How to Budget With a Low Income

By

Rachel Cruze

By

Rachel Cruze

Key Takeaways

- Budgeting on a low income means giving every dollar a job, covering essentials first, and not spending more than you earn.

- If your income isn’t enough, you’ll need to cut expenses and find ways to bring in more income.

- Many people get off track by skipping the basics, estimating instead of tracking, or leaning on debt.

- Focus on building an emergency fund, avoiding debt, and adjusting your budget as needed.

Somehow, there always seems to be more month than money. Sound familiar? If so, I see you.

Whether you’re stuck in a low-paying job or you’re battling inflation, I know it can be hard to make progress toward your goals—let alone make ends meet—on a lower income. Forget thriving. Maybe you’re just trying to survive.

That’s where a budget comes in.

Here's a Tip

Budgeting when your income is low means making a plan for every dollar you earn, prioritizing your basic needs first, and adjusting your spending so your income covers your expenses.

When money is tight, there’s no room for guessing. Every dollar has to count.

It might not feel like a budget will make much difference—especially on a low income—but it really does. Take a look:

|

Without a Budget |

With a Zero-Based Budget |

|

Money disappears quickly. |

Every dollar has a job. |

|

Bills feel unpredictable. |

Expenses are planned ahead. |

|

You rely on credit cards. |

You avoid debt and overspending. |

|

Money causes constant stress. |

Having a plan gives you clarity and peace. |

|

You make no progress toward goals. |

Small wins add up over time. |

|

Surprise expenses wreck everything. |

You’re prepared and in control. |

This is how you move from just surviving to actually making progress.

So, let’s break down how to make that happen. I’m going to show you three simple steps to budget on a low income, plus some practical tips to help you save more money and make your paycheck go further.

How to Budget With a Low Income (Step-by-Step Guide)

Even if you have a low income, you still can (and should) make a plan for your money. It’s all about working with what you have. And a budget helps you do just that by telling your money where to go each month.

But how exactly do you create a budget when you don’t make a ton of money? The same as everyone else: one step at a time.

Before I get into the nitty-gritty, go ahead and have your bank account pulled up for easy access (you’ll need it in a minute). Also, grab a pencil and paper to write out your budget—or you can use a budgeting app like EveryDollar, which makes it super easy to plug in and adjust your numbers in real time. Okay, ready? Let’s jump in!

Step 1: List your income.

Every budget starts with your income, no matter how much you make. Because you can’t know how much you’re able to spend for the month if you don’t know how much is coming in, right?

Start by listing out all your sources of income. This includes salaries, part-time work, side hustles, stipends, child support, disability, social security—basically any way you get paid each month. And if you work on commission or have an irregular income, just use your lowest monthly income as a place to start (you can always go up from there).

Step 2: List your expenses.

Once you’ve got your total monthly income figured out, your next step is to plan for all your monthly expenses. (This is when you’ll use your bank account to get a better idea of your spending.)

Take care of your Four Walls first.

Before you can budget for the things you want, you’ve got to make sure the basics are taken care of. After setting aside money for giving and saving (depending on what Baby Step you’re on), start by budgeting for what we call the Four Walls: food, utilities, shelter and transportation.

Write down how much you need for your rent or mortgage, as well as an average for bills like electricity and water. What do you usually spend on food each month? What about gas? Don’t sweat trying to get your budget percentages exactly right. Just give it your best estimate.

Then plan for other expenses.

After your Four Walls are covered, be sure to include costs for things like childcare, insurance and debt payments in your budget, as well as other common expenses. How much do you spend on entertainment? How many Target runs do you usually make for household products each month? And you’ll definitely need a miscellaneous category for those random expenses that pop up (because you know they will pop up).

For now, don’t worry about what you think you should be spending in these categories. At this point, you’re just trying to get an idea of what you typically spend each month (and we’ll do some adjusting in a minute).

