By

By

Link copied!

Unable to copy link. Please try again.

Key Takeaways

- A budget is simply a plan for your money where every single dollar has a purpose.

- A zero‑based budget is when all your income minus your expenses equals zero. It’s the best method because it puts you in control of your money.

- When allocating money to expenses, budget for your Four Walls first (food, utilities, shelter and transportation).

- Use a budgeting app to create a monthly budget and track your spending.

A budget is a plan for your money. Plain and simple! It’s how you tell your money where to go—rather than wondering where it went. As a matter of fact, I like to call it custom organization for your money because when you budget, you’re getting organized and taking control of the income you work those hard, precious hours to earn. I also call budgeting self-care. Because it’s deciding that your self cares about where your money goes! Every single dollar!

Get expert money advice to reach your money goals faster!

I know this because I’ve lived it. My husband, Sam, and I paid off $460,000 in debt—and having a budget was key to helping us make that happen. That’s why I get so pumped to talk about this topic.

So let’s do this! We already answered “What is a budget?” Now let’s break it down even more: from the types of budgets, to how to make a budget, to some classic budgeting myths that might be holding you back this very moment.

What Makes a Budget “Good”?

So, what really defines a good budget? It isn’t about picking the trendiest method or nailing a certain ratio. A good budget is one that works for you and matches your life, your goals and your money. It keeps you organized, intentional and realistic with your money.

Here’s what you want to see in a solid budget:

- Clarity and simplicity: If your budget feels like it requires a PhD to navigate, it’s not serving you. The best budgets are easy to understand, easy to use, and easy to keep up with.

- Flexibility: Life happens! A good budget can flex and shift with your needs, whether you’re hit with a surprise expense or your goals change. It allows you to be adaptable while still staying in control.

- Accuracy: The numbers have to be real. A great budget is honest about your income and faces all your expenses—no sweeping that coffee shop habit under the rug!

- Alignment with your goals: Want to pay off debt, save for a big trip, or build up your emergency fund? Your budget should put your priorities front and center so your money goes where it matters most.

- Accountability: The right budget keeps you tracking your progress and helps you catch mistakes before they turn into trouble.

The bottom line: A good budget doesn’t look the same for everyone. The best budget is the one you’ll actually use and stick with—because that’s the one that leads to real results.

Ready to take a peek at some of the most popular budgeting methods and find the right fit for you? Let’s do it.

