Real Estate

Home Affordability Calculator

Take the stress out of buying a home. See your affordable price range, estimate how much you can borrow, and feel confident your house fits your budget.

A debt-to-income (DTI) ratio is how much you owe (debt) divided by how much you earn (income). Lenders use it to check the risk of lending you more money. Find out your DTI below.

The EveryDollar app helps you cut costs and pay down debt. That means a better DTI ratio—and a better chance of getting approved for a mortgage. Start budgeting today!

A debt-to-income (DTI) ratio is the percentage of your monthly income that goes toward debt. Lenders use your DTI to see how you manage monthly payments and to determine whether or not to loan you money.

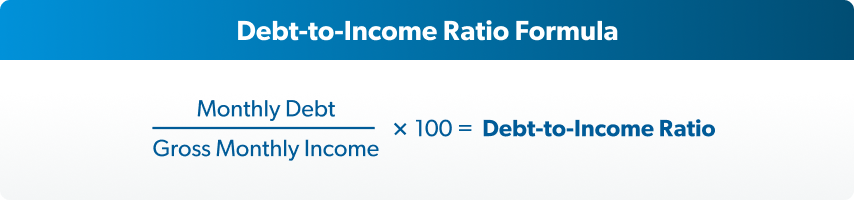

Your debt-to-income ratio is how much you owe (debt) divided by how much you earn (income). To figure out your DTI ratio, just add up your monthly debt payments and divide the total by your gross monthly income (that’s your wages before taxes and other deductions are taken out).

Monthly Debt / Gross Monthly Income x 100 = Debt-to-Income Ratio

You don’t need to factor in common living expenses (like utilities and food) or paycheck deductions (like health insurance or 401(k) contributions). But you should include all types of debt, like:

You’ll also include recurring monthly payments—like rent, child support or alimony—even though they aren’t technically considered debt.

But think about it like this: Lenders need an accurate picture of how much you’re spending each month so they can have confidence you’ll be able to pay back the loan—that’s why they’re not just looking at your debt.

So, to sum it up, include all your monthly minimum debt payments and recurring or legally binding payments in your debt-to-income ratio—but not basic monthly bills.

Again, your gross monthly income is what you make before taxes are taken out. Don’t forget to include any money that comes into your bank account on an average month. That includes your salary or wages, tips, bonuses, child support, alimony, as well as pensions or Social Security.

For example, let’s say you pay $600 a month in minimum debt payments (for student loans and a car payment) plus $1,000 per month for a mortgage payment. Before taxes, you bring home $5,000 a month. To calculate your DTI, you would add up your monthly debt and mortgage payment ($1,600) and divide it by your gross monthly income ($5,000) to get 0.32.

Multiply that by 100 to get a percentage. So in this case, your debt-to-income ratio would be 32%.

Now, it’s your turn. Plug your numbers into our debt-to-income ratio calculator above and see where you stand.

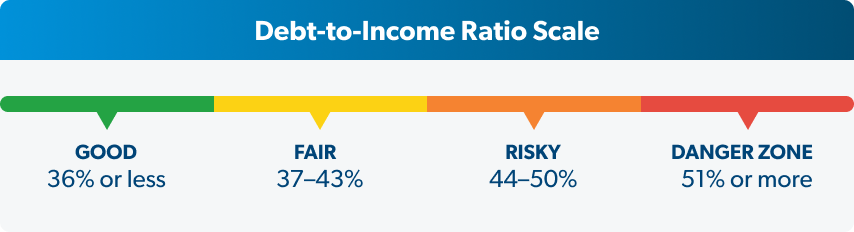

Now that you know how a debt-to-income ratio is calculated, you might be wondering what lenders think of your score. Each lender has their own idea of what qualifies as a good DTI, but here’s a breakdown of the general industry standards.

DTI of 36% or less: Lenders view a DTI of 36% or under as good, meaning they think you can manage your current debt payments and handle taking on an additional loan.

DTI of 37–43%: In this range, lenders get nervous that adding another loan payment to your plate might be challenging, especially if an emergency pops up. You won’t necessarily get turned down for another loan, but lenders will proceed with caution.

DTI of 44–50%: When your DTI gets to this level, you’re almost too risky for lenders. You might get approved for smaller loans, but not a mortgage.

DTI of 51% or higher: At this point, you’re in the danger zone, and lenders probably won’t lend you money. With a DTI over 50%, that means over half of your monthly income is going toward debt. After covering living expenses, like groceries and insurance, there’s not much left for saving or covering an emergency—and another loan could tip you over the edge.

But listen, just because your DTI is considered good by industry standards and you qualify for another loan, it doesn’t mean you should borrow more money. Debt steals from you now and in the future. Your income is your most important wealth-building tool, and when it's all going toward debt, it's hard to get ahead with your money.

