What Is Passive Income? How It Works and How to Build It

16 MIN READ | JUN 12, 2026

By

By

Link copied!

Unable to copy link. Please try again.

Key Takeaways

- Passive income is money you earn from assets, investments or systems with little daily effort after putting in the up-front work.

- The most common types include dividend mutual funds, rental properties (which are best paid for in cash), digital products, REITs and high-yield savings accounts.

- Passive income often takes time to grow and may start as a side hustle (like digital products or affiliate marketing), but it can add up over time depending on the strategy you choose.

- Passive income works best after you have steady active income, are out of consumer debt, have a fully funded emergency fund, and are consistently investing for retirement.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

Ramsey Solutions is a paid, non-client promoter of participating pros.

Dreaming of early retirement? Or maybe you just want to earn enough money to cover your needs and a few more of your wants? Yeah, those are some great dreams—and they’re well within reach if you’re starting to think bigger than just the income that comes with your nine-to-five. That’s exactly where passive income comes in.

Here's A Tip

Passive income is money you earn from assets, investments or systems that take little day-to-day effort once they’re up and running. Common sources include dividend-paying mutual funds, rental properties, digital products, royalties and REITs. Unlike a paycheck, passive income doesn’t stop when you stop working.

Keep Boosting Your Investing Know-How

Every two weeks, the Ramsey Investing Newsletter will send you practical insights, easy-to-use resources, and the latest investing news. All explained in plain English.

The advice you’ll find on the internet makes passive income sound like a magic trick that’ll make you rich overnight. It’s not. It requires time and money to get started. And building passive income depends on which Baby Step you’re on. If you’re still walking through Baby Steps 1–6, focus on that. It’s not time to start building a real estate portfolio.

This article covers what passive income actually is (and isn’t), the best ways to build it, when to start, and how taxes work.

What Is Passive Income (and What Isn’t)?

Passive income is money you earn from assets, investments or systems that can run with little daily effort on your part. Note that we didn’t say no effort at all. Earning passive income isn’t a gig where you can just sit on your butt and make money fast. You’ll need to put in the work—at least on the front end. So if you’re expecting passive income to be some kind of get-rich-quick thing, you’re out of luck.

Most passive income ideas—like building a blog or an app—take time and money to get up and running. But if you play your cards right, they could eventually earn you money while you sleep. And that could boost your progress on the Baby Steps.

Passive vs. Active Income: What’s the Difference?

Before you start building passive income, it helps to understand how it’s different from the income you’re probably used to earning.

Active income is money you make by actively working. If you stop working, the income stops too. This includes your paycheck from a job, freelance work, commissions, overtime and side hustles.

Passive income, on the other hand, is money you earn with less day-to-day effort after the up-front work is done. That could mean investing money, creating a digital product once and selling it repeatedly, or owning an asset—like a rental property—that keeps earning even when you’re not working.

That said, passive income isn’t truly hands-off. Most passive income streams require:

- Time, money or effort up front

- Occasional maintenance or oversight

- Patience while the income grows

For most people, active income comes first. It pays the bills, helps you get out of debt, and gives you the margin to save and invest. Passive income can help you as you walk through the Baby Steps, but you can really kick it into gear after you’re on solid financial footing and have more money to invest. Once you’ve built a passive income stream, it grows steadily in the background.

Active Income vs. Passive Income at a Glance

|

Active Income |

Passive Income |

|

You earn money by actively working. |

You earn money from up-front work or investments. |

|

Income stops when you stop working. |

Income can continue with less day-to-day effort. |

|

You’re paid for your time, effort or output. |

You’re paid from assets, systems or investments. |

|

There’s usually immediate and predictable pay. |

Pay is often slow to start and less predictable at first. |

|

You’re limited by hours in the day. |

Income can grow without working more hours. |

|

Examples: salary, hourly wages, freelancing, side hustles |

Examples: dividends, rental income, digital products |

The IRS defines passive income more narrowly than most people do. IRS Publication 925 says that passive activity is a trade or business activity in which you don’t materially participate.1 (In other words, you aren’t using any elbow grease to earn the income.) Many people classify dividends, interest and royalties as passive income, but the IRS call this portfolio income. When tax time rolls around, you'll have a few extra hoops to jump through to report passive income correctly. (More on that in the tax section).

But in everyday conversation (and throughout most of this article) “passive income” simply means money that comes in without you trading hours for it every day.

