Cash Stuffing: How It Works

8 MIN READ | MAY 11, 2026

By

By

Link copied!

Unable to copy link. Please try again.

Key Takeaways

- Cash stuffing, also called the envelope system, means putting cash into labeled envelopes for each category and only spending what’s in each one.

- Each envelope has a set amount for the month, and once it’s gone, you stop spending in that category.

- Paying with cash makes spending feel real, which helps you spend less than when you swipe a card.

- When an envelope runs out before the month ends, you can see exactly where you need to pull back on your spending.

- Any leftover cash should be put to work toward goals like building an emergency fund or paying off debt.

Cash stuffing may be trending on TikTok, but it’s nothing new. It’s a hands-on way to follow a zero-based budget, and it’s been helping people stop overspending and get out of debt for decades.

Here's A Tip

Cash stuffing is simple. You put physical cash into labeled envelopes for each spending category—groceries, gas, fun money and more. When the envelope is empty, you’re done spending.

Today, most people use digital budgets to track what they’ve already spent. You make a late-night McDonald’s run, then log it. You impulse buy a new pair of sneakers, then log it. But cash stuffing flips that. You decide what you’ll spend before you spend it, and then you stick to it.

In other words, you give every dollar a job before the month begins. And then you stuff those dollars into labeled envelopes until you spend them. No swiping, guessing, or asking “Where did my paycheck go?” two weeks later.

What Is Cash Stuffing and Why Does It Actually Work?

Cash stuffing is a budgeting method where you divide your monthly income into labeled envelopes, one for each spending category, and only spend what’s inside. When the money’s gone, it’s gone, and you’re done spending in that category for the month.

Sound familiar? It should. Cash stuffing is just the envelope system with a trendier name.

It works because it changes your behavior. People consistently spend more when they use cards than when they use cash. In fact, some studies have found that shoppers spend up to four times as much when paying with cards versus cash.1 That's because spending doesn't feel as real when you're not physically handing over cash. When you’re at the grocery store watching the total climb past your budget, and you’re the one handing over twenties, it hits different.

Psychologists call that the “pain of paying,” and the envelope system uses that feeling to keep you from overspending and help you stick to your plan. Swiping a card doesn’t feel like spending real money, but cash does. That feeling is your budget working.

How Does the Cash Stuffing System Work? (Step by Step)

Here’s how to go from your paycheck to fully stocked envelopes. Follow these steps in order.

- Build your zero-based budget. Start by listing your income and expenses so every dollar has a job. In a zero-based budget, your income minus expenses equals zero. This is the plan that drives everything else.

- Choose the categories to use cash for. Focus on the areas where you tend to overspend, like groceries, gas, dining out and fun money. Fixed bills like rent, insurance and utilities stay in your checking account as automatic payments.

- Decide how much cash to put in each envelope. Set a monthly amount for each category, then divide it by how often you get paid. That tells you how much cash to pull each payday.

- Withdraw cash and stuff your envelopes. When your paycheck hits, go to the bank and withdraw the cash you planned. Label your envelopes and put the right amount in each one so your categories are funded.

- Spend only what’s in the envelopes. Use the cash for its assigned category and nothing else. (That means no sneaking money from the gas envelope because the restaurant envelope ran dry.) When the envelope is empty, you’re done spending for the month.

- Put leftover money to work. At the end of the month, if you have extra cash, don’t let it just sit there. Give it a clear assignment based on where you are in the Baby Steps. If you’re on Baby Step 1, add it to your starter emergency fund. On Baby Step 2, throw it at your smallest debt and keep the snowball rolling. Once you’re out of debt, move it into savings and investments.

How Do You Start Cash Stuffing?

Cash stuffing for beginners is simpler than it looks. You really just need a budget, some envelopes and your next paycheck.

If you want something more durable than plain paper envelopes, the Ramsey Cash Envelope System is an easy way to keep your categories organized and your cash in one place.

When you’re set up correctly, it looks like this:

- Every dollar in your budget has a job.

- Your main spending categories have envelopes.

- Each envelope has a clear monthly amount.

- You know how much cash to pull each payday.

- Your envelopes are labeled and ready to use.

- You’re reviewing and adjusting after your first month.

Use EveryDollar to build the budget behind all of this. It shows you the full plan on paper, and cash stuffing helps you follow through in real life.

Find Margin You Didn’t Know You Had With EveryDollar

The EveryDollar budgeting app helps you find extra money every month so you can beat debt, build wealth, and make progress. Every. Day.

What Envelopes and Categories Should I Use?

You don’t need an envelope for every category right away. Start with three to five areas where you tend to overspend and build from there. As you get more comfortable, you can always add more.

Here are some of the most common envelope categories:

- Groceries

- Dining out

- Personal care

- Clothing

- Fun money

- Entertainment

- Gifts

Groceries and dining out are usually the biggest game-changers because those are the categories where money tends to disappear fast if you’re not paying attention.

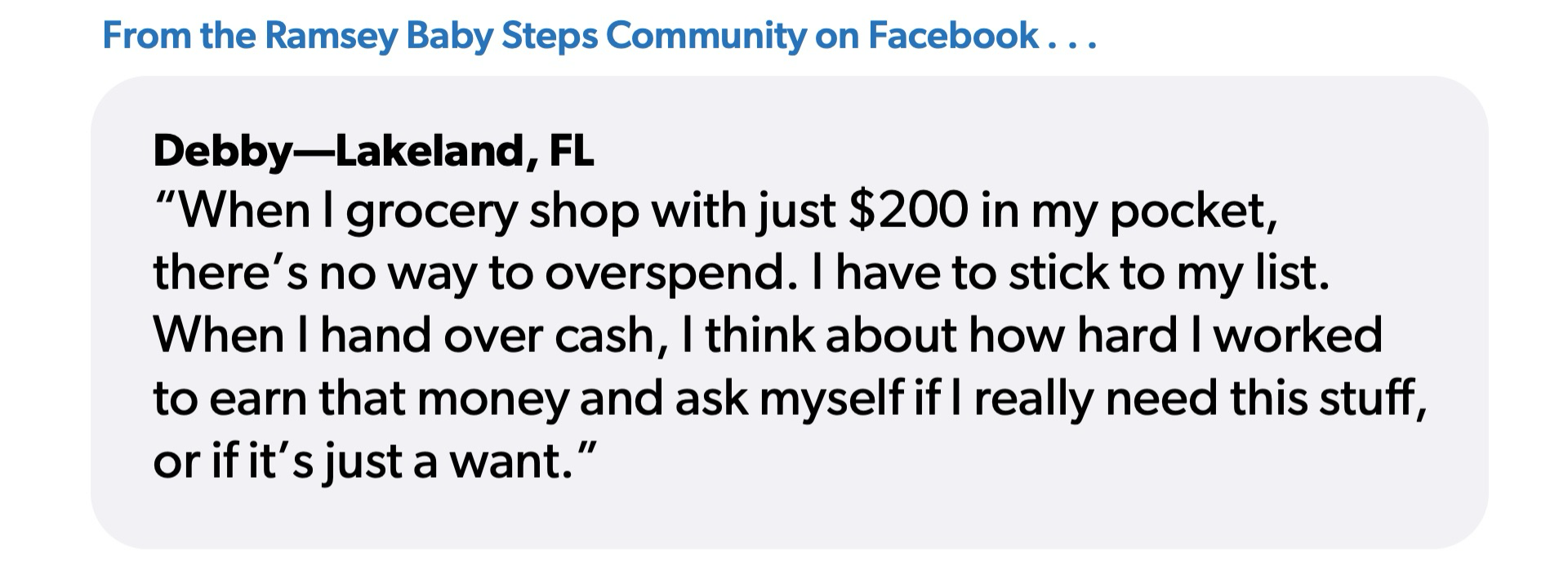

As Debby from the Ramsey Baby Steps Community puts it, “When I grocery shop with just $200 in my pocket, there’s no way to overspend. I have to stick to my list. When I hand over cash, I think about how hard I worked to earn that money and ask myself if I really need this stuff, or if it’s just a want.”

Use these guidelines to decide where to start:

- Pick categories where you tend to swipe without thinking.

- Focus on in-person spending (envelopes don’t work as well for online purchases).

- Leave recurring bills like your mortgage, utilities and insurance on autopay in your checking account.

Real-World Examples

Use your recent spending as a starting point, then adjust as you go. The first month is about getting a clear picture of your habits and making small corrections.

If you’re not sure what to budget, these are example monthly amounts for common spending categories based on different household sizes. We looked at consumer spending data and common budgeting recommendations to put these examples together, but your numbers will look different depending on your income and where you are in the Baby Steps. This is just a starting point.

|

Category |

Single Person (~$40K income) |

Family of Four (~$65K income) |

|

Groceries |

$350/month |

$900/month |

|

Dining Out |

$100/month |

$250/month |

|

Personal Care |

$40/month |

$80/month |

|

Clothing |

$50/month |

$100/month |

|

Fun Money |

$50/month |

$100/month |

|

Entertainment |

$100/month |

$250/month |

|

Gifts |

$40/month |

$80/month |

Use our Budget Calculator to estimate category amounts based on your monthly take-home pay and national averages. Then adjust the numbers to fit your situation and build a zero-based budget.

How Much Cash Should You Withdraw and When?

Once you’ve set your category amounts, the next step is figuring out how much cash to pull each payday.

The answer depends on how often you get paid.

The Withdrawal Formula

To figure out how much cash to pull each payday, use this formula:

Monthly category amount ÷ number of paychecks = cash per paycheck

The goal is to break your monthly budget into smaller, per-paycheck amounts so you don’t blow through the whole category at once. Here’s what that looks like with a $400 grocery budget:

|

Pay Schedule |

Paychecks/Month |

Withdraw Per Paycheck |

|

Weekly |

~4 |

$100 |

|

Biweekly (every 2 weeks) |

2 |

$200 |

|

Monthly |

1 |

$400 |

Then repeat that same math for every envelope. If your grocery budget is $250 a month and you’re paid every two weeks, you’ll pull $125 each payday. If dining out is $100 and you’re paid weekly, that’s $25 per week. Write those amounts on your envelopes so there’s no guessing.

Which Expenses Go in Envelopes vs. Stay in Checking?

If you’re not sure what belongs where, here’s a simple way to think about it:

|

Expense Category |

Where It Goes |

|

Groceries |

Envelope |

|

Gas |

Envelope |

|

Dining Out |

Envelope |

|

Fun Money |

Envelope |

|

Entertainment |

Envelope |

|

Clothing |

Envelope |

|

Giving |

Checking (auto) |

|

Rent/Mortgage |

Checking (auto) |

|

Insurance |

Checking (auto) |

|

Utilities |

Checking (auto) |

|

Debt Payments |

Checking |

Notice we listed giving as an automatic payment. That’s because it belongs at the top of your budget (you don’t want to run out of envelope money before you give).

If your church offers online giving, setting it up automatically can help you stay consistent. If not, plan for it in your budget and give first.

What Are the Pros and Cons of Cash Stuffing?

Cash stuffing isn’t the only way to budget, but it’s one of the most effective if you tend to swipe without thinking. Here’s a quick look at the pros and cons:

|

PROS |

CONS |

|

Stops overspending because when the envelope is empty, you’re done. |

Getting cash can take extra time depending on your bank. |

|

Makes you more aware of your spending every time you pay. |

You have to carry and keep up with envelopes. |

|

Builds discipline because cash feels more real than swiping a card. |

Cash doesn’t work for some bills or online purchases. |

|

Cuts down on impulse buys since you can’t spend what you don’t have. |

It can feel inconvenient in a mostly digital world. |

|

Helps you make progress faster by putting leftover money toward your goals. |

|

|

Keeps your budget simple and easy to follow. |

Start Cash Stuffing This Pay Period

Cash stuffing works because it makes your budget real. Instead of wondering where your money went, you’re deciding where it goes before you spend it.

Build your zero-based budget in EveryDollar, then use cash for the categories where you tend to overspend. It’s a simple shift, but it can completely change how you handle money.

Start today, stick with it, and adjust as you go. That’s how you build better spending habits!

Next Steps

- Build a zero-based budget so every dollar has a job before the month begins.

- Choose three to five spending categories where overspending happens most and create labeled envelopes for them.

- Only spend what’s in the envelopes each month, then put any extra money toward your financial goals.

Frequently Asked Questions

-

Is cash stuffing safe?

-

Yes, if you use common sense. Keep most of your cash at home in a secure place, and only carry what you need for the day. You don’t need to walk around with $800 in your purse or wallet.

-

What if I run out of cash in an envelope before the month ends?

-

Stop spending in that category or move money from a lower priority envelope (like fun money). That moment is the system working. It shows you where your plan needs adjusting or where your habits need to change.

-

Can I use cash stuffing if I have debt?

-

Yes, and you should! Cash stuffing helps you control spending so you have more money to put toward your debt snowball.

-

What do I do with leftover cash at the end of the month?

-

Give it a job. On Baby Step 1, add it to your starter emergency fund. On Baby Step 2, throw it at your smallest debt. After that, move it to savings.

-

Can I use a debit card instead of cash envelopes?

-

You can, but it’s not the same. People tend to spend more when they swipe. Cash slows you down and helps you stick to your plan. Use EveryDollar to track your budget, then use cash where you need more control.

-

How do I handle irregular or large expenses with cash stuffing?

-

Use sinking funds. Set aside a small amount each month for things like car repairs, holidays or annual bills. That way, those expenses don’t catch you off guard.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.