Fixed vs. Variable Expenses: The Difference and How to Budget for Both

By

Rachel Cruze

By

Rachel Cruze

Key Takeaways

- Fixed expenses usually cost the same each month.

- Variable expenses change in cost each month.

- When you create a budget, don’t start with fixed or variable expenses—start with essential expenses (the Four Walls).

I’ve been teaching people how to budget for years—and budgeting always starts with you listing out two things: your income and then your expenses.

But those expenses are where things can get tricky. That’s because you’ve got fixed expenses (which usually cost the same each month, like rent) and variable expenses (which can change from month to month, like gasoline).

To better understand how fixed and variable expenses affect you, let’s break down what they are, ways to save money on each, and how to get them covered in your budget.

Fixed Expenses Definition

Fixed expenses are the items in your budget that pretty much stay the same amount month after month.

Examples of Fixed Expenses

Common fixed expenses include:

- Mortgage or rent

- Gym memberships

- Most insurances

- Streaming services

- Phone bill

- Internet

- Subscriptions

- Day care

Now, some of these costs go up annually, like how your TV streaming service costs more after your first year (sneaky, sneaky). And some go up if you have a life change, like adding a new line to the phone bill for your teen. But overall, fixed expenses don’t change much each month.

Variable Expenses Definition

Variable expenses change in dollar amount each month, usually based on how much you use them. When it comes to planning, these can be a lot harder to predict than fixed expenses. (But that doesn’t mean you can’t budget ahead! I’ll get to that in a minute.)

Examples of Variable Expenses

Common variable expenses include:

- Water

- Electricity

- Eating out

- Date nights

- Groceries

- Entertainment

- Gasoline

- Car repairs

- Medical bills

- Copays

A couple of those expenses might pop up one month and be gone the next—like if everyone in your family gets their teeth cleaned the same week and you have to dish out cash for all those copays. Planning ahead is how you’ll stay on top of these expenses!

Also, I know a few of those variable expenses, like your electric bill, can be put on a payment plan that evens out the spending over time. But here’s why it’s usually better to pay for the exact amount you use each month instead of an assumed average: You’ll know that any changes you make (like cracking down on your kids leaving lights on all over the house) will make an immediate difference in your next bill.

Which brings me to my next point: Yes, there are things outside our control (like inflation) that affect how much we spend on variable expenses. But the definition itself calls out our part in these changing costs.

How does that play out? Well, if you start taking hot, relaxing baths every day, you’ll pay more for electricity (or gas) and water. If you hit the drive-thru for Chick-fil-A more, you’ll pay more for restaurants. And if you meal plan, you can lower your grocery spending—even with rising food costs.

When it comes to variable (and even fixed) expenses, you’ve got way more control here than you might think!

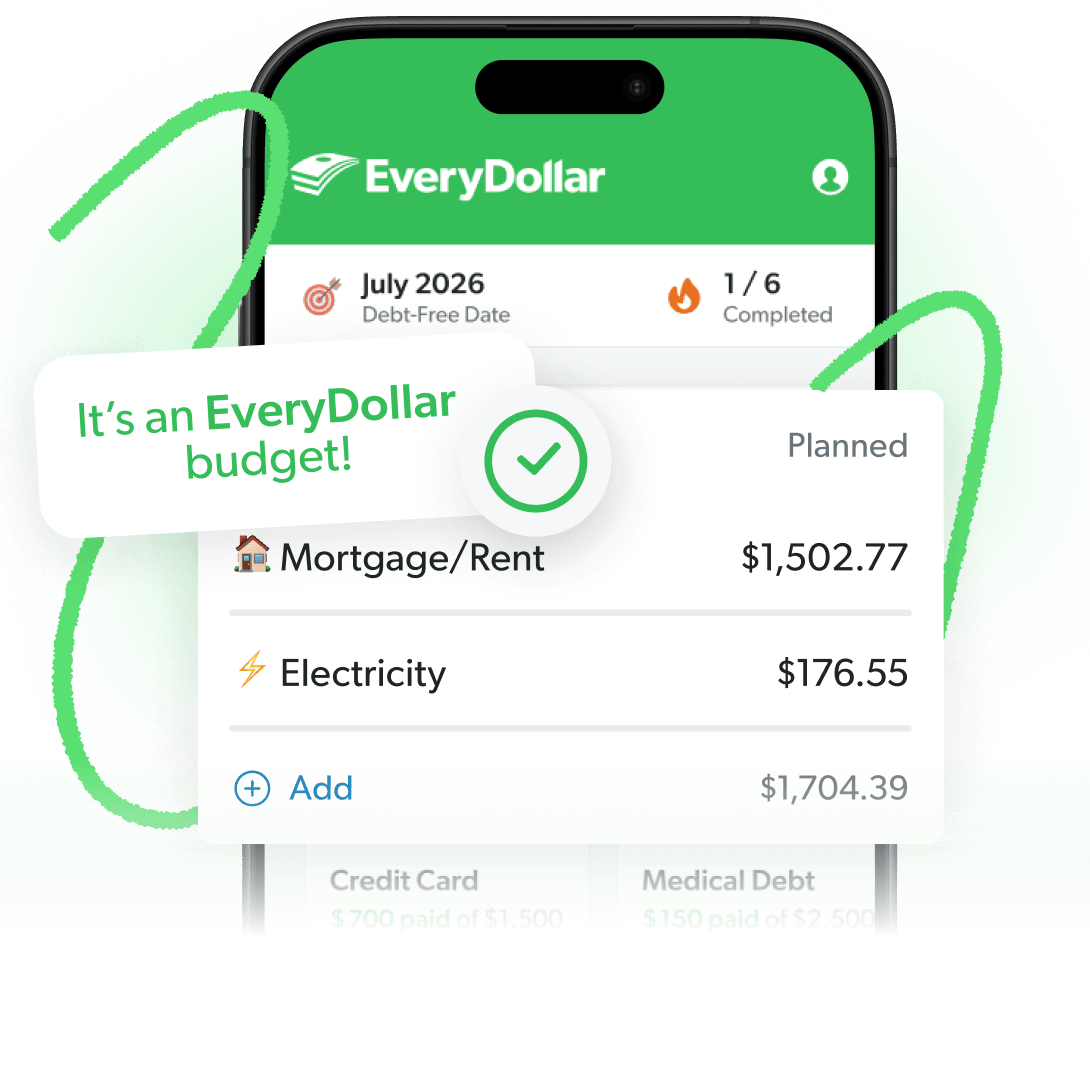

The Budgeting App That Finds Hidden Margin

You’ve got more margin than you think. EveryDollar helps you find it in minutes so you can start making real money progress, really fast.

How to Save on Fixed and Variable Expenses

Speaking of savings tips, let’s run through some ways to save on variable and fixed expenses each month.

Savings Tips for Fixed Expenses

- Try free exercise videos to get fit and healthy without the gym.

- Switch carriers or plans to save on your phone bill.

- Spend less on rent by getting a roommate.

- Check out free TV streaming service options. (The ads are worth the savings!)

- Take our Coverage Checkup to make sure you aren’t overpaying or underinsured.

Savings Tips for Variable Expenses

- Meal plan and shop sales to save on groceries.

- Join gas rewards programs (not credit cards!) at your grocery store to save on transportation.

- Lower your electric bill by lowering the water heater temp.

- Get creative with some cheap (and still fun) date night ideas.

- Order water instead of a soda or tea to spend less at restaurants.

And pro tip: If you want to get super serious about saving, go through your budget and see which expenses you can cut out. Completely.

Maybe you’ll do without for just a month or two. Or maybe you’ll realize you prefer having that money in the bank over having that expense in your budget. Either way, you’ll give your savings goals a great boost.

How to Budget for Fixed and Variable Expenses

Where do fixed expenses and variable expenses come into play when you’re creating your budget?

First, let’s cover the five steps of budgeting:

- List your income. (Plan for everything coming in.)

- List your expenses. (Set planned amounts for everything going out.)

- Subtract your expenses from your income. (This should be zero, meaning you gave every dollar a job.)

- Track your expenses all month long. (See where you still have room to spend—so you can keep from overspending.)

- Make a new budget before the next month begins.

Honestly, fixed expenses are easier to nail down when you’re doing that second step. You can go to your bank account, check last month, and boom—you know what you’ll spend this month.

Variable expenses are harder to figure out, especially that first month. Once again, groceries are a prime example. You probably go shopping a few times a month. So you aren’t glancing at one transaction in your bank account or one receipt. You’re looking back at every Kroger, Publix or ALDI trip from last month and adding them all up to get an idea of what you spend on groceries.

Listen: It usually takes three months of budgeting to get the hang of things. Plan those variable expenses as best as you can to start—it’ll get easier as you go!

Here are five tips to help you budget for both fixed and variable expenses:

1. Start with the Four Walls.

When you’re listing out expenses, don’t start with fixed or variable—start with essential. That means covering your Four Walls (food, utilities, shelter and transportation) first. That’s right: Needs come before wants.

2. Create a miscellaneous budget line.

Plan some money each month in a miscellaneous line. This helps you cover surprise expenses, and you can move money from this line to another if you planned too low for a variable expense.

3. Plan high for variable expenses.

If your electric bill comes in lower than you planned, that’s exciting. Throw some confetti and then throw that extra cash at your current money goal to make it happen that much sooner! (Maybe don’t throw literal confetti, unless you like vacuuming.)

4. Adjust your budget when needed.

Okay, you’re tracking your expenses all month, and a variable expense comes in different from what you planned. What do you do? Don’t ignore it—adjust the budget. That’s why it’s called a planned amount to spend and not a set-in-stone-or-else amount.

5. Get a budgeting app.

Keeping up with it all—the planning, the tracking, the adjusting—is way easier when you’ve got a budgeting app.

That’s why we made the EveryDollar budgeting app! EveryDollar helps you find extra margin every month so you can start making real money progress, really fast.

Just download the app, answer a few questions, and we’ll build you a personalized plan, based on your situation, to free up margin and make the most of every dollar. Every day. (See where we got the name?)

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Rachel Cruze

Get proven Ramsey answers fast.