Should You Buy Stocks? Here’s What You Need to Know

10 MIN READ | JUL 17, 2024

By

By

Key Takeaways

- Stocks are a type of investment that give investors tiny pieces of ownership in a company.

- While investing in stocks always has some element of risk, there are ways you can reduce your risk—and that’s through diversification.

- Mutual funds, which contain stocks from dozens or hundreds of different companies, are the best type of long-term investment.

Did you ever hear the story about the tortoise and the hare when you were a kid? Believe it or not, there's something to learn about investing from this little tale.

Stocks are a powerful wealth-building tool, but they can also delay your progress and cost you a lot of money and heartache without the proper caution. There’s a fast and reckless way to invest in stocks (the hare), and then there’s the slow and steady way (the tortoise).

Let’s take a closer look at stocks and talk about everything you need to know about investing in them the smart way, starting with the basics.

How Do Stocks Work?

When you buy stock in a company, you become a partial owner of that business. But before you shoot off an email requesting a corner office or reserving the company jet, just know that companies often issue millions—if not billions—of shares of stock.

Each day, millions of shares of stock are bought and sold through the stock market. And all that buying and selling causes prices to rise and fall. If lots of investors are buying a certain stock, that’ll cause the price to rise. But if more investors are trying to sell instead of lining up to buy, then the price of that stock will drop.

So, what makes investors want to buy one stock instead of another? Demand for a stock is driven by things like a company’s earnings and profitability. But there are hundreds of other reasons why people do or don’t invest in companies, and that all affects price. If the U.S. economy is going through a downturn, stock prices could fall across the board.

Stock prices often go up and down based on guesses about how companies are performing or how they’ll perform in the future. Maybe they’re in an up-and-coming industry or in an industry that seems to be on the decline.

In other words, stock prices are unpredictable, and that’s why investing in single stocks is risky.

How Do You Make Money From Owning Stock?

With stocks, you make money one of two ways (and sometimes both ways):

Dividends

Dividends are quarterly payments of company profits distributed to stockholders. They’re basically the company’s way of saying thank you for investing in the company.

Keep in mind that not all stocks pay dividends. Some companies decide to reinvest their profits in their company rather than paying dividends.

The companies that do pay out dividends normally do so in cash. But there are other types of dividends you could receive, including stock dividends and opportunities to do some dividend investing.

Capital Appreciation

When your shares of stock increase in price, it’s called capital appreciation. But that potential profit only exists on paper and could disappear unless you sell your stock for more than you paid for it.

And that’s why you want to take a long-term approach to investing. The market will go up and down over the years, but if you give compound interest time to work its magic, your money will continue to grow, no matter how volatile the market is. It won’t make you rich overnight, but it’ll pay off in the end!

Should You Invest in Stocks?

Yes, stocks should definitely be part of your retirement portfolio . . . but you need to be smart about how your stocks are grouped and diversified.

Historically, the stock market’s average annual return is somewhere from 10–12%.1 That means that if you invest in stocks the right way, you can grow your retirement savings so they beat inflation and set you up for the kind of retirement you’ve always wanted.

But if you’re not careful, you could be betting your retirement future on the success of single stocks . . . and that usually doesn’t end well.

That’s why we recommend you invest in growth stock mutual funds. Chances are, your company’s 401(k) plan is full of them! This is the best place to start investing since it’s an easy and automatic process. In addition to your workplace account, you can open a Roth IRA to take advantage of tax-free growth.

Hear us on this: Investing is important! To keep up with inflation, your money needs to work for you—to grow over time. Stuffing it under a mattress or burying it in your backyard like a pirate will not help you when it comes time to retire.

Getting started on your investing journey might seem overwhelming, but you don’t have to walk this path alone. An investment professional can help you get started and make a game plan for your money.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

What’s the Best Way to Buy Stocks?

While investing in stocks always has some element of risk involved, there are ways you can reduce your risk—and that’s through diversification. That’s just a fancy investing term for spreading your investments around so that you’re not putting all of your eggs in one basket.

There are basically three different ways you can buy stocks:

- Single stocks

- Exchange-traded funds (ETFs) and index funds

- Mutual funds

Which option will help you save for retirement the most? Let’s go through them one at a time.

