inspires a whole new level of responsibility. Even if you go with a different method to track expenses, doing the envelope system with at least some of your budget lines is a great way to manage your money.

Computer Spreadsheets

Okay, let’s talk software, specifically computer spreadsheets, as another way to track expenses.

Pros

- Spreadsheet enthusiasts love all the template options.

- You can customize your budget.

- You can set up your spreadsheet so it does the math for you.

Cons

- Spreadsheet enthusiasts aren’t always married to fellow spreadsheet enthusiasts. This can cause some friction in the money and marriage department.

- Having to physically get to your computer every time you need to track a transaction can be super inconvenient. And if you aren’t regularly entering your expenses, your budget’s not doing you any good—it’s just a spreadsheet full of plans.

Conclusion

If spreadsheets are the only way you (or your spouse) want to budget and handle expense tracking, that’s cool. But know there are more convenient tracking methods out there.

Expense-Tracker Apps (aka Budgeting Apps)

We love a good budgeting app. Seriously. Most of us always have our phones on us—which means we can always have our budgets on us! Brilliant.

Pros

- You can log in on your phone and track your expenses immediately, no matter where you are. So convenient!

- You don’t have to do the math—the app does it for you.

- Budgeting apps usually have loads of features to help you create your budget and keep up with your money—including streaming your bank transactions right to your budget.

- Sharing the same budget with your spouse is super easy.

Cons

- You need access to technology.

- The company who made your app could shut it down (like with the Mint situation), and you could lose your budgeting history.

Conclusion

A budgeting app is the best way to track expenses because it makes it way easier to create a budget, regularly track your expenses, and stay on the same page with your spouse if you’re married. Win, win and win!

Get an Expense Tracker That Works for You

Ready to start tracking your expenses like a pro? Then you need a budgeting method that keeps you accountable—while also being simple enough to stick with.

That’s why we made the EveryDollar budgeting app!

EveryDollar helps you find extra margin every month so you can start making real money progress, really fast. Just download the app, answer a few questions, and we’ll build you a personalized plan, based on your situation, to free up margin and make the most of every dollar. Every day. (See where we got the name?)

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.