Types of Budgets

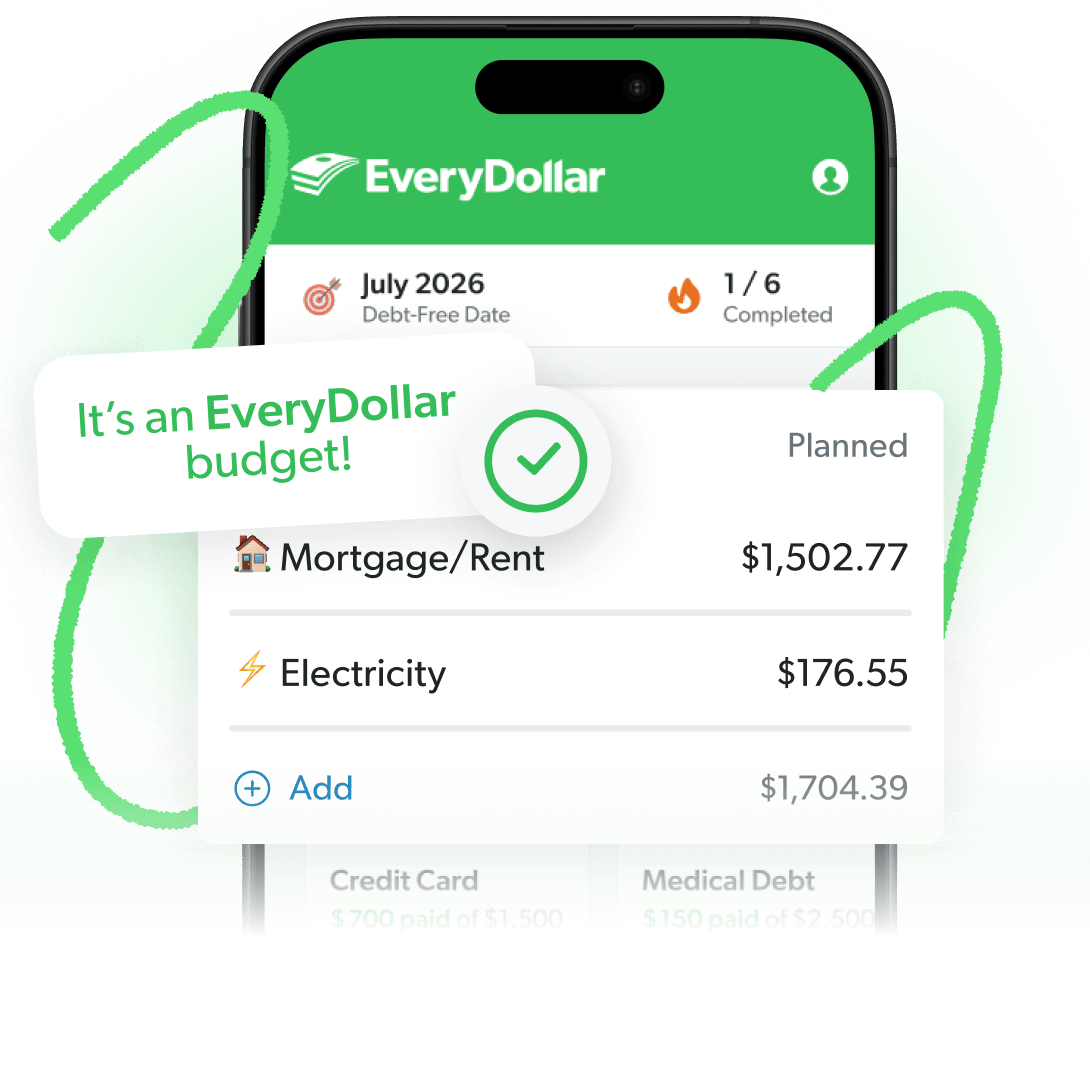

When it comes to ways to budget your money, you’ve got options: Excel spreadsheets, classic pen and paper, or budget apps (like EveryDollar—the app Sam and I use).

You’ve also got different budget methods to sort through, so here are five of the most popular ones out there.

1. 50/30/20 Rule

The 50/30/20 rule says 50% of your income goes to needs, 30% goes to wants, and 20% goes to savings. But hold up, I’ve got a couple problems here.

First off, if you’re staring down $460,000 of debt like I was, you shouldn’t be spending 30% of your income on extras. Now’s the time to cool out in that area.

Also, if you stop to do the math by subtracting average expenses from average income, the average American does not spend 50% on needs. Try 80%. Real talk, this budget method does not work. (Find that math and everything else about the 50/30/20 rule here.)

2. 60% Solution

Here’s another popular method based on budget percentages. With this one, 60% of your budget goes to anything you’ve “committed” to pay for (including wants and needs). You divide up the other 40% like this: 10% to retirement, 10% to long-term savings, 10% to short-term savings, and the last 10% to “fun.”

Okay, first up, I don’t want you lumping needs and wants together. You better be covering groceries before your Netflix subscription. You have to eat. You don’t have to binge-watch The Crown.

But let’s not forget, the average American is spending 80% on needs alone—which includes minimum payments on several kinds of debt, by the way. That’s right. This 60% solution doesn’t hold up, especially if you’ve got debt. And it’s got no plan of attack for getting you out of debt. Thank you, next.

3. Set It and Forget It

Let’s say you write up your first budget, but then you just leave it there all month long. You don’t check in. You don’t track spending. That means you created the plan, but you didn’t follow up or follow through! So what was all that work for?

Using the “set it and forget it” method for budgeting is like writing out the steps to train for a marathon and then never even lacing up your shoes. Making the plan is just the first step—not the whole enchilada. (Don’t worry. We’ll walk through all the steps in just a minute.)

But take it from me—this method won’t work either.

4. Reverse Budgeting

This method starts with savings and then tackles spending. (Perfect name, right?) It says you should start your budget by saving for emergencies, other goals (like a home or travel), and retirement. After that, you budget for essential expenses like housing, utilities, transportation, food, insurance and debt. Finally, you cover nonessentials and fun.

Hey, I’m all about savings being a priority. But I don’t want you putting all these savings goals first if you’ve got debt. (And 77% of Americans—aka most of them—have debt!1)

Build a starter emergency fund, then pay off your nonmortgage debt before you load up your savings and start investing for retirement. Your income is your largest wealth-building tool. When you’re debt-free, you can use that tool to prep for the future, rather than paying off your past.

5. Zero-Based Budgeting

A zero-based budget is when all your income minus all your expenses equals zero. This doesn’t mean you have zero dollars in your bank account (leave a little buffer in there of $100–300). It does mean you’re giving every single dollar a job. All right, now we’re getting somewhere!