Who Passive Income Is (and Isn’t) Right For

Passive income can be a powerful wealth-building tool—but only when the timing is right. Some passive income streams only make sense when you’re on Baby Step 7, while others can be helpful while saving and paying off debt. Passive income may be a good fit for you if you:

- Have steady active income coming in

- Are working to pay off consumer debt or build an emergency fund

- Want to build extra income without taking on another job

On the other hand, passive income is not a good fit (yet) if you:

- Are trying to use it as a shortcut to fix money problems

- Are still relying on debt to pay bills or don’t have savings set aside

- Expect quick or guaranteed returns

- Need immediate income to cover basic expenses

What Are the Best Ways to Make Passive Income?

The best ways to make passive income include dividend-paying mutual funds, rental properties (paid in cash), digital products, intellectual property licensing, affiliate marketing, REITs or high-yield savings accounts. Each one takes different amounts of time and money to get started.

Dividend mutual funds

Some companies share part of their profits with investors. When you own dividend-paying mutual funds in a brokerage account, you can get regular payments just for leaving your money invested. No clocking in, no boss—just patience. Keep in mind though: You should only invest in dividend-paying funds with a brokerage account after you’ve maxed out your tax-advantaged retirement accounts and have paid off your house.

Dividend funds can have payouts as high as 8%, but many of them will earn you 1% or less.2 Over the long haul, that isn’t a great source of passive income unless you have lots of money to invest. Think about it: If you invested $100,000 in dividend-paying mutual funds that earned 1.25%, you’d only get about $1,250 per year ($104 per month) of passive income before taxes.

Rental properties

A rental property makes money when tenants pay rent each month. Sounds great—but it’s not totally hands-off. You’ll need money up front to purchase a rental property, and you may still get the occasional phone call about a leaky faucet at the worst possible time. Just remember: Always pay cash for rental property and never go into debt to buy it. That’s why rental income makes the most sense once you’re out of debt (including your mortgage) and on solid financial footing.

Going into debt to buy a rental property doesn’t just reduce your profit—it turns a wealth-building asset into a risk. If tenants stop paying or the property sits vacant, you’ll still have to pay the mortgage. If you can’t pay the mortgage without rent coming in, your rental property could end up in foreclosure. That’s no fun for anyone.

Sure, it’ll take some time to save the money to buy a rental property with cash, but once you do, all the cash it generates will be yours!

Digital products

Digital products are things you create once and sell again and again—like e-books, online courses or downloadable guides. They take time and effort to build, but once they’re finished, you’re not starting from scratch every time someone clicks Buy. That’s where the passive part kicks in.

Intellectual property licensing

If you create something like music, photos, artwork or written content, you may be able to license it for others to use. Each time someone pays to use your work, you earn money without having to recreate it. This kind of income often builds slowly, but it can add up over time.

Affiliate marketing

Affiliate marketing is when you earn money by recommending products or services through platforms like blog posts, videos or social media content. When someone buys through your recommendation, you earn a commission. But to earn meaningful income, you typically need a large, engaged audience. Building that kind of following takes time, and it doesn’t happen for most people who try. And even after you have an audience, affiliate marketing usually requires ongoing content to keep income steady. Still, for those who do build trust and reach, affiliate marketing can create income while you’re doing literally anything else.

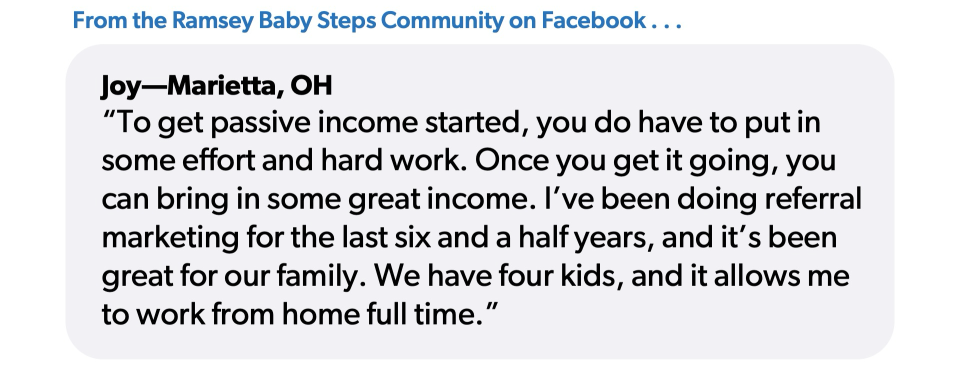

As one member of THE Ramsey Baby Steps Community Facebook group shared, “To get passive income started, you do have to put in some effort and hard work. Once you get it going, you can bring in some great income. I’ve been doing referral marketing for the last six and a half years, and it’s been great for our family. We have four kids, and it allows me to work from home full time.”

Real estate investment trusts (REITs)

A real estate investment trust (REIT) lets you invest in real estate without buying an actual piece of property. REITs pool money from multiple investors to buy income-producing real estate, like apartment complexes, office buildings or shopping centers. By law, REITs must pay out at least 90% of their taxable income to shareholders as dividends, which makes them a decent passive income option.3 This usually translates to higher dividends than mutual funds.

REITs can be a good option for people on Baby Step 7 who have maxed out retirement accounts. But beware: Some REITs use debt to buy properties, which can make them risky.

High-yield savings accounts

A high-yield savings account (HYSA) earns way more interest than a standard savings or money market account—sometimes up to ten times as much! Online banks can offer interest rates around 3% because they have lower overhead than brick-and-mortar banks. Compared to other options, this won’t be a big moneymaker—3% is a pretty small return. But an HYSA is the smartest place to park your emergency fund while it grows. It’s also the only passive income stream that makes sense across all Baby Steps.

When Should You Start Building Passive Income?

If you’re looking to build a passive income stream that requires time but not much money, you can start wherever you are in the Baby Steps. Passive income can help you move through the Baby Steps more quickly.

But for passive income streams with higher up-front costs, it’s best to start once you’re on Baby Step 4 or later. Before that, you should focus your time and money on getting out of debt and saving up an emergency fund.

For instance, if you have consumer debt at 18–29% interest, paying that off is a guaranteed return that’s higher than what you could earn with a passive income stream. But this goes for all debt (even if the interest rate is low). You shouldn’t chase passive income while you’re in debt.

And if you don’t have an emergency fund, the first unexpected expense (car repair, medical bill, job loss) will force you to cash out your investments at the worst possible time. Your emergency fund helps protect your passive income. It absorbs big surprise expenses so you don’t have to sell your investments to pay for them.

Here’s how the Baby Steps work with passive income.

- Baby Steps 1–2: Focus on saving your $1,000 starter emergency fund and working the debt snowball. You can start a passive income stream that requires time but not a lot of money. Think of it like starting a side hustle to fuel your debt snowball.

- Baby Step 3: Build your fully funded emergency fund (3–6 months of expenses). Park it in a high-yield savings account, which will give you a little bit of passive income.

- Baby Step 4: Invest 15% of your household income for retirement. This is where passive income (through investing) officially starts.

- Baby Steps 5–6: Keep saving for retirement, save for your kids’ college, and pay off your house. You can still use no- or low-cost passive income streams to help with these goals.

- Baby Step 7: Build wealth and give generously. Once your house is paid off and you’ve maxed out your retirement accounts, this is when you can start investing in rental properties (bought with cash), REITs and taxable brokerage accounts.

How Do Beginners Start Building Passive Income?

If you’re brand new to passive income, here’s a five-step framework that can get you started.

Step 1: Get the foundation right. Pay off consumer debt (Baby Steps 1–2)—and use low-cost passive income streams if possible. Build a fully funded emergency fund (Baby Step 3), then start investing 15% for retirement (Baby Step 4). Setting a solid foundation will get you to a place where passive income will actually work.

Step 2: Open a high-yield savings account. Move your emergency fund into an account earning 3% or more. That’ll give you zero-risk passive income on money you already have.

Step 3: Start a side hustle with passive income potential. A side hustle, like a digital product you spend time working on, brings in active income now, but some side hustles can become passive income later.

Step 4: Once you’ve paid off your house, max out your retirement accounts first. Your 401(k) and Roth IRA are the most tax-friendly passive income engines you have. Use them before opening a taxable brokerage account.

Step 5: Pick one stream and start small. Don’t try to build multiple passive income streams at once. Pick the one that fits your current Baby Step and your skills.

What Are the Benefits of Passive Income?

Your income is your greatest wealth-building tool. But for most of us, that income requires working 40 hours a week. Even if you love your work, you probably wouldn’t mind earning some extra cash without punching the clock at another job. Building passive income adds a second source of income to your financial plan—one that keeps bringing in money even if your active income stops.

Here’s what building a passive income stream can do for you:

- It can increase your net worth over time and allow you to retire early.

- It frees up time you would’ve been spent working more hours.

- It protects you from a complete loss of income if you lose your job.

- It can boost your savings.

- It can add margin to your budget—even if it’s a small income stream.

How Long Does It Take to Build Passive Income?

Some passive income can start showing up pretty quickly. Interest from a high-yield savings account or dividends from investments may begin within weeks or months.

But it usually takes years to build steady income from digital products, rental properties or affiliate marketing. That slower start is normal. Passive income almost always grows gradually. But when you stay consistent, reinvest what you earn, and give it time, those income streams can become more dependable in the long run.

There’s no one-size-fits-all timeline for passive income. How long it takes depends on what you choose, how much time or money you put in up front, and how consistent you are with it.

How Much Money Can I Make With Passive Income?

Some passive income streams can bring in thousands a month, while others could be less than $100.

For dividend funds, you could earn anywhere from 1% to 8% on your investment, and the exact dollar amount depends on how much you invest. For instance, you could expect a $30,000 investment to earn you anywhere from $300 to $2,400 per year. That’s not much. And if you put your money in a high-yield savings account, you’d have to invest roughly $400,000 at 3% interest just to earn $1,000 a month.

On the other hand, a single paid-off rental property could earn you well over $1,000 a month. And it’s a pretty popular way to earn passive income. According to the U.S. Census Bureau, individual investors own 11.2 million rental properties in the U.S.4

Now, you could earn tens of thousands of dollars from a digital product or course that hits the right audience. Most people don’t reach that level of income—but if you like the work and have a knack for spotting great opportunities, go for it!

How Is Passive Income Taxed?

As your passive income grows, it’s important to remember that extra income comes with extra responsibility—especially when it comes to taxes.

First, let’s get the IRS definition straight. According to IRS Publication 925, “Passive activity generally means trade or business activity in which you do not materially participate.” Under the IRS’s framework, rental real estate is typically treated as passive activity, but if you actively manage your rental and your income is below $100,000, you may be able to deduct up to $25,000 in loses from your ordinary income.5

Most forms of passive income are taxed as ordinary income on your tax return. For example, if you earn interest from a high-yield savings accounts or get investment dividends, they’ll be taxed as ordinary income.

But not all dividends are taxed as ordinary income. Some dividend mutual funds pay “qualified dividends,” which are taxed at the long-term capital gains rate: 0%, 15% or 20%, depending on your taxable income.6 You’ll need to check out your specific fund to see if it includes qualified dividends. The long-term capital gains rate is much lower than ordinary income tax rates for most people. Unqualified dividends (from REITs, for example) are taxed as ordinary income.

Taxes can get really complicated really fast—especially if you have multiple streams of passive income. If you have questions about the taxes you might owe on your passive income, talk to a RamseyTrusted® tax pro. They can help you understand how much you owe and how to get your taxes done right!

Where Does Passive Income Fit in Your Financial Plan?

Passive income isn’t about shortcuts or getting rich fast. It’s about building smart, steady income streams on top of a strong financial foundation. When you choose the right method for your current Baby Step, passive income can become a helpful tool that supports your long-term goals without adding more stress or work hours to your week.

And sometimes the fastest way to feel like you have more money isn’t adding another income stream at all—it’s taking control of the money you already have. A clear budget can free up cash, reduce stress, and help you decide which passive income ideas make sense for your goals. Our budgeting app, EveryDollar, makes it easy to see where your money’s going so you can put it to work toward your goals.

Next Steps

- Check which Baby Step you’re on—that tells you which passive income streams make sense right now and which ones to skip until later.

- If you need extra income now to pay off debt or build your emergency fund faster, start a side hustle.

- Move your savings into a high-yield savings account earning 3% or more. That’s immediate passive income on money you already have.

- If you’re on Baby Step 4 and ready to invest, or on Baby Step 7 and interested in passive income options, connect with a SmartVestor Pro to build a plan.

This article provides general guidelines about investing topics. Your situation may be unique. To discuss a plan for your situation, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

-

What does the IRS consider passive income?

-

The IRS defines passive income under Publication 925 as income from “trade or business activity in which you do not materially participate”—most commonly rental real estate.1 Dividends, interest and royalties are considered portfolio income under IRS rules—even though most people still call them passive income.

-

How can I make $1,000 a month in passive income?

-

A paid-off rental property can usually net $1,000 a month after all expenses are paid. To earn $1,000 a month in a high-yield savings account (HYSA) with a 3% interest rate, you’d need to have $400,000 in the account. You could also stack smaller income streams—like affiliate marketing, a digital product and HYSA interest—to reach $1,000 a month. There isn’t a shortcut. Passive income requires time and money to get started.

-

Does passive income affect Social Security?

-

Passive income usually doesn’t affect Social Security retirement benefits. Social Security only considers wages (not investment or rental income) when calculating benefits.

-

Can you build passive income with no money to start?

-

Yes, but you’ll still need to invest your time and energy to get them going. Zero- or low-cost passive income options include: creating and selling digital products (e-books, templates, courses) using skills you already have, building content (blog, YouTube, social media) that earns ad revenue, and licensing creative work you’ve already produced. None of these are fast.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions