Quiz

Are You Ready to Work With a Pro?

Get advice on when to get an investment pro in your corner.

Learn about different types of financial advisors in Florida, their services, what they cost, and how to find the right one for you.

Dave Ramsey and his team founded the SmartVestor program to connect people with pros who lead with the heart of a teacher. Find out how a Florida SmartVestor Pro can support your financial journey.

Are you an investing pro? Learn about our program.

Ramsey Solutions is a paid, non-client promoter of participating pros.

Florida is home to plenty of advisors, who can help with anything from investment and retirement planning to wealth management. These free tools are designed to help you find the right type of pro at the right time.

Finding the best Florida financial advisor for you doesn’t have to be intimidating!

Our free guide will walk you through what to ask each pro you interview.

Sources: 1Census.gov 2Consumer Affairs 3Realtor.com 4FLHealthCharts 5SSA.gov

Florida financial advisors charge a variety of prices depending on the services they offer and the pricing structure they use. Some of the most common fee structures include:

Assets Under Management or AUM-based advisors charge a percentage (usually around 1%) of the assets they manage for you.

Flat-fee advisors charge a fixed rate for their services, which can range from several hundred to several thousand dollars.

Commission-based advisors charge you a percentage (usually 3–6%) of each investment they make on your behalf.

Some advisors charge hourly rates that can average anywhere from $200–400, depending on their location and specialties.

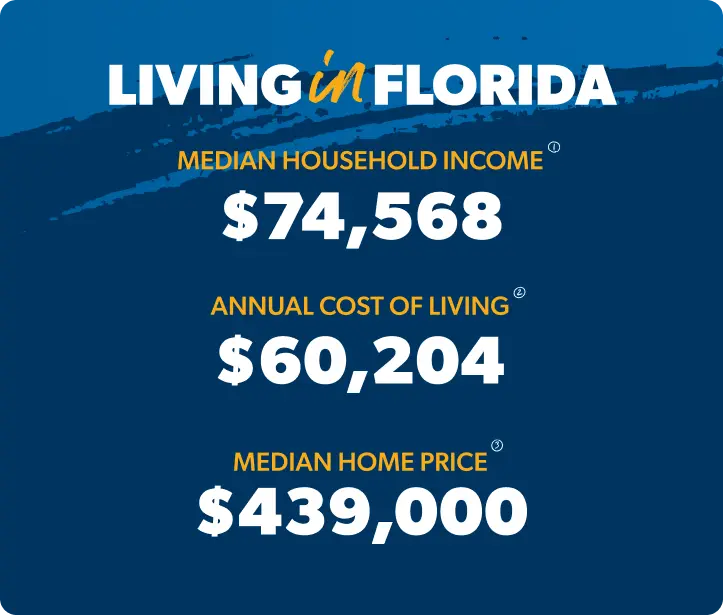

Get a breakdown of average prices for everything from housing and utilities to health care in various cities across Florida.

Whether you’d like an ocean view or just an affordable place to retire in Florida, we’ll point you in the right direction.

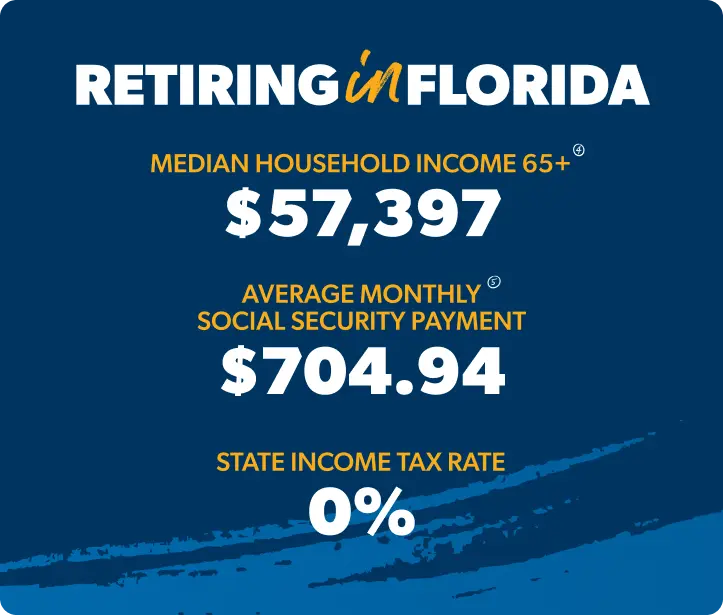

One of the advantages of retiring in Florida is that there’s no income tax! Learn more about taxes in the Sunshine State.

Financial advisors in Florida charge a variety of rates and even use different types of pricing structures. Here’s a breakdown of some of the most common ways financial advisors charge for their services—and a rough estimate of how much you could expect to pay under each:

Assets-under-management (AUM) pricing: Advisors who use an AUM pricing model charge you a percentage (usually around 1%) of the value of the assets they manage for you. For example, an advisor who charged an annual 1% AUM fee would get paid $1,000 a year for every $100,000 worth of assets they managed for you

Flat-Fee Pricing: This type of advisor pricing model is more like a subscription. As a client, you agreed to pay a fixed price that doesn’t change with the size of your portfolio. Depending on the services you need, these prices usually cost anywhere from several hundred to several thousand dollars a year.

Commission-based pricing: Commission-based advisors don’t typically charge for their advice but earn money from fees that are built into products they sell you. For example, if you gave an advisor $10,000 to invest in a mutual fund and their commission fee is 5%, they’d take a $500 fee and invest the remaining $9,500 into the fund for you.

Hourly pricing: Financial advisors who charge by the hour tend to only provide advice instead of ongoing financial management. Their fees are usually determined based on the services you need and their specialties.