Budget Priority Table

|

Priority Level |

Category |

Examples |

|

1 |

Four Walls |

Food, utilities, shelter, transportation |

|

2 |

Essentials |

Insurance, childcare |

|

3 |

Financial Goals |

Savings, debt payoff |

|

4 |

Extras |

Dining out, subscriptions |

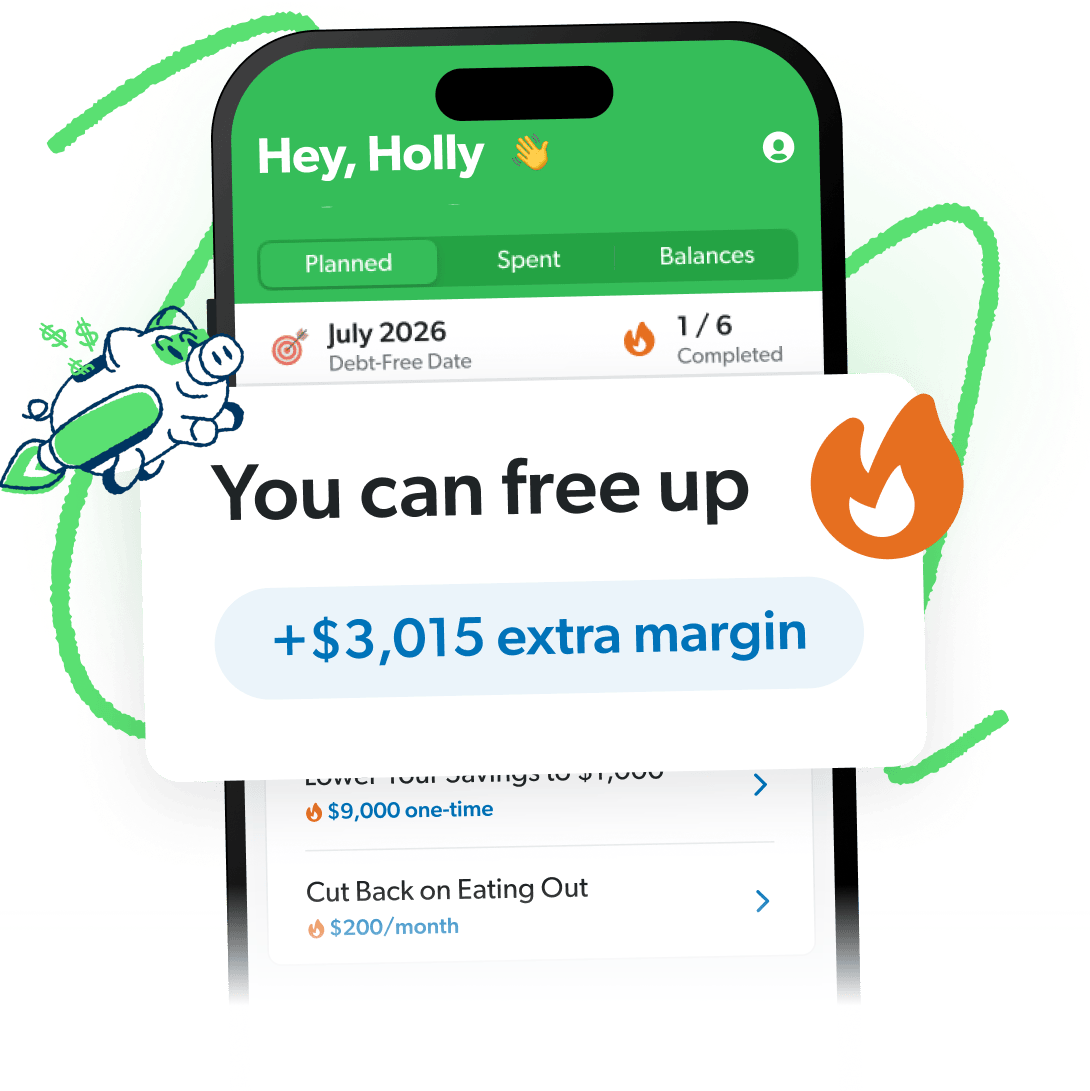

Find Margin You Didn’t Know You Had With EveryDollar

The EveryDollar budgeting app helps you find extra money every month so you can beat debt, build wealth, and make progress. Every. Day.

Step 3: Subtract your expenses from your income.

Zero-based budgeting is hands down the best way to manage your money. When you subtract your expenses from your income, it should equal zero. (If you’re using EveryDollar, it’ll do the math for you.) For example, if you bring in $2,000 a month, your budget should assign all $2,000 to specific categories—like rent, groceries, gas and savings—until you reach zero.

That might sound like you’re spending all your money in one month, but it really just means every dollar you’re making should have a job to do inside your budget—whether it’s giving, saving, spending or paying off debt.

Now, you might get a negative number instead of zero the first time you do this, especially if your income has gone down recently. If that happens, no shame. This is why you’re doing a budget: to stop the overspending before it happens (and to avoid those overdraft fees).

If you want help getting started, try our Budget Calculator to see how your numbers can work.

What Do You Do if Your Income Isn’t Enough to Cover Expenses?

So, you did your zero-based budget, and you realize you don’t have enough money to cover all your expenses for the month. First, take a deep breath. I know it can feel overwhelming when you’re looking at the numbers. But we’re about to do some adjusting to help fix that!

