By

By

Key Takeaways

- No matter what it’s for or what form in comes in, debt means you owe money and keeps you from building wealth for you and your family—and that’s never good.

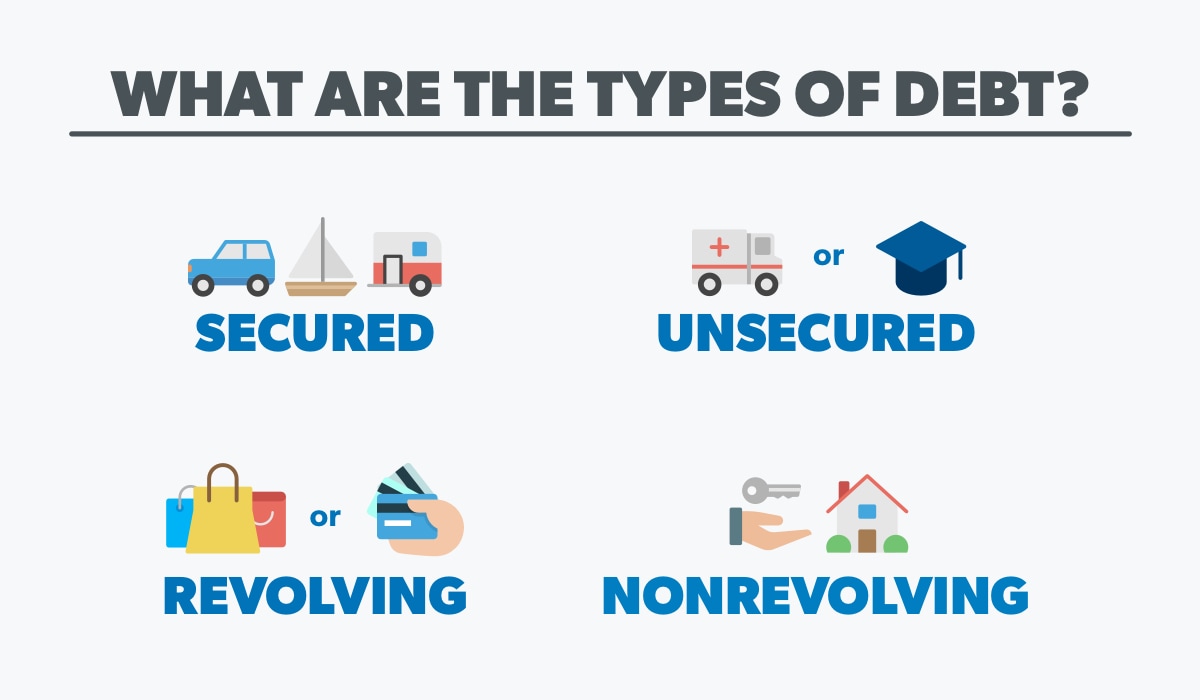

- The main types of debt are secured debt, unsecured debt, revolving debt, nonrevolving debt and sneaky debt.

- Commit to kicking debt to the curb for good by making a budget every month and working the debt snowball.

Car loans, student loans and credit cards. Oh my!

Debt comes in many shapes and sizes. But no matter what form it takes, debt just steals from you and your future. It’s time to take back control of your money! Here’s everything you need to know about the different types of debt—plus how to break up with debt for good so you can start living the life you want.

What Is Debt?

Debt is when you owe anyone money. Any time you don’t pay in full—that’s debt. Are you still making payments for something you bought? Yep, also debt. You purchased the Cadillac before you had the cash. You borrowed from your mother-in-law because you didn’t have the moola. No matter how you package it, debt means you’re at the mercy of someone else until you pay them back.

Maybe debt is a common word in your house, or maybe you think you’ve done a good job avoiding it. But no matter what kind of relationship you have with debt, Proverbs 22:7 says the borrower is slave to the lender.

When you have debt, you’re no longer working just for you or your family—you’re working for the people you owe money to. And the average American carries $34,055 in consumer debt.1 That’s not okay! You’re made for more in this life than just working to pay off debt.

Listen, debt is debt. And it’s holding you back no matter what type it is! But let’s walk through the types of debt that are out there so you can know how to avoid the traps. Keep in mind, some debts fit into more than one category.

Secured Debt

The dealer hands you the keys to a brand-new SUV. You pump your fist in the air and drive home to show off the car you just bought. Except you didn’t buy it—you financed it. The bank owns the car. You just get to pay them to drive it each month. That’s secured debt.

With secured debt, any money you borrow is backed by a physical item. In other words, there’s collateral. When you finance a car, boat, RV or even a home, the lender looks at your credit to check your borrowing history. That helps them determine your interest rate (money charged just for the act of borrowing).

They also place a claim of ownership (also called a lien) on your stuff. If you stop making payments, the lender can take the item back (either through repossession or a foreclosure).

Secured debt is great for lenders because it means less risk for them. They either get their money, or they get the item back to sell. But it also means more risk for you. The moment you don’t pay up, you’ll be saying hello to the repo man and goodbye to your precious Honda. And with assets that go down in value (like cars), you could end up underwater and owe more than the item is worth.

But instead of paying someone else to use their stuff (because that SUV isn’t yours until you finish paying it off), what if you saved up cash to buy that item up front? Not only will that save you a ton of money in interest, but you’ll also get a better night’s sleep knowing your car (and your mattress) is paid for.

Unsecured Debt

So, if secured debt is backed by something that can be taken away, what about unsecured debt? Unsecured debt means there’s no collateral for the loan. Think credit cards, student loans, medical bills, payday loans, personal loans, or a bunch of other money traps. It’s money you’ve borrowed, but it’s not directly tied to an item.

This makes it harder for the lender to get their money when you don’t pay up, so unsecured debt usually has a higher interest rate. It also means you’re more likely to face debt collectors or lawsuits if you miss payments. And if you think you can make it go away by ignoring it, unsecured debt just turns into zombie debt and can come back and eat you (well, eat your money).

This kind of debt can pile up quick if you’re not careful. With secured debt, you’re more motivated to make payments because you might lose your car, home or something you use every day. With unsecured debt, it’s not as easy to see where the money you’re borrowing is going, but you still need to pay off the debt ASAP!

Revolving Debt

Revolving debt is an open line of credit. It’s when you enter into a cycle of borrowing money and paying back—just to borrow more money. It’s kind of like the revolving door you use to enter a mall to buy things with your line of credit. You can borrow up to a certain amount (called a credit limit), and as long as you make the minimum payment by a specific date each month, you can keep spending.

Revolving debt is your credit card, store card (we’re looking at you, Target), or even the tab you’ve racked up at your local hardware store.

With this type of debt, it’s easy to feel like you have your credit under control because the minimum payments you make are usually super small compared to your credit limit. But only paying the minimum each month (or anything less than the full balance, for that matter) means you have to pay interest on the rest of your balance later.

And if you miss a payment, you’ll owe late fees on top of everything else! No gaming system or pair of shoes is worth the mess you could be in if you use a credit card.

Even if you pay off your entire balance at the end of the month, there’s still a period of time where you owe someone else, whether it’s a store or a credit card company. That thing you bought technically isn’t yours until you’ve paid off the balance. Time to do a 180 and revolve right out of this debt for good.

Nonrevolving Debt

Nonrevolving debt is a line of credit that can’t be used more than once. It’s a car loan, a business loan, a student loan or a mortgage. You borrow a specific amount of money and pay it back in installments before a certain date. And your minimum payment each month usually depends on how much you originally took out. Once you’ve paid the loan off, it’s gone, and you don’t get any more funds to spend.

Like all debt, interest is also involved. But with nonrevolving debt, you’re usually dealing with some larger numbers. So even if you make the minimum payment each month, you’re still going to have to pay interest on the remaining balance. These loans are probably going to take some time to pay off (especially a mortgage), which means you will end up shelling out more than you borrowed to begin with. And depending on your interest rate, that can add up to some serious cash.

For example, let’s say you took out a 30-year $250,000 mortgage at 3.8% interest. When all is said and done, your house will actually cost you almost $420,000 ($250,000 plus about $170,000 in interest)! That. Is. Insane!

