Pay-Yourself-First Budget: What It Is, How It Works, and How It Compares to Zero-Based Budgeting

By

By

Key Takeaways

- Pay-yourself-first budgeting automatically sets aside money for savings as soon as a paycheck arrives, before any other spending.

- This approach is a strong savings habit, but it’s not a complete plan without a zero-based budget telling every dollar where to go.

- If you’re in debt, those dollars need to go toward the debt snowball first, not into savings.

- A zero-based budget gives you control by assigning every dollar a job before the month begins.

- When you’re debt-free, combining a zero-based budget with automatic saving is a powerful way to build wealth.

Your paycheck lands, and somewhere between payday and the end of the month, it disappears. A quick scan through your account shows nothing out of the ordinary. Groceries. Gas. That random fix the car needed. By the time you think about saving, there’s nothing left to save.

That’s the problem pay-yourself-first budgeting is meant to fix. With this method, you save or invest a set amount the moment your paycheck hits (before bills, spending or anything else).

But this method isn’t a full plan. To really win with money, you need to see how it fits inside a zero-based budget.

Here's a Tip

A pay-yourself-first budget is a savings strategy where you move a set amount to savings the moment your paycheck hits—before bills, spending or anything else. It’s simple and automatic, but it’s not a complete plan on its own. To really win with money, it needs to work inside a zero-based budget.

What Is Pay-Yourself-First Budgeting?

A pay-yourself-first budget treats savings like a bill you pay first. As soon as you get paid, an automatic transfer moves a set amount—let’s say 15%—straight into your savings or investments. You might also hear this called “reverse budgeting” (because you save first, then live on the rest).

It feels like a win because you save right away, giving you confidence you’re making real progress toward your savings goals.

But here’s the catch: Paying yourself first only works if you don’t have debt. If you do, you’re just saving money on one side while your debt keeps growing on the other. And if you’re already living paycheck to paycheck, pulling money out first can leave you short when it’s time to pay your bills.

That’s why paying yourself first is just one piece of the puzzle. The real plan is zero-based budgeting, where every dollar has a job before the month begins. In other words, you’re telling your money where to go instead of wondering where it went.

What Are the Benefits of Paying Yourself First?

People like the pay-yourself-first method because it’s simple and makes it easier to follow through on saving. Here’s why they stick with it:

- It automates saving. Money moves to savings on payday, so you don’t have to think about it.

- It makes saving happen first. Instead of hoping there’s something left at the end of the month, you set money aside from the start.

- It builds consistency. Saving the same amount each month helps turn good intentions into a habit.

- It creates a sense of security. Watching your savings grow can make you feel more stable and in control of your money.

That’s what makes it appealing. Now let’s see how it actually works.

How Does the Pay-Yourself-First Method Work?

Here’s what the pay-yourself-first method looks like in real life. Let’s say you bring home $3,000 per paycheck:

Step 1. Your paycheck hits. $3,000 lands in your account.

Step 2. Savings goes out first. You’ve set up a 10% automatic transfer, so $300 moves to savings the same day.

Step 3. You pay your bills. You cover your rent, utilities, car payment, insurance and other bills with what’s left. Let’s say those bills total $2,400.

Step 4. You spend what’s left. The remaining $300 goes toward groceries, gas, eating out, subscriptions and whatever else comes up.

|

Step |

What Happens |

Example: $3,000 Take-Home Pay |

|

Your paycheck arrives. |

The full paycheck hits your account. |

$3,000 |

|

Savings goes out first. |

A fixed percentage transfers to savings immediately—before you spend anything. |

-$300 |

|

You pay your bills. |

You pay your rent, utilities, insurance and other fixed expenses. |

-$2,400 |

|

You spend what’s left. |

You spend the remaining money without a clear plan. |

-$300 |

But look at that last line. That $300 has to stretch across the rest of the month.

Groceries run higher than expected. Gas prices jump. You’re out of laundry detergent and need to restock basics. By the third week, the money’s gone, and now you either have to dip into savings or reach for a credit card.

That’s the problem with traditional pay-yourself-first budgeting. It handles savings, but it doesn’t make sure the rest of your money actually works. A zero-based budget fixes that.

Pay Yourself First vs. Zero-Based Budgeting: Which Should You Pick?