Here’s the deal: You have to be more intentional about your spending and even make some sacrifices—especially if you’ve been relying on debt to fill in the gaps before now. But the good news is, there are plenty of ways you can balance out your budget to get back on track and spend with confidence.

Cut out extras.

First things first, go through your budget and see what costs you can cut out. Do you need all those streaming services? Do you really have to get your nails done every week? These things aren’t bad, but if your budget says no, you have to say no as well.

Skip the restaurants.

Eating out is a huge budget buster! Scale back on restaurant visits to once a week—or cut them out completely if your budget is super tight. Yeah, cooking isn’t as convenient as swinging through the drive-thru, but you’ll save a ton of money. Repeat after me: “We have food at home.”

Don’t buy new clothes.

Listen, I love shopping as much as the next person. But unless your kid has outgrown their clothes or you need some new items because nothing in your closet fits, you can probably get by without buying any new clothes for a while.

Sell your stuff.

Clearing the clutter in your life can help you add more money back into your budget. Just do a sweep of your home and look for things you no longer use or love. Old sports equipment? The gift from your mother-in-law that’s collecting dust in the closet? That extra set of fancy dishes you keep just in case the Queen of England happens to stop by for a meal? It’s time to let these things go and sell your stuff online to make some extra cash.

Save money on expenses.

What about the budget categories that you can’t cut out completely? Here are some ways to save money on those necessary expenses.

Food

- Try meal planning. (I’ve got a great Meal Planner & Grocery Savings Guide that will help!)

- Buy generic products.

- Shop at cheaper grocery stores.

- Use coupon apps.

Utilities

- Replace your air filters.

- Only run appliances (like dishwashers and washing machines) when they’re full.

- Wash clothes on cold.

- Adjust your AC or heat.

Transportation

- Combine your errands to save on gas.

- Join gas rewards programs.

- Use an app that tells you the cheapest gas in the area (like GasBuddy).

- Get rid of your car payment.

Insurance

- Shop around for better policies.

- Raise your deductible (just make sure you’ve got your emergency fund in place first).

- Drop unnecessary coverage. (Here’s a tool to help you know what coverage you need.)

- Bundle your policies to get a better deal.

Entertainment

- Look for free events in your neighborhood or city.

- Take advantage of your local library.

- Try one of these fun activities that won’t bust your budget.

Find ways to increase your income.

If you’ve scaled back all you can on your expenses and you still don’t have enough to make ends meet, you need to figure out how to boost your income. Here are some ideas to help you get started.

Get a side hustle.

From driving for Uber and delivering meals to selling homemade jewelry and tutoring online, there are lots of ways you can use your talents and free time to make some extra money on the side.

Work overtime.

Don’t want to commit to a new side gig? See if you can work more hours or take on extra shifts at your current job. It doesn’t have to be all the time, but having that bonus in your paycheck is definitely worth it.

Freelance.

If you’ve got skills like photography, writing, designing or bookkeeping, there are plenty of opportunities to do some freelance work. You can charge by the hour or a flat rate per project. And the best part is, you get to decide how many projects you take on at a time.

Ask for a raise.

If you feel like your pay doesn’t match the effort you put into your job, try asking for a raise. You’ll have to do some planning before you bust into your leader’s office asking for more money. But if you think you deserve to make more than your current salary, it’s worth starting the conversation.

Switch jobs.

Are you trapped in a job with low pay and little to no opportunities for growth? If that’s the case, it’s probably time to look for another job. Maybe you just need to find a better company. Or maybe you need to switch career paths altogether. Either way, there are plenty of jobs out there that will help you make more money and do work you love—without having to go back to school.

Common Budgeting Mistakes to Avoid on a Low Income

When money is tight, even small mistakes can throw your whole budget off track. But this is something a lot of people struggle with. Here are a few common pitfalls to watch out for:

Not prioritizing your Four Walls

I know I’ve already mentioned this, but it’s important. Before anything else, make sure your basics are covered—food, utilities, shelter and transportation. It can be tempting to keep paying for subscriptions or grabbing takeout, but taking care of your needs first gives you a solid foundation.

Guessing your numbers instead of tracking them

When you’re on a tight budget, every dollar matters. If you’re just estimating what you spend, it’s easy to go over without realizing it. Take a few minutes to check your bank account and use real numbers. You’ll feel more in control right away.

Trying to budget like someone with a higher income

It’s easy to compare your budget to someone else’s, but your situation is unique. Budgeting methods like 50/30/20 don’t always fit when most of your income goes to necessities. Give yourself permission to build a budget that actually works for your life.