Sneaky Debt

Cars, motorcycles, couches, computers, dishwashers, even pets—you can finance anything nowadays. You’ve probably seen the flashing, neon signs: zero percent APR! Or 90 days same as cash! These, friends, are examples of sneaky debt. Salespeople know most folks don’t pay off that furniture set or treadmill within 90 days—and the moment your time is up, crazy interest rates kick in with full force.

Even credit card points and airline miles are another way to tempt people to spend more money in the hopes of getting a very small reward. Don’t fall for these debts disguised as deals. They’re not worth it!

There’s also another kind of debt you may not even know is debt . . . and it’s in your pocket. Yep, cell phones fall into the sneaky debt category because many of us don’t think twice before signing a contract and agreeing to pay it off every month for the next two years.

But it’s secured debt. It may not seem like a big deal, but the truth is, you still owe on that device, and it could be taken from you if you don’t pay up. Instead of financing the latest iPhone, you’d be better off saving up to pay for the whole thing with cash.

Good Debt vs. Bad Debt

Good Debt vs. Bad Debt

Spoiler alert: There’s no such thing as good debt. That’s like saying there are good kinds of the flu.

Take student loans, for example. Some folks think student loans are “good debt” because they help a student better themselves. But really, loans just end up getting in the way and holding the borrower back for years. Just ask the thousands of people who are still drowning in student loan debt because of an English degree they got back in 1998. There are ways to get a quality education that will help your career, but student loans aren’t the answer.

What about a mortgage? We get this question all the time. Yes, a mortgage is debt, but it’s the only kind we won’t yell at you about. Even then, we’ve got some guardrails to keep you from derailing your goals—and your life. If you can’t pay cash for your house (that’s our favorite option), we tell you to only take out a 15-year fixed-rate mortgage. And your monthly payment should be less than 25% of your total take-home pay. Plus, you need a good down payment of 10–20%.

How to Get Out of Debt

Take a moment and dream. What would your life look like without debt? What would you do if you didn’t have any payments holding you back? Would you travel more, start a business, or bless others?

Debt keeps you in the past, makes you worry about the present, and steals from your future. The sooner you call debt what it is—dumb—the sooner you can take back your income and kick Sallie Mae and those nasty credit cards out of your life. Here’s how to pay off your debt once and for all:

Make a budget.

The first step in paying off debt is to be more intentional with your money. And the best way to do that is with a zero-based budget. When you give every dollar a job, you make sure the bills get paid while you make progress on your goals. Tracking your expenses every month also makes it easier to see where you’re overspending and where you can cut back. Do you need to ditch the cable bill to pay off that credit card? Maybe it’s time you trimmed your grocery budget so you can throw even more money at your debt.

A budget tells your money where to go so you’re not left wondering where it went. If you’re tired of having too much month at the end of your money, a budget is your new best friend. (And we've got a free budgeting tool called EveryDollar, if you need one!)

Use the debt snowball.

If you’ve got more than one type of debt fighting for your attention, the debt snowball method will give you focus. It’s the best way to pay off debt because it helps you prioritize your different debts and gives you motivation to tackle them one by one.

Here’s how it works: First, you list all your debts from smallest to largest (regardless of interest rate). Then you make minimum payments on all your debts, except the smallest debt—that’s the one you attack with intensity. Get a second job, sell your stuff, use that budget! Do whatever it takes to throw as much money as possible at that littlest debt. Once that one is done, take what you were paying on that first debt and add it to your payment for the next debt. Keep doing this until all your debts are gone for good!

When you give yourself little wins, you’re more likely to keep attacking your debt. Think of it like a snowball rolling downhill and gaining momentum along the way. You can even use our debt snowball calculator to figure out how soon you could be debt-free!

Get on a Plan That Works

Here’s the deal: You can either let your money control you, or you can control your money. If you’re ready to call it quits on debt and tell your money what to do, download the EveryDollar app.

EveryDollar is an amazing budgeting tool that doesn’t just help you track expenses . . . it’s a one-stop shop for planning out your long-term money goals—like getting out of debt. EveryDollar gives you a real strategy to knock out that debt, cheers you on as you go, and gets you on the road to real financial peace. How does that sound?

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.