Single Stocks

When you buy a single stock, you’re basically betting on the performance of one company. Most people who dabble with buying and selling stocks try to “time the market.” They’ll buy a stock when its value is low and then plan to sell after its value rises to make a profit.

Instead of taking a “buy and hold” approach to investing—which means you hold on to your stocks for longer periods of time regardless of what the stock market is doing—most stock traders will try to sell their stocks after just a few days or weeks to make a quick profit.

The bottom line: Let’s be really clear here—we do not recommend investing in single stocks! There’s just too much risk in tying your investments to the performance of just a handful of companies. If you put your retirement savings into one stock, what happens if that company goes under? Boom! Your investments are gone.

Your grandmother was really onto something when she said don’t put all your eggs in one basket. It’s better to diversify your money so you can reduce risk and take a more balanced approach to building wealth.

Exchange-Traded Funds (ETFs) and Index Funds

Exchange-traded funds (ETFs) are very similar to mutual funds, filled with stocks from many different companies . . . except they’re bought and sold like single stocks.

Most ETFs are also like index funds—they’re filled with stocks from high-performing companies known for being reliable investments, like Amazon, Microsoft, Apple and The Home Depot. They’re often referred to as blue-chip companies, because in the game of poker, the blue chip has the highest value.

While ETFs usually carry lower fees than many mutual funds, you lose the personal touch that comes from working with a professional. Believe us, it helps to have an investment professional in your corner to help you pick and choose your investments.

The bottom line: Only after you’ve maxed out your retirement accounts should you even think about investing in low-turnover ETFs (or index funds) inside of a taxable investment account.

Let’s say you’ve maxed out your 401(k)s and IRAs and still want to keep investing. In that situation, you could open up a taxable investment account—like a brokerage account—and invest in stock ETFs or index funds that mirror the stock market (which means they average 10–12% annual growth over the long-term).

Mutual Funds

Mutual funds are created when a group of investors pools its money together and buys stocks from dozens or hundreds of different companies, which gives you a healthy level of diversification for your investments.

Most mutual funds are also actively managed funds, which means a team of investing professionals makes it their mission to pick and choose stocks for the fund with the goal of beating the stock market’s average returns.

The bottom line: We have a winner! Mutual funds are the best type of long-term investment. Investing for retirement through mutual funds does two things:

- It diversifies your portfolio, protecting you from the huge losses that can come from investing in just a few single stocks. You’ll still experience the ups and downs of the stock market, but over time the value of your mutual funds should continue to grow.

- It helps you reap the benefits of investing in stocks of companies of all sizes from different industries and sectors of the economy.

And on top of all that, you get the benefit of having an investment pro in your corner to help you adjust your investments throughout your financial journey.

The Smart Way to Invest in Stocks

One of the biggest myths about millionaires is that they take big risks with their money on things like get-rich-quick gimmicks and fad investments like the latest single-stock investment hype.

But when we talked to over 10,000 millionaires for The National Study of Millionaires, do you know how many of them said that single stocks were one of their top-three wealth-contributing factors? Zero. Not a single one!

Instead, 8 out of 10 millionaires reached a million-dollar net worth through steadily investing through their employer-sponsored retirement plan, like a 401(k). They got there over time, after years of hard work and consistently investing into their retirement accounts. That’s how you become a Baby Steps Millionaire!

Once you’re out of debt and have a fully funded emergency fund, invest 15% of your gross income in growth stock mutual funds inside your tax-advantaged retirement accounts, like a 401(k) and Roth IRA.