Ignoring small expenses

Those little purchases here and there don’t seem like a big deal, but they can add up quickly. Being more aware of the small stuff can free up money you didn’t even realize you had.

Relying on credit cards to fill the gaps

It might feel like a quick fix, but using debt to cover expenses creates more stress down the road. Instead, focus on adjusting your budget and finding ways to make your money stretch further.

Giving up after one bad month

No one gets this perfect on the first try. You’re going to have months where things don’t go as planned, and that’s totally normal. Just make a few adjustments and keep going.

What to Focus on When Budgeting on a Low Income

It’s easy to feel like everything’s urgent, but not everything matters equally. These are the key areas to focus on first so you can stay stable and start making progress (even on a low income).

Get a starter emergency fund.

I know things may be tight, but you still need a safety net. Nothing is more stressful than being broke and having to deal with a very expensive emergency. But an emergency fund will keep you from busting your budget when life throws a curve ball—especially if you’re living paycheck to paycheck. So before you focus on any other goals, make it a priority to save $1,000 for your starter emergency fund. That way, you can rest assured you’ve got enough to cover a new tire or AC unit repair.

If you’re out of debt, your next goal is to build a fully funded emergency fund of three to six months of expenses. That kind of cushion helps protect you from even bigger setbacks—like a job loss or major repair—without having to rely on debt again.

Don’t go into debt.

You might feel tempted to borrow money if you don’t have enough to cover everything you need or want. But trust me, debt only makes your problems worse. Like, way worse. And the payments you’ll have to make will only squeeze your budget even tighter.

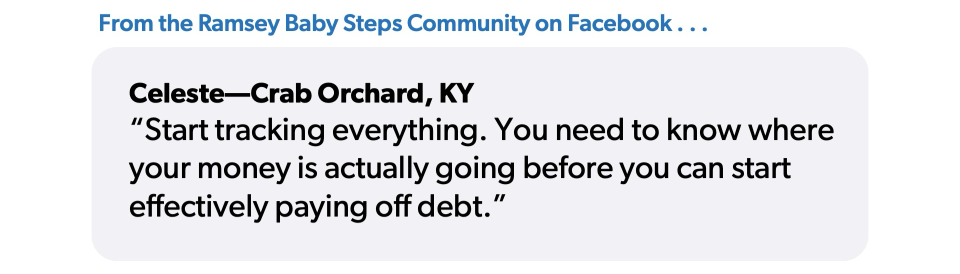

That’s why it’s so important to get clear on where your money is going before you even think about tackling debt. As one member of the Ramsey Baby Steps Community Facebook group put it, “Start tracking everything. You need to know where your money is actually going before you can start effectively paying off debt.”

If you have your emergency fund and you’re making the right decisions with your current income, you won’t have to rely on debt to bail you out. And if you’ve already got debt, paying it off will help you free up your budget that much more!

Adjust your budget.

Low income or not, you can still have control over your money by making and sticking to a budget. And when you do get a higher income and lower your expenses, make sure you adjust your budget—and keep adjusting it month to month. Remember, every dollar should have a job to do, especially when things are tight.

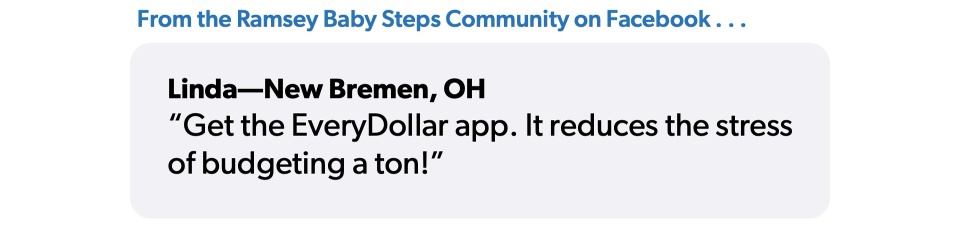

No matter where you’re at with money, you can get better. That’s why we made the EveryDollar budgeting app! As our friend Linda from the Ramsey Baby Steps Community Facebook group says, “Get the EveryDollar app. It reduces the stress of budgeting a ton!”

EveryDollar helps you find extra margin every month so you can start making real money progress really fast. Just download the app, answer a few questions, and we’ll build you a personalized plan based on your situation to free up margin and make the most of every dollar, every day. (See where we got the name?)

Next Steps

- Start your EveryDollar budget by entering your income and covering your Four Walls first.

- Use EveryDollar to track every expense so you don’t overspend when money is tight.

- Budget for your next month ahead of time so every dollar has a job before you spend it.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Rachel Cruze