Most wealth managers use an Assets Under Management (AUM) pricing model. That means that they charge you a percentage (usually around 1%) of the assets they manage for you.

Is there a difference between a financial planner and a retirement planner?

While there is a difference between a financial planner and a retirement planner, it is possible for a financial professional to be both.

Many financial planners do offer retirement planning services, but can also help with things like taxes, wealth management, insurance, budgeting and investment management. They usually hold certifications like Certified Financial Planner (CFP®).

Retirement planners hold certifications like Retirement Income Specialist (RICP®). They specialize in helping clients create a retirement financial plan that includes everything from withdrawals to Social Security and Medicare.

While everyone’s situation is different, there can be plenty of advantages to working with a financial advisor during retirement. When you’re nearing or in retirement, a financial advisor can help with things like:

Red flags for financial advisors include things like guaranteeing returns, pressuring you to invest in things you don’t understand, and lack of clarity about their qualifications or how they get paid.

A good financial advisor:

Keep in mind that a financial advisor works for you, not the other way around. A good financial advisor should leave you feeling empowered, not intimidated.

The average cost of living for Florida retirees can vary based on lifestyle choices, whether you own your home, and even the area you choose to live. But all things considered, the median cost of living in Florida is around $60,000.

In addition to the year-round sun, retiring in Florida comes with several nice financial perks. The sunshine state is considered one of the tax-friendliest places for seniors in U.S.

Florida is one of the few U.S. states with no state income tax—which means retirees get to keep more of their income from retirement accounts, Social Security and pensions.

Florida doesn’t do estate or inheritance taxes either. It also offers several sweet property tax exemptions for residents over 65.

The content on this page provides general guidelines about investing topics. Your situation may be unique.

To discuss a plan for your situation, connect with an investment professional.

SmartVestor™ is an advertising and referral service for investment professionals operated by The Lampo Group, LLC d/b/a Ramsey Solutions (“Ramsey Solutions”). When you provide your contact information through the SmartVestor site, Ramsey Solutions will introduce you to up to five (5) investment professionals (“Pros”) that cover your geographic area. Each Pro has entered into an agreement with Ramsey Solutions under which the Pro pays Ramsey Solutions a combination of fees, including a flat monthly membership fee and a flat monthly territory fee to advertise the Pro’s services through SmartVestor and to receive client referrals from interested consumers who are located in the Pro’s geographic area. Each Pro may also, if applicable, pay Ramsey Solutions a one-time training fee.

The fees paid by the Pros to Ramsey Solutions are paid irrespective of whether you become a client of a Pro and are not passed along to you. However, you should understand that all of the Pros that are available through SmartVestor pay Ramsey Solutions fees to participate in the program. Further, the amount of compensation each Pro pays to Ramsey Solutions will vary based on certain factors, including whether the Pros choose to advertise in local or national markets. Ramsey Solutions has a financial incentive to present certain Pros that offer their services on a national basis (“National Pros”) more often than other National Pros that pay lower fees.

It is up to you to interview each Pro and decide whether you want to hire them. If you decide to hire a Pro, you will enter into an agreement directly with that Pro to provide you with investment services. Ramsey Solutions is not affiliated with the Pros and neither Ramsey Solutions nor any of its representatives are authorized to provide investment advice on behalf of a Pro or to act for or bind a Pro. Ramsey Solutions introduces you to Pros that cover your geographic area based on your zip code. Neither Ramsey Solutions nor its affiliates provide investment advice or recommendations as to the selection or retention of any Pro, nor does Ramsey Solutions evaluate whether any particular Pro is appropriate for you based on your investment objectives, financial situation, investment needs or other individual circumstances.

No investment advisory agreement with a Pro will become effective until accepted by that Pro. Ramsey Solutions does not warrant any services of any SmartVestor Pro and makes no claim or promise of any result or success by retaining a Pro. Your use of SmartVestor, including the decision to retain the services of a Pro, is at your sole discretion and risk. Any services rendered by a Pro are solely that of the Pro. The contact links provided connect to third-party websites. Ramsey Solutions and its affiliates are not responsible for the accuracy or reliability of any information contained on third-party websites. Each Pro has signed a Code of Conduct under which they have agreed to certain general investment principles, such as eliminating debt and investing for the longer-term, and, if applicable, have completed Ramsey Pro Training. However, Ramsey Solutions does not monitor or control the investment services the Pros provide.

The term financial advisor covers a wide range of specialties. The good news? The credentials after an advisor’s name offer clear clues about the services they provide.

Here’s a quick guide to some of the most common credentials and what they mean.

CFAs have extensive training in investment analysis. They usually work with large institutions, but some do take on individual (usually high-net-worth) clients.

What they can help with:

CFPs have to pass a thorough exam, complete thousands of hours of work experience, and operate under a code of ethics.

What they can help with:

CPAs have to pass a tough exam to earn their title and tend to be experts in things like taxes and business finance.

They can help with:

IARs work under RIAs and will often be the ones you work with directly.

They can help with:

A PFS is a CPA who has taken it to the next level. They’ve fine-tuned their skills with even more education—and proven it by passing more exams.

They can help with:

RIAs are financial advisors or firms that are registered with the Securities and Exchange Commission (SEC) and held to a fiduciary standard. That means they’re legally bound to act in your best interest.

They can help with:

*RIAs usually operate on a fee-only or fee-based pricing structure. This helps avoid commission-driven sales that could conflict with their fiduciary standard.

Registered representatives work for (or are affiliated with) a broker-dealer firm. They often work on commission and are licensed to buy and sell investment products on your behalf.

What they can help with: