Closing Costs in Texas

By

By

Key Takeaways

- Buyers in Texas typically pay 2–6% of the home’s purchase price in closing costs, while sellers often pay 6–10%.1

- Common buyer costs include loan fees, appraisal, inspection and prepaid expenses.

- Sellers usually cover agent commissions, attorney fees and their remaining mortgage balance.

- Some costs—like escrow, title services and notary fees—are shared or negotiable between buyer and seller.

- Buyers can save by skipping lender credits and home warranties, applying for closing cost assistance, and negotiating.

So, you’re on the move in Texas—maybe you're moving from out of state or maybe you're just moving to different zip code. Either way, the deal’s in motion. Your offer’s accepted, the inspection’s done, and closing day is in sight. Now comes the last hurdle before you get those keys: closing costs.

These fees show up in every real estate deal, but they can look different depending on where you live. In Texas, closing costs come with their own price tags and rules. And if you don’t plan for them now, you might end up eating rice and beans for the next 12 months.

In this guide, we’ll go over everything you need to know about closing costs in Texas—like how much they are, who pays for what, and how you can save.

What Are Closing Costs in Texas?

Closing costs are fees people pay for services that switch ownership of a home from the seller to the buyer. The good news is, some closing costs are tax deductible.

We’ve talked about closing costs before, so check out our other article for more general info about closing costs. For now, we’re focusing on closing costs in Texas. Let’s start with the question everyone wants to know: How much are closing costs in Texas?

How Much Are Closing Costs in Texas?

In Texas, the average closing costs for buyers are typically 2–6% of the home’s purchase price. Sellers can expect to pay around 6–10% of the home’s purchase price (including real estate agent commissions).2

So, if you’re selling a house, don’t think you’re off the hook—you may actually have more closing costs than the buyer!

How to Calculate Closing Costs

Calculating closing costs is pretty easy—you just multiply the home’s purchase price by the percent you’ll pay for closing costs. In Texas, the median list price for a home was $375,000 in July 2025.3

If the buyer has to pay 3% for closing costs, that would look like:

$375,000 x 3% = $11,250 closing costs

Now, let’s say the seller’s closing costs are 8%. So, they’re looking at:

$375,000 x 8% = $30,000 closing costs

That’s a big chunk of change. But don’t worry—you won’t get slapped with a huge bill all at once.

When Will You Find Out How Much You Owe?

Having a ballpark number is nice. But when will you find out how much your closing costs are?

Buyers will get an estimate of their closing costs when they apply for a mortgage. They can then take that estimate back to the seller and negotiate to see if the seller will cover any closing costs.

Once the buyer shares that info with the lender, both the buyer and the seller will get their final closing cost numbers at least three business days before they actually close on a house.

Who Pays Closing Costs in Texas?

Like we said, both buyers and sellers pay closing costs in Texas. But they don’t necessarily split them down the middle. Let’s dig into who pays for what—as well as which costs they can share.

Buyer Closing Costs

Buyer closing costs in Texas seem small, but they can add up pretty quickly. Here’s what you’ll have to pay:

Loan Application and Origination Fees

Before they give you a mortgage, lenders will check your finances and process the paperwork. And yes, you’ll still have to pay a fee to cover the cost of setting up the loan.

Credit Report Fee

Your lender will pull your credit report several times during the loan application process to make sure your finances haven’t had a crazy change. You’ll have to pay for each credit report—even if you’re debt-free.

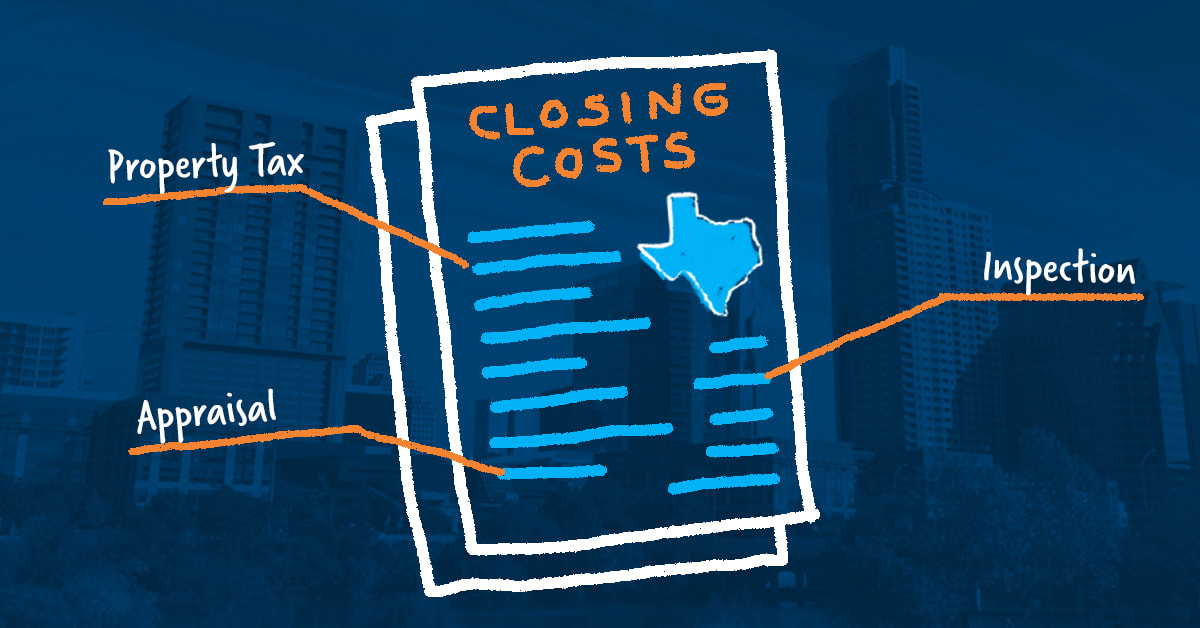

Appraisal Fee

Before closing, you’ll need an appraiser to assess the home’s value. Then you and the seller can negotiate a final sale price based on the home’s fair market value. You’ll have to pay for the appraiser’s services up front.

Home Inspection

Another up-front cost is the home inspection. You may be tempted to skip this step, but don’t! A home inspection is one of the best ways to make sure you’re getting a good deal on the house. And if there are any problems you missed, they should turn up during the inspection.

Survey Fee

Many property owners might not know exactly where their property line is—especially if you’re buying land that’s been handed down for generations. With a professional survey, you’ll know exactly where your new property boundaries are.

Prepaid Costs

Prepaid costs cover a variety of home-buying expenses, like your escrow account, prepaid interest, first year of homeowners insurance, and private mortgage insurance premium.

Discount Points

With mortgage discount points, you pay the lender an up-front fee (essentially prepaid interest) in exchange for a lower interest rate. But you can probably skip this closing cost—mortgage points aren’t always worth it.

Don’t buy or sell without an agent you can trust.

There are RamseyTrusted real estate agents all over the country who are ready to help you win.

Seller Closing Costs

Sellers have fewer closing costs than buyers, and Texas has banned some seller closing costs that other states have—like transfer tax fees. But sellers usually pay one of the biggest closing costs—agent commissions.

Real Estate Agent Commissions

Most real estate agents charge 3% of the home’s sale price for commission. But since sellers traditionally pay their agent and the buyer’s, you’ll likely pay around 6%. We know that’s a lot, but it’s worth it. Your agent will help you negotiate a better deal than you can get alone.

Attorney Fee

Texas doesn’t require an attorney to sit at the closing table with you—but an attorney may still help the lender prepare closing documents. Traditionally, the seller pays the attorney’s fee if there is one.

Homeowners Association Documents

If you live in a homeowners association (HOA), you’ll need to give the buyer a copy of the HOA bylaws. And you’ll both need an estoppel letter, or resale certificate. This document lists monthly dues and any money you owe the HOA before you sell the house.

Reconveyance Fee

If you have a mortgage, your lender has a lien against your house. A reconveyance fee pays to remove this lien so you can sell the home.

Outstanding Bills

This one’s kind of well, duh—but you’d be surprised how many people forget. You have to pay any bills you owe before you can sell your property, whether that’s your Wi-Fi bill or a city fine.

Mortgage Payoff

You’ll have to use the profits from the sale to repay any money you owe your lender. The buyer will then take out their own separate mortgage instead of taking over your old loan.

Seller Concessions

You may agree to pay some buyer closing costs—like prorated property taxes or home inspection fees. But keep in mind, you can only help with a certain amount of buyer closing costs in Texas (or any state for that matter).

How much you can help depends on the buyer’s loan type and down payment, but the maximum is 9% of the purchase price. If you’re already at your limit and still need to sweeten the deal, you may need to make other concessions, like replacing the water heater or installing new cabinets.

Shared Closing Costs

Some closing costs are negotiable in Texas—it doesn’t really matter who pays them, as long as they get paid. For other closing costs, buyers and sellers typically split the costs evenly.

Escrow Fees

Escrow companies help all the money involved in a home sale get where it needs to go. Since both buyers and sellers need these services, you’ll split the costs.

Title Search and Title Insurance

During the title search, a title company checks public records to make sure the seller rightfully owns the property and there are no claims against it. Title insurance protects buyers if a problem turns up later.

The buyer and seller typically split the cost for the title search. Traditionally, sellers in Texas have always bought title insurance for the buyer—but these days, more buyers are paying for their own policies. Either way, the Texas Department of Insurance regulates how much those policies cost.

Municipal Lien Search

A city can put liens on a property for code violations, structures that were built without proper permits, and so on. A municipal lien search finds these violations so the seller can resolve them before closing. Either party can pay for or split this closing cost.

Prorated Property Taxes

Most people pay property taxes every 6–12 months. So, what happens if the home sale occurs in the middle of the payment cycle?

The seller pays property taxes owed before closing. The buyer takes over paying the property taxes after closing. Usually, buyers have to pay a couple months of property taxes up front—called a tax service fee. That way, property taxes don’t get lost in the home-buying shuffle.

Recording Fees

Home mortgages and deeds have to be filed—or recorded—with your county. The buyer pays the recording fees. The seller pays an additional recording fee to update the records after they take care of any issues, like unpaid bills or municipal liens.

Home Warranty

Home warranties are an unnecessary closing cost, and they’re usually not worth it for buyers. The only time we recommend paying for a home warranty is if you’re selling an older house or one in a competitive real estate market.

Notary Fees

Some closing documents need to be notarized—and if the notary charges a fee, the buyer and seller usually split the cost. But Texas has lots of free notaries, so you shouldn’t have to pay for this service on top of all your other closing costs. We recommend checking with a local bank, credit union, government office or library.

Other Costs to Consider

We’ve covered a ton of closing costs you’ll have to pay in Texas. Whew—glad that’s done! But, home buyers, you’re not out of the woods yet. There are other expenses in this process you should be aware of. Let’s cover those next.

Property Taxes

Wait, didn’t we already talk about these? Yes, but only for the first few months. You’ll have to pay these suckers as long as you own the property, so make sure you have a plan to save up for future property taxes.

Home Insurance

Your first year of homeowners insurance is included in your closing costs. But you’ll have to renew your policy each year. Want help finding the right policy for your home? Talk to a RamseyTrusted® insurance provider.

Utilities and Maintenance

Good news—Texas has a lower cost of living than many other states! So home maintenance may cost less if you move there. But that doesn’t mean it’s cheap. Again, you’ll need a plan to pay for these items.

Your monthly budget should include utilities, and your emergency fund can cover unexpected home repairs. But if you’ve got an upcoming expense—like replacing the windows next year—a sinking fund is a great way to start saving for those upgrades.

How to Save on Closing Costs in Texas

Buying and owning a home is expensive, so let’s talk about how buyers can save on closing costs in Texas. Sellers, don’t worry—we’ve got some saving tips for you too.

Lender Credits

Lenders claim lender credits are a smart way to save on closing costs. And a lot of people think the lender pays the closing costs for you. Spoiler alert: They don’t!

With lender credits, the lender fronts you the money for your closing costs—then adds that amount to your mortgage, plus interest. So you actually end up paying more. Lender credits are just a big moneymaking scheme for lenders, which is why we never recommend them.

Now that that’s out of the way, let’s get to some ways you can actually save money on Texas closing costs.

Closing Cost Assistance

Some home buyers may qualify for closing cost assistance from the state of Texas. Let’s check out some of the most popular state assistance programs.

Southeast Texas Housing Finance Corporation (SETH)

SETH closing cost assistance is available in certain communities in southeast Texas through the SETH 5 Star Program—which offers up to 5% of the total loan amount toward your closing costs.

But you have to meet certain criteria for income, home sale price, credit score and more. Plus, with SETH 5 Star, you’ll get stuck with a 30-year mortgage, which we don’t recommend.

Texas Homebuyer Program

The Texas Department of Housing and Community Affairs (TDHCA) offers closing cost assistance to first-time home buyers and veterans through its My First Texas Home program. On the other hand, the My Choice Texas Home program is open to all home buyers.

Again, you’ll have to meet income, sale price and credit score limits. And the My Choice program sticks you with a 30-year loan—so you’ll pay thousands more dollars in loan interest than you’ll save on closing costs.

Are closing cost assistance programs worth it?

Most closing cost assistance programs aren’t worth it. These programs may seem good for you—but they’re better for the lender.

Before you jump at any of these assistance programs, do the math. Are you actually getting the best deal, or are you paying more over time? If it’s the latter, you’re better off saving for closing costs on your own.

Negotiation

Whether you’re a buyer or a seller, your best chance at saving money on closing costs is to negotiate! That way, both parties can work out a compromise that fits their needs. Plus, your real estate agent is an expert negotiator. They can help you get the best deal on closing costs—and the final sale price.

Finding the Best Real Estate Agent

Real estate agents are the key to a smooth home purchase or sale. They really do make all the difference! If you want to hire one of the best real estate agents in all of Texas, make sure they’re a RamseyTrusted agent.

These guys and gals are part of our RamseyTrusted program. We endorse them because we trust them to serve you with excellence. And since they’re local, you can work with an agent who knows your real estate market inside and out.

Find a RamseyTrusted agent in Texas.

Next Steps

- Write down your home-buying budget and how much you've saved for a down payment.

- Get preapproved for a home loan and ask your lender for a loan estimate.

- Make sure you have enough money saved separately from your down payment to cover closing costs.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.