I love a zero-based budget because it doesn’t confine your money—it defines your money. It’s you defining how much money you’ll put toward debt and savings each month. It’s you saying what you’ll spend on giving and groceries, on rent and restaurants. A zero-based budget puts you in control of your money. All of it!

And that’s why it’s my favorite—and the best—budget method.

How to Make a Zero-Based Budget

Now it’s time for those budgeting steps I just mentioned.

1. List your income.

Write out every regular paycheck coming in this month for you and your spouse, if you’re married. And don’t forget anything extra. (I see you, side hustlers! And I’m cheering you on.)

Be sure you’re using your take-home pay. That’s your income after taxes and deductions—like health care premiums and anything else your employer automatically pulls out. This is the real number you have to work with each month, not your pre-tax salary.

Then add it all up to see exactly how much money you have to work with. But wait, if you’re like me and hate math, try a budgeting app like EveryDollar. It does all the math for you.

2. List your expenses.

List anything you might possibly spend money on—all the giving, saving and spending happening this month. And when it comes to spending, make sure you cover your Four Walls first (food, utilities, shelter and transportation). Then other essentials. Then the fun stuff. That’s right: Needs come before wants. Every. Time.

And when I say anything, I mean it! From fixed expenses like rent and car payments, to variable expenses like groceries and grandma’s birthday cookout—plan for it all!

3. Subtract your expenses from your income.

Remember, this should equal zero (aka that zero-based budget we just talked about). If you’ve got anything extra, put it toward your current money goal. If you’ve got a negative number, don’t freak out. Here are a few ways to get it to zero.

Short Term:

- Cut some spending. (To Hulu or to Netflix—that is the question.)

- Pick up a side hustle to make more cash.

- Downsize your lifestyle. (Those car payments, am I right?)

Long Term:

- Start looking into higher paying job options.

- Research lower-cost areas to live.

The Budgeting App That Finds Hidden Margin

You’ve got more margin than you think. EveryDollar helps you find it in minutes so you can start making real money progress, really fast.

4. Track your transactions (all month long).

Okay, you did it. You wrote out the plan. Now, it’s time to stick with it.

How? By tracking your transactions! Despite what you saw on Instagram, don’t wait till the end of the month to see what you spend—you should be tracking that all month long.

That means every single time you buy something (even that quick trip to Target for “just one thing”), track it in your budget. This isn’t supposed to make you feel guilty for spending (though it could). It helps you stay aware of your spending so you always know where your money’s going.

That’s right: When you make money, track it to income. When you spend money, track it to the right budget line. This is how you’ll stay on top of your spending so you don’t overspend.

And again, if this seems like a lot of work, it’s not—with EveryDollar! You can connect your bank so the transactions stream right into your budget. All you have to do is drag and drop them to the correct line. It’s kind of like a game. It’s actually oddly satisfying.

Anyway, the point is, track your transactions! You’ll thank yourself at the end of the month when you know exactly where every dollar went (and why).

5. Make a new budget (before the month begins).

Your budget needs to be detailed, realistic and flexible. And making a new budget each month will help you do just that!

Get detailed by covering all those month-specific expenses, like holidays or celebrations.

Make it realistic by planning fair amounts or budget percentages for each category. Prices change. Your budget needs to reflect that. If you aren’t realistic, your budget will be impossible to stick to, and you’ll eventually fall off. So be realistic when you make the next month’s budget, adjusting your planned amounts as you learn what works for your income, your goals and your life.

Finally, be flexible! The truth is, sometimes things pop up that end up being more expensive, like the utility bill or your babysitter. Understand you may have to adjust other categories to rebalance your budget, and that’s okay. Just be sure not to pull from necessary areas like rent or savings to make it work.

To help with this, make it a practice to look back over the previous month to see if you need to make adjustments based on any overspending (or underspending!) you did.

This is your budget. It should reflect your goals and your life. Follow these five steps, and you’ll crush it.

If you need a starting point, check out our Budget Calculator.

Budget Calculator

Enter your income and the calculator will show the national averages for most budget categories as a starting point. A few of these are recommendations (like giving). Most just reflect average spending (like debt). Don't have debt? Yay! Move that money to your current money goal.

Income

Expenses

Difference

Total Expenses

$0.00What a Budget Is and What It Is Not (Aka Budgeting Myths)

You can’t really answer “What is a budget?” without also talking about what it isn’t. Yep, I’m going to point out (and throw out) some popular budget myths right quick.