Bottom line? The best DTI is 0%. So don’t focus so much on your number—focus on paying off your debt.

When applying for a mortgage, lenders will look at two different types of DTI ratios: a front-end ratio and a back-end ratio.

Front-end ratio: A front-end ratio only includes your total monthly housing costs—like your rent, mortgage payment, monthly homeowners association fees, property taxes and homeowners insurance.

Lenders prefer your max front-end ratio to be 28% or lower. But we recommend you keep your total housing costs to no more than 25% of your take-home pay to avoid becoming what’s known as “house poor.”

Back-end ratio: A back-end ratio (which is what our DTI Ratio Calculator above gives you) includes your monthly housing costs plus any other monthly debt payments you have, like credit cards, student loans or medical bills. Lenders typically care more about the back-end ratio because it gives them a better picture of your average monthly payments.

Every mortgage lender has their own DTI limits. For example, the Federal Housing Administration (FHA) allows you to have a front-end ratio of 31% and a back-end ratio of 43% to qualify for an FHA loan.1

If your blood pressure shot up when you saw your DTI, take a deep breath. You actually have more control over that number than you might think!

The key to lowering your DTI is to decrease your monthly debt or increase your monthly income. Or better yet, both! Here’s what you can do to lower your debt-to-income ratio.

The brand-new car that’s calling your name? That boat you’ve been eyeing for years? You’re just a loan or two away from making them “yours.” Nope, hold it right there! Borrowing more money will just make your DTI percentage rise (and also your stress level). You may be tempted to add more payments to your plate, but you should really be working to get rid of the payments you already have.

Pick up a few extra hours at work. Snag a side hustle. Ask for a raise. Anything you can do to get more money coming in each month will help lower your DTI. But don’t just earn more money for the sake of improving your debt-to-income ratio. Use that extra cash to pay off your debt too!

Minimum payments equal minimal progress. Seriously, if you’re only paying your minimum payments on your debts each month, those balances will hang around forever. And nobody wants that. To pay off debt faster, start by tackling your smallest debt first—not the one with the highest interest rate (we call this the debt snowball method). When you use the debt snowball method, you’ll get quick wins and see progress right away. And that’ll motivate you to pay off the rest of your debt even faster.

Downloading a budgeting app (like EveryDollar) won’t make your DTI ratio magically shrink. But what a budget will do is help you visually see where your money is going each month and track where you’re overspending. If you cut back in those areas, you’ll have more money to throw at your debt every single month—which will lower your DTI (and get you closer to a life without debt holding you back).

A lot of companies will say that keeping your debt at a level you can manage is a sign of good financial health. But let’s be honest. Even if your DTI ratio is considered good, that still means over a third of your paycheck is going to stuff you don’t own. Sure, it might be “manageable” by a lender’s standards, but do you really want that much of your paycheck going in someone else’s pocket?

The truth is, lenders aren’t helping you out by accepting your loan application. The interest you pay on the loan is actually helping them out. You continue to feel like the current is pulling you under, and they profit off you staying there.

So, don’t ask, “Can I take on another payment?” Instead, ask, “Do I want to be even more strapped than I am right now?”

Just think. If you didn’t have any of those payments at all, how much more breathing room would you have in your finances? In your life?

The real sign of financial health (and freedom!) is you being in control of your money—100% of your paycheck going into your account—so you can save more, spend without worry, and build the future you really want. Without owing anyone a thing.

Your DTI is determined by your monthly debt payments and your monthly gross income (before taxes). This includes:

What’s typically not included in determining your DTI:

Your DTI doesn’t directly affect your credit score. That’s because your credit score doesn’t take into account your income. But lenders may look at both your DTI and your credit score.

Generally, lenders prefer your back-end ratio to be below 36%, but some will allow up to 50% when applying for a mortgage. It really depends on the particular lender you’re working with and if you’re doing automated vs. manual underwriting.

But before you apply for a mortgage loan, a better question to ask is, “How much house can I afford?” When you’re buying a house, it’s easy to get excited and take on more than your budget can actually handle. So, use our mortgage calculator to make sure you don’t get in over your head.

When you find your dream home, you don't have to wonder if you can actually afford it. Churchill Mortgage is here to help!

Learn more about the home-buying process and how to get a mortgage.

Take the stress out of buying a home. See your affordable price range, estimate how much you can borrow, and feel confident your house fits your budget.

Figuring out how to get a mortgage can sound intimidating, but it’s not as tricky as it seems! You just need to follow these eight steps—then you can get back to choosing paint colors for the kitchen.

Buying your first house can be overwhelming, but these tips will help you buy with confidence and make sure your new house becomes a blessing, not a burden.