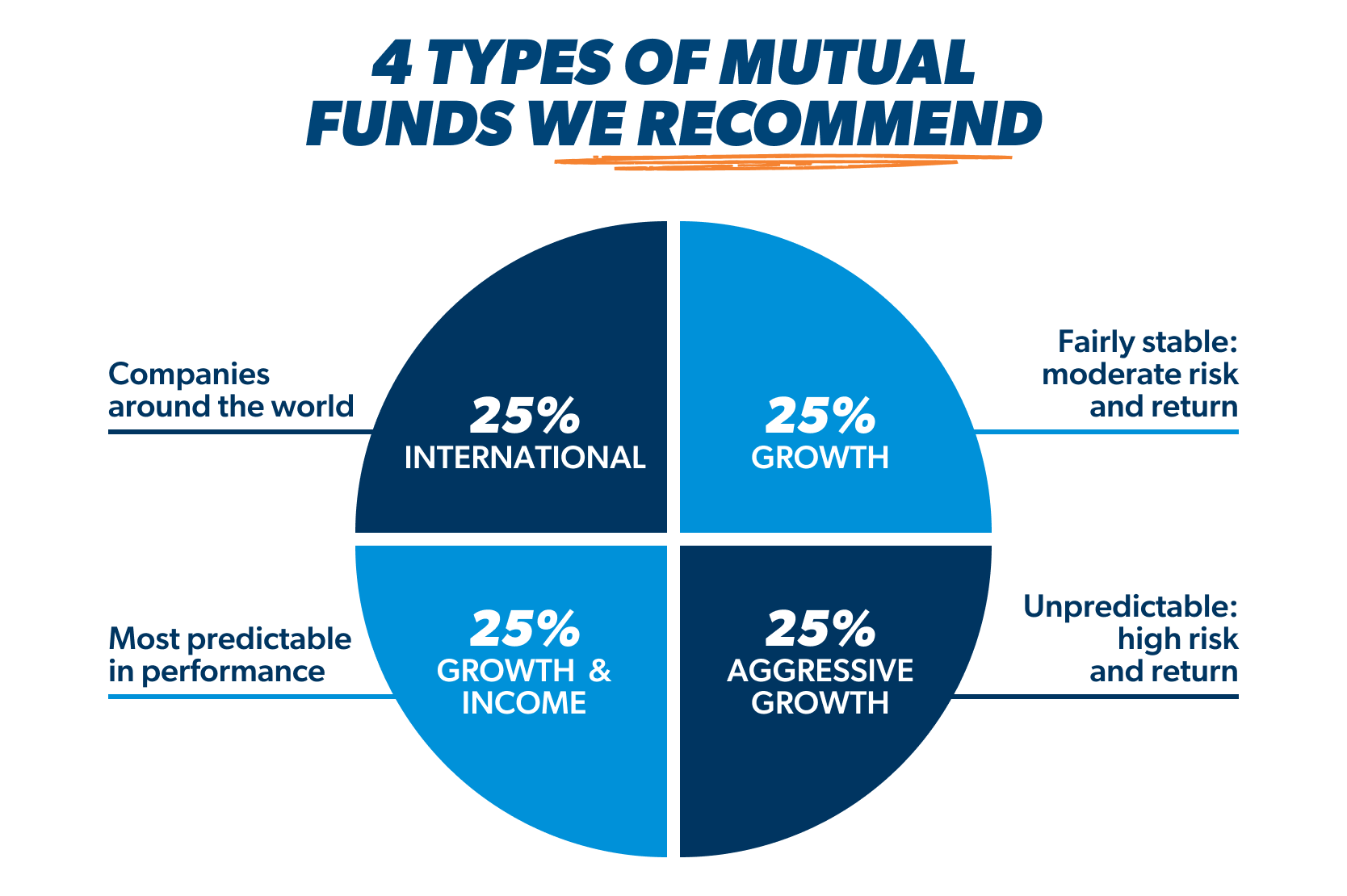

We also recommend diversifying your portfolio even more by dividing your investments evenly across four different types of mutual funds:

- Growth and income (large cap): The calmest and most predictable funds in your portfolio, these funds contain stocks from large, stable companies you’d probably recognize.

- Growth (mid cap): These funds are invested in medium to large companies that are still growing and usually bring in higher returns than growth and income funds.

- Aggressive growth (small cap): The wild child of your portfolio, aggressive growth funds have stocks from smaller companies with lots of potential, but they are all over the place—one year they could be way up and the next they could be way down.

- International: These funds contain stocks from companies all over the world and will help you diversify your portfolio beyond your country’s borders.

When you spread out 25% of your investment money to each of these four funds, you’ll ensure that your portfolio is diversified.

And listen, if you’re already investing 15% for retirement or reached millionaire status and you want to put a very small percentage of your net worth into single stocks, we’re not going to yell at you. But when you’re just getting started with investing, there’s just too much at stake to put it all on the line for a single stock.

Connect With an Investment Professional

There are two things we always tell people when it comes to investing. First, you should never invest in anything you don’t understand. And second, you don’t have to figure it all out on your own.

That’s where an investment professional comes in. Our SmartVestor program can connect you with up to five investment pros in your area. They’ll sit down with you and help you understand your investing options so you can make confident decisions that’ll help you save for the retirement you’ve always wanted. You can do this!

Next Steps

- Your 401(k) is a great place to get started investing in growth stock mutual funds, especially if there’s a company match! Set a meeting with your company’s HR representative to discuss your company’s retirement plan options.

- Want to learn more about the stock market? Check out our article on the stock market and how it works.

- If you’re ready to start investing, our SmartVestor program can connect you with up to five investment pros in your area.

Frequently Asked Questions

-

What is the stock market?

-

If stocks are shares of companies, and markets are places where things are bought and sold, then the stock market is where brokers buy, sell and trade stocks! Pretty simple, right?

Stockbrokers are people who buy and sell stocks, usually on behalf of clients they represent or funds they manage. They’re always watching stock market activity and tracking real-time updates to see how the stocks are performing.

The stock market isn’t necessarily a physical location, although the New York Stock Exchange (NYSE) is housed in an actual building on Wall Street. The Nasdaq is an electronic exchange where brokers communicate through computers to buy and sell.

If you pay any attention to financial news, you’ll hear a lot about the Dow. It’s short for the Dow Jones Industrial Average, which is a list of 30 large public companies that are traded on the NYSE and the Nasdaq. It’s basically a quick reference of how top companies are performing.

-

What is stock trading?

-

Stock trading is the act of buying and selling stocks frequently with a goal of making short-term profits instead of focusing on long-term gains.

With stock trading, the goal is to “time the market.” That’s investing talk for buying stocks when they’re low and then selling them when they’re high to make a profit. We never recommend stock trading for a few important reasons:

- When you mess with single stocks, you’re not investing—you’re “chasing.” Here’s what happens: You buy a company’s stock when it’s low. You start to see it grow and grow and you get really excited. Each day or each month you have an idea or a goal of when to sell, but here’s the problem—you don’t know where the ceiling or the floor is. The stock starts to fall, but you stay in, hoping it bounces back, or you double down to chase what you lost. You keep chasing, hoping, wishing . . . and then it’s gone.

- Stock traders have a short-term perspective, but as an investor, we want you to focus on growth over the long haul instead of trying to make a quick buck right now. Investing and saving for retirement is a marathon, and slow and steady wins the race every time!

- For long-term investing, you want your nest egg to be diversified. That’s why we recommend investing in good growth stock mutual funds that are stuffed with stocks from dozens of different companies. That way, you get to enjoy the long-term growth of stocks without relying solely on the success of one or two companies.

-

How do dividends affect stock prices?

-

Have you ever seen the chaos that ensues at the running of the bulls in Spain? Well, it looks a lot like that once news of a dividend payment becomes public. You’ll see a rush to purchase the stock before the ex-date (the deadline to buy stock and receive the dividend).

When that happens, you’ll see the share price go up. You’ll also notice the price dropping after the ex-date because anyone buying the stock on or after that date won’t receive the dividend, so people sell the stock.

-

What are the differences between stocks and bonds?

-

A stock is an investment that represents a tiny piece of ownership in a company. But a bond is a type of loan between an investor and a corporate or government borrower that promises to repay the money with interest.

Companies and governments at all levels (state, local, federal) issue bonds to borrow money for projects too expensive for a bank to fund. By issuing bonds, they’re basically handing out IOUs where they agree to pay you interest on the loan and return your principal (the original amount you loaned to them) at a specific date in the future.

That’s right, you’re loaning them your money! Unlike buying stock, where you are buying partial ownership of a company, bonds do not have ownership attached to them. You’re simply a lender. Though most bonds have a fixed interest rate, bonds with variable rates are gaining in popularity.

What a lot of people find attractive about investing in bonds is the possibility of receiving steady payments over the life of the bond. Having that stable income makes it easy to plan out your spending, which is why bonds are tempting additions to many retirement portfolios.

But we don’t recommend betting your retirement on bonds. The returns you get from bonds just aren’t impressive, especially when compared to mutual funds, because they barely outpace inflation. That’s why you’re better off investing your money in a mix of growth stock mutual funds. Remember, you want to beat the market so you can build wealth.

This article provides general guidelines about investing topics. Your situation may be unique. To discuss a plan for your situation, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.