Budget Myth 1: Budgets are just for people who are bad with money.

Budgeting isn’t just for “those” people. It’s for you.

I don’t care if you’re $460,000 in debt or sitting pretty as a millionaire—you should budget. Even if you’re doing “just fine” with your personal finances, you should budget.

Remember, budgeting is self-care. We all work hard for our money. We should care about where it goes. A zero-based budget is how you take real control of your money so you can make real progress with your money.

If you make and spend money, you should budget. And listen, there’s even a trend called loud budgeting where you let friends and family members know you’re taking charge of your money!

Budget Myth 2: Budgeters have to be good at math.

You don’t have to be a nerd to make a great budget. Money is less about math and more about mindset. Budgeting every month is about getting that mindset right and building a habit that’ll literally change your relationship with money—for good.

Also, you don’t have to do all the math! Do yourself a favor and get EveryDollar. This budget app will make it easy to set up—and keep up with—your budget.

Budget Myth 3: Budgeters don’t have any fun.

Listen, budgeting doesn’t mean you never spend money on fun. It means you plan that fun spending—and you do it after you’ve covered the necessities. Because it isn’t fun to overdraft or worry your card will get declined when you’re trying to buy a four-pack of Angel Soft. Trust me.

But it is fun to treat yourself guilt-free when you know it’s in the budget.

Those are just a few of the budgeting excuses I’ve heard. And none of them hold up. If you’ve fallen for any of them in the past, it’s time to move past that. Right now!

Here's A Tip

Learn how to get past the budgeting lies that are holding you back and start making real progress with your money in my Quick Read, Money’s Not a Math Problem.

How Budgeting Helps You Save for the Future

Let’s be real: Saving for the future can feel like climbing Mount Everest in a pair of flip-flops. But that’s where budgeting swoops in to save the day (and your piggy bank).

When you give each dollar a job (including saving for emergencies, future vacations or even that dream home) you start turning those “someday” goals into actual line items. Suddenly, setting aside money for a down payment or a car doesn’t feel impossible. It just becomes part of the plan.

Break down big purchases—like that trip to Paris or holiday gifts. Tuck away a set amount each month and watch your savings stack up, little by little. That's called a sinking fund! (And yes, a vacation sinking fund is totally okay—even if you're just dreaming of hitting Dollywood.)

Don’t stress about starting big. Maybe it’s $10 a week right now. Maybe it’s $100 next month. The magic is in consistently setting money aside—even if it feels small. Trust me, those little steps carry you a long way.

Buckets and Sinking Funds: Making Savings Goals Easier

Savings buckets (also called sinking funds) makes big goals way less intimidating. In EveryDollar, you can turn any budget line item into a “fund” (which is essentially a sinking fund). The balance automatically carries over from month to month, making it perfect for saving for specific goals like:

- Christmas gifts

- Vacations

- Car insurance premiums

- Property taxes

- Any other irregular or large expenses

Funds work by dividing up your savings into clear, specific categories. Each month, you move a set amount into each fund, like a vacation fund, a holiday gifts fund or even a car repair fund. Let’s say every month, you put $100 aside for your dream getaway, $50 for December festivities, and $50 for car repairs. You’re telling every dollar exactly where to go so you’re not left scrambling when expenses pop up.

The beauty of this method is that you treat these savings just like bills you have to pay. And when it’s time to book that trip or fix your car, you’ve already set money aside.

Why Budgeting Is So Important

Budgeting isn’t just crunching numbers or tracking receipts. It’s about taking control. Knowing exactly where your money is going brings a sense of relief, especially when life throws a curveball.

You work too hard to just wonder where your money goes every single month. That’s life without a budget. Your paycheck comes in and—lickety-split—it’s gone. But you don’t have to live like that.

That’s why we made the EveryDollar budgeting app! EveryDollar helps you find extra margin every month so you can start making real money progress, really fast.

Just download the app, answer a few questions, and we’ll build you a personalized plan, based on your situation, to free up margin and make the most of every dollar, every day. (See where we got the name?)

Then, give yourself three months to get the hang of it—because nobody starts off with a perfect budget. But the work is worth it. You’re about to be calling the shots with your money. And there is nothing in the world like that feeling.

Next Steps

- If you want to get your numbers down with pencil and paper first, download our free Quick-Start Budget template.

- Then, make everything way easier by downloading EveryDollar to set up (and keep up with) your monthly budget. Plus, it helps you find extra margin every month!

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Jade Warshaw

Get proven Ramsey answers fast.