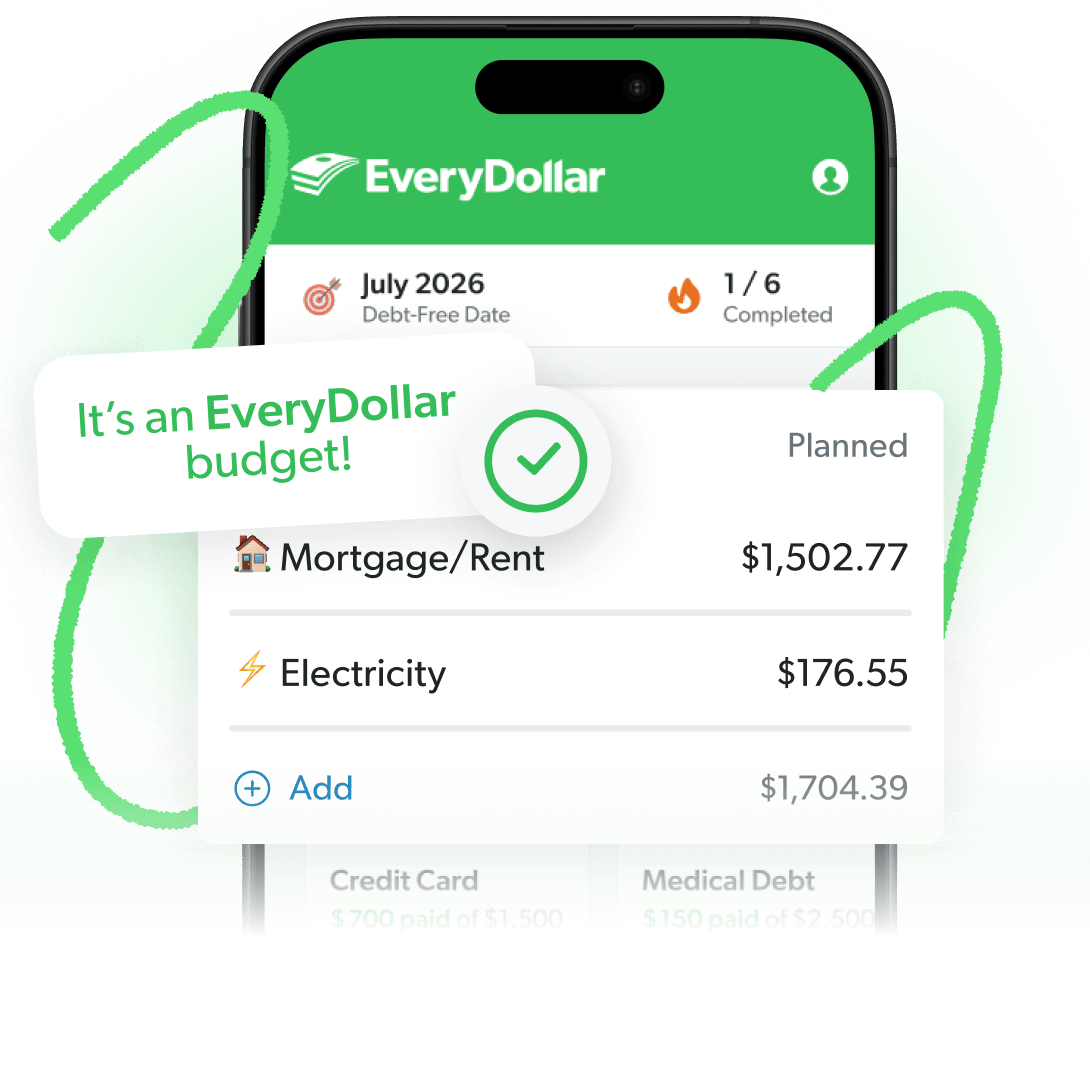

We’re huge fans of zero-based budgeting because it works for everyone, at every Baby Step. That’s why we created the EveryDollar budget app. It’s zero-based by design, which makes it easy for you to give every dollar of your income a job to do before the month begins.

Paying yourself first fits inside that plan. Once you’re out of debt, saving simply becomes one of the first jobs your budget handles.

So the question isn’t which method to pick. Both serve a purpose, and they can work together.

Pay Yourself First vs. Zero-Based Budgeting

|

Criteria |

Pay Yourself First |

Zero-Based Budgeting |

|

What it is |

A savings habit with one automatic transfer |

A complete plan where every dollar has a job |

|

Who it’s for |

People who are debt-free and using a zero-based budget |

Everyone, no matter what Baby Step you’re on |

|

Spending visibility |

Savings is covered, but the rest goes unplanned without a budget. |

You have full visibility because every category is planned before the month begins. |

|

Works on its own? |

No. Savings is handled, but spending is not. |

Yes. It covers your entire plan from start to finish. |

|

The Ramsey approach |

Use this after you’re out of debt. |

Every budget should be zero-based. |

How to Create a Zero-Based Budget That Puts Savings First

At this point, you may be wondering how to use a pay-yourself-first method with a zero-based budget. Well, the suspense is over. Here's how to build a zero-based budget with automated savings. Every dollar gets a job—and once you’re out of debt, savings is one of the first jobs you assign (right after giving). The difference is, now it’s part of a plan where every dollar is accounted for, not just one line item.

|

|

Pay-Yourself-First Budgeting |

Zero-Based Budgeting |

|

Step 1 |

Decide a savings percentage and automate the transfer. |

Give first. Set aside 10% for your church or charity. |

|

Step 2 |

Pay your fixed bills. |

Cover the Four Walls: food, utilities, shelter, transportation—in that order. |

|

Step 3 |

Spend whatever’s left (without tracking anything). |

If you choose to, automate your savings transfer (Baby Steps 3–7). |

|

Step 4 |

— |

Assign every remaining dollar to a spending category. |

|

Step 5 |

— |

Track your spending throughout the month. |

|

Step 6 |

— |

Adjust your budget when life happens. |

|

Step 7 |

— |

Make a new zero-based budget before the next month begins. |

The Steps (in Detail)

Let’s take a closer look at how each step works.

Step 1. Give first. The first line of your budget is giving. Set aside 10% for your church or charity. If your church offers automatic giving, set it up on payday just like your savings. Giving shapes how you think about money and keeps your focus on something bigger than yourself.

Step 2. Cover the Four Walls. Start with food, utilities, shelter and transportation—in that order. These are your most important expenses each month, and they come before anything else.

Step 3. Set your savings and automate it. This is where the pay-yourself-first habit comes in. If you’re debt-free and in Baby Step 3, start putting money toward fully funding your emergency fund. If you’re on Baby Step 4 and beyond, invest 15% of your gross income for retirement—typically through payroll deductions like a 401(k). Set up any additional transfers for the same day your paycheck hits so the money moves before you have a chance to spend it.

Here's a Tip

If you’re still in Baby Step 2, skip saving and investing for now and put that money toward the debt snowball. You’ll come back to saving once you’re out of debt.

Step 4. Assign every remaining dollar to a category. That includes insurance, childcare, groceries, gas, eating out and everything else. When you’re done, your income minus your planned expenses should equal zero. That’s what zero-based budgeting means. You’re making sure there are no dollars left without a purpose.

Kimberly from our Ramsey Baby Steps Community Facebook group explained it this way: “A zero-based budget isn’t referring to your bank account at all—it’s referring to what you do with your money. When you have a paycheck come in, list all your expenses. When you subtract them from the total of that paycheck, it should equal zero. Repeat this monthly!”

Step 5. Track your spending throughout the month. A budget only works if you actually use it. Check in throughout the month, not just at the end. Weekly is a good baseline, but more often is even better. When you see a category getting low, you can adjust before you run out of money. And if you're in Baby Step 3 and you see you budgeted more than you need in a category, throw that extra at your emergency fund.

Step 6. Adjust as life happens. Something unexpected will come up, and that’s normal. Move money from one category to another and keep going. You didn’t fail. Your budget is just doing its job.

Step 7. Make a new budget before the month begins. Don’t reuse last month’s numbers. Sit down before the new month starts and build a fresh zero-based budget based on what’s coming up. Every month is different, and your budget should reflect that.

Find Margin You Didn’t Know You Had With EveryDollar

The EveryDollar budgeting app helps you find extra money every month so you can beat debt, build wealth, and make progress. Every. Day.

Pay-Yourself-First Budgeting Examples

Now let’s walk through a couple examples that show why a zero-based budget is really what makes paying yourself first work. Notice what’s different in each scenario.

Example 1: It works—because it’s part of a plan.

Jenna is 27, debt-free, and takes home $4,000 a month. Before the month begins, she builds a zero-based budget. She gives first (10%, which is $400), then covers her essential expenses.

Because she’s in Baby Step 3, she’s focused on building her fully funded emergency fund. She automates $600 a month toward savings. Then she assigns every remaining dollar a job and tracks her spending throughout the month. If she ends up with money left over in a category, she puts it toward her savings too.

After eight months, she has at least $4,800 saved (and likely more). Nothing about her income changed—she just had a plan. Saving worked because every dollar had a purpose.

Example 2: It breaks down—because there’s no plan.

Marcus is 34, debt-free, and also takes home $4,000 a month. He decides to try a pay-yourself-first budget by setting up a $600 automatic transfer to savings each month.

But he never builds a full budget. After his bills and fixed expenses, he spends what’s left without a plan. Some months feel fine, but others don’t. Groceries run high, unexpected costs pop up, and by the third week, his money is gone. He ends up dipping into savings just to cover the gap.

His savings might grow some months, but it doesn’t stick. If Marcus used a zero-based budget, he would see exactly where his money is going and make sure every dollar, including that $600, is working on purpose.

Common Mistakes—and How to Fix Them

Even with good intentions, the pay-yourself-first method can go sideways if you’re not careful. Here are some common mistakes and how to fix them:

- Setting up automatic savings without a plan for the rest of your money. The fix: Saving is only one part of the picture. You need a plan for everything else too. Give every dollar a job so you know exactly where your money is going.

- Saving while carrying debt. The fix: If you have debt, those dollars have a different job. Once you’ve built your starter emergency fund (Baby Step 1), put everything you can toward the debt snowball (Baby Step 2). You’ll come back to saving once you’re out of debt.

- Setting your savings amount too high and pulling money back out. The fix: Start with an amount you can actually stick to. Consistency matters more than hitting a perfect number. You can always increase it over time.

- Not tracking spending during the month. The fix: A plan only works if you follow it. Check your budget regularly so you can adjust before you run out of money, not after.

Take Control of Your Money

When every dollar has a job, you take control of your money and finally pay off debt, save money, and build wealth for the future. Dave Ramsey says it this way: Live like no one else now so later you can live and give like no one else.

The EveryDollar budgeting app helps you put that plan into action. It’s free to start and built on the same money principles Dave has taught for decades, so you can build your budget, track your spending, and stay on top of your money all month long.

Next Steps

- Figure out your monthly take-home pay so you know exactly what you’re working with.

- If you’re debt-free, automate your savings. If not, send that money straight to the debt snowball until you are.

- Build a zero-based budget that starts with giving, covers your Four Walls, and assigns every dollar a job.

Frequently Asked Questions

-

Is the pay-yourself-first method a good budget method?

-

Paying yourself first is a helpful saving habit, but it’s not a complete plan. The best plan is zero-based budgeting, where every dollar has a job. If you’re debt-free, saving can be one of the first jobs you assign. If you’re in debt, those dollars go to the debt snowball.

-

How much should I pay myself first?

-

Once you’re in Baby Step 4, invest 15% of your gross income for retirement. If you're in Baby Step 3 and want to automate your emergency fund savings, set yourself up to save as much as you can for your emergency fund each month. If you still have debt, you should focus all your money toward paying that off. You can come back to savings once you've kicked debt to the curb.

-

Can I use the pay-yourself-first method while paying off debt?

-

No—you’ll make faster progress by focusing on one goal at a time. First, save up $1,000 for your starter emergency fund. Then put all your extra money toward paying off debt with the debt snowball. Once you’re debt-free, you can try paying yourself first to save up your full emergency fund.

-

Pay yourself first vs. zero-based budgeting: Which pays off debt faster?

-

Zero-based budgeting. It gives every dollar a job and helps you find more money to throw at your debt. Paying yourself first comes later, once you’re out of debt.

-

What’s the difference between paying yourself first and a reverse budget?

-

There’s no difference. They’re two names for the same idea: Save first, then spend what’s left.

-

What app or tool should I use for a pay-yourself-first budget?

-

We recommend EveryDollar. It’s built on zero-based budgeting, so you can plan your saving and spending, track your money, and stay on top of your budget all month long. It’s free to start.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.