Is Your 401(k) Enough for Retirement?

By

By

Key Takeaways

- A 401(k) is a great place to start saving for retirement thanks to relatively high contribution limits, a possible employer match and tax advantages.

- If you don’t like your 401(k)’s options, at least invest up to the match—then save for retirement through a Roth IRA.

- A Roth IRA is a great supplement to a 401(k) because it provides tax-free growth, more flexibility and a wider range of investment options.

- Talk to an investment pro for help navigating your investment choices.

A 401(k) can sometimes be enough for retirement if you have strong investment options and you’re able to invest 15% of your income.

How do we know? Ramsey Solutions has helped millions of people become debt-free and build wealth for their future. And according to our National Study of Millionaires (the largest survey of millionaires ever done), 8 out of 10 millionaires said their 401(k) was their main wealth-building tool.

Those millionaires are the kind of people who live next door to you (teachers, managers, accountants)—they just used their workplace retirement plans to become Baby Steps Millionaires. It’s not the most exciting way to invest . . . but it is exciting to become a millionaire!

So, is your 401(k) enough?

- It might be if you have access to a Roth 401(k), solid investment options and are able to invest 15% of your income.

- It might not be if one or more of those above points aren’t true in your case. You may need to look at options outside your workplace retirement plan, like a Roth IRA.

Let’s take a closer look at the 401(k), how it fits into retirement planning, and how you can team it up with a Roth IRA to build a solid nest egg for your golden years.

How Much Should You Save for Retirement?

The Ramsey way to save for retirement is to invest 15% of your gross income in tax-advantaged retirement accounts—usually through your 401(k) at work.

But you should only start saving for retirement once you’re completely out of debt and have a fully funded emergency fund in place. If you still have consumer debt lying around, pause all your investing until you pay it off.

Here's a Tip

We don’t count the company match toward your 15% goal. So if Sarah earns $80,000 a year and her employer matches up to 5%, she’ll invest $12,000 to reach 15%. The 5% her employer contributes ($4,000) is the icing on the cake.

What Are the Benefits of a 401(k)?

Your 401(k) plan makes it easy to get started investing—you can pretty much “set it and forget it” so your contributions automatically come out of your paycheck. On top of that, your 401(k) comes with several other benefits that make it awesome.

Higher Contribution Limits

One of the great things about a 401(k) is that it has higher contribution limits than an IRA.

For 2026, the 401(k) contribution limit is $24,500. If you’re 50 or older, you can invest an extra $8,000 as a catch-up contribution. And if you’re age 60–63, your catch-up limit is even higher at $11,250.1

Free Money From Employer Match

If your employer matches your contributions (and most do), that means when you put money into your account, they do too. It's essentially free money added to your investment—so take advantage of it.

Your employer’s match is usually put into a separate bucket as pretax contributions—so it grows tax-deferred. You’ll pay taxes on those dollars when you make withdrawals in retirement.

But there’s a wrinkle.

The SECURE 2.0 Act allows employers to provide their match as Roth contributions. That means matching funds are treated as taxable income. You’ll pay taxes on that money when it’s earned instead of later in retirement—when your savings have had time to grow. (More employers are starting to offer matching funds as Roth contributions, so keep an eye out for that.)

Here's a Tip

What if your employer doesn’t match contributions? If that’s the case, max out your Roth IRA. Then if you still have money to invest, you can at least take advantage of your 401(k)’s tax benefits (more about that later).

When Is a 401(k) Not Enough for Retirement?

If it’s not clear by now, we love the 401(k) for retirement investing! But as great as it is, it's not always enough on its own.

Your 401(k) may not be enough if:

- Your investment choices are limited or not great

- You don’t have a Roth option

- Plan fees are high

- You can't reach your 15% goal using your 401(k) alone

Let’s take a look at some situations where your 401(k) isn’t enough.

You don’t like your investment choices.

Most companies partner with a brokerage firm to administer 401(k) plans for their employees. Those firms usually provide a limited menu of investment options—mostly mutual funds, index funds and target-date funds.

You might look at your options and feel . . . underwhelmed. If that’s the case, pick the best options available and invest up to the match. Then invest in a Roth IRA where you have more control.

You don’t have access to a Roth 401(k) option.

About a decade ago, only half of employers offered a Roth 401(k). But that number has almost doubled since then: More than 95% now do.2

If you’re one of the few without access to a Roth 401(k), that’s okay. Invest up to the match, then open a Roth IRA and max it out before putting any more money into your workplace retirement plan.

Your fees are too high.

Don’t get so obsessed with fees that you find yourself stepping over dollars to pick up pennies. But make sure your 401(k) plan isn't charging high administrative or maintenance fees.

Why You Should Use a Roth IRA With Your 401(k)

The best tool you can use for investing beyond your 401(k) is a Roth IRA. We surveyed more than 10,000 millionaires in our National Study of Millionaires. A huge majority (74%) said they invested outside of their workplace retirement plan.3 This isn’t an either/or situation—it’s both/and.

The Roth IRA is an investing account that lets you save for retirement on your own regardless of your employer.

Like the Roth 401(k), a Roth IRA is funded with after-tax contributions—meaning there’s no tax break now, but you do get tax-free growth and withdrawals later. Contribution limits for Roth IRAs are much lower than they are for 401(k)s, though. For 2026, you can invest up to $7,500 in a Roth IRA ($8,600 if you’re 50 or older).4

The Roth IRA is the butter to the 401(k)’s popcorn (they’re better together)! Here’s why a Roth IRA is the perfect choice to team up with your 401(k):

- Tax-free growth and withdrawals: When you retire, you’ll be able to use the money in your Roth IRA tax-free. Did you catch that? Tax-free!

- Flexibility: You can work with an investment pro to choose from thousands of mutual funds to invest in through your Roth IRA. That means you can choose high-performing funds and diversify with different fund types.

These may seem like minor details, but they can make a big difference in the size of your nest egg over time.

Why Roth Accounts Are Better for Retirement Taxes

When you sign up for your 401(k) plan, you’re likely to find you have two options: a traditional 401(k) or a Roth 401(k). This is a big decision with a major impact on your nest egg.

Both plans have the same contribution limits and come with the same employer match, but one difference between the two is huge: how your contributions, investment growth and withdrawals are taxed.

Roth 401(k) vs. Traditional 401(k)

|

Feature |

Roth 401(k) |

Traditional 401(k) |

|

Contributions |

After-tax |

Pretax |

|

Tax Break Now |

No |

Yes |

|

Growth |

Tax-free |

Tax-deferred |

|

Withdrawals |

Tax-free |

Taxed as income |

|

RMDs |

None (SECURE 2.0 removed RMDs for many plans) |

Yes (starting at age 73) |

|

Best For |

Long-term tax savings |

Lowering taxes today |

Contributions to traditional 401(k)s are pretax, which means they lower your taxable income for the year you make them. So you’ll have a lower tax bill next April—but you’ll pay taxes on all the growth and withdrawals in retirement. The IRS also requires you to start taking money out of traditional 401(k)s by age 73. These withdrawals are called RMDs (required minimum distributions).

But Roth plans don’t have RMDs. And Roth 401(k) contributions are funded with after-tax dollars. That means you won’t get a tax break now, but your money will grow tax-free—and you won’t pay any taxes on withdrawals in retirement.

If you have access to a Roth 401(k), you should always pick that option. Nobody knows what tax rates will look like in the future, so it's smart to pay taxes now—before your money has a chance to grow. That way, you can enjoy tax-free withdrawals in retirement.

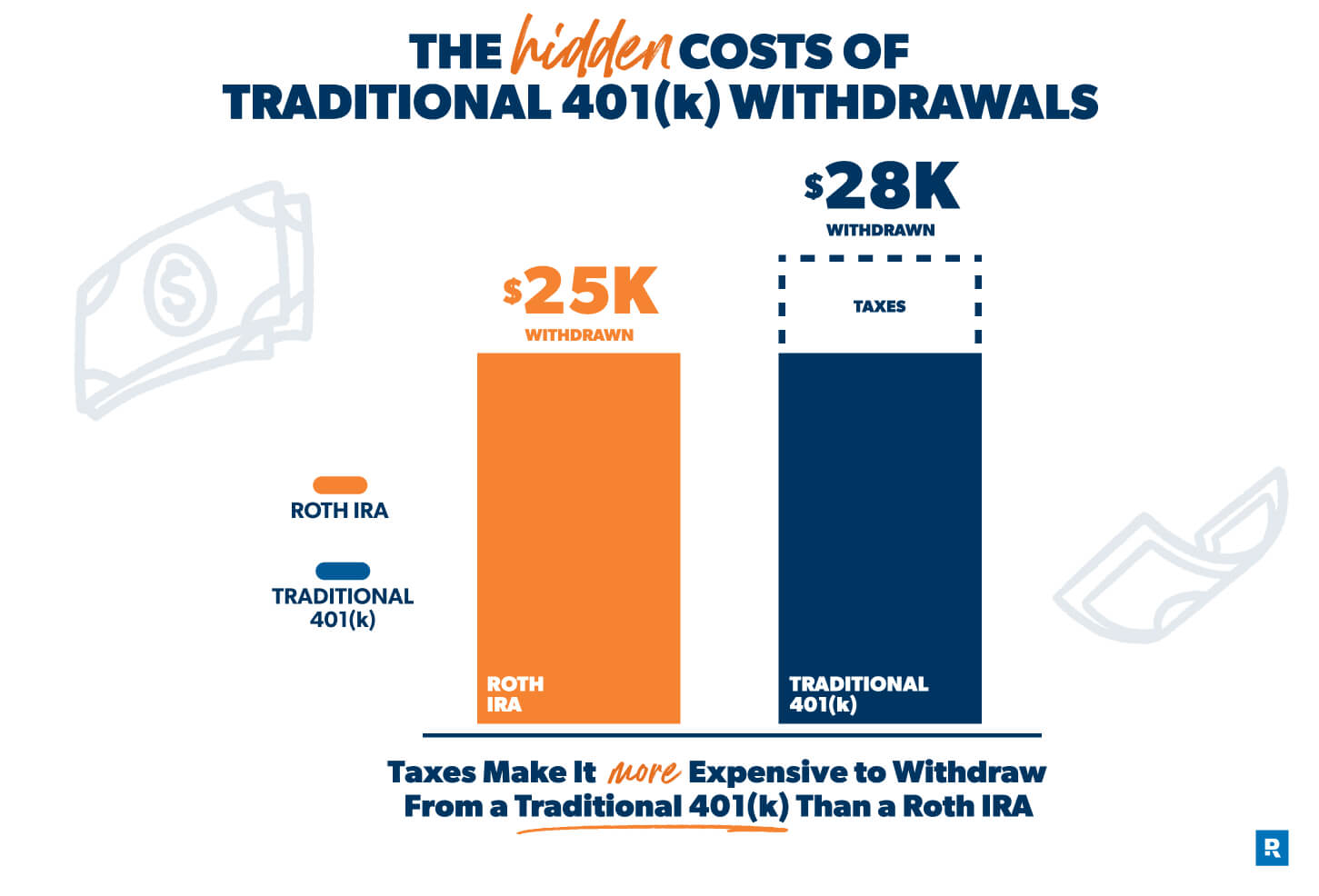

How Taxes Affect Your Retirement Income

Let’s say you’re retired and have both a traditional 401(k) and a Roth IRA. It’s time to start making withdrawals, and you want to withdraw $25,000 from each account for $50,000 of annual income.

Because your IRA is a Roth plan, you can take out $25,000 every year and not owe any taxes on it. No problem there! Since most Roth IRA withdrawals in retirement do not count as taxable income, it puts less stress on you at tax season too.

But your traditional 401(k) is a different story. Those withdrawals do count as taxable income. If your retirement income puts you in the 12% tax bracket, you’ll actually have to withdraw around $28,000 from your 401(k) every year to cover your taxes and still get the income you need.

An extra $3,000 might not seem like much, but it adds up over time. If your retirement lasts 30 years, you’ll end up withdrawing almost $100,000 more from your 401(k) than your Roth IRA just to maintain your income.

Any tax you pay on your investments after retirement adds pressure. Your investments have to bring in higher returns just to pay Uncle Sam. But Roth accounts take taxes out of the picture at the beginning.

It’s a pretty clear choice: Take advantage of Roth IRAs—and Roth 401(k)s—whenever and wherever you can.

How the Flexibility of a Roth IRA Works in Your Favor

If your 401(k) plan doesn’t have great investment options, you can choose from thousands of mutual funds in a Roth IRA. How do you know which funds are right for you?

Work with an investment pro! They can help you choose good growth stock mutual funds and build a diversified portfolio to grow your retirement nest egg.

Here's a Tip

One of the best things you can do with your retirement savings—aside from investing more—is to spread out your investments by choosing a from a wide range of mutual funds. Diversifying your portfolio minimizes risk.

A Roth IRA gives you the freedom to choose a balanced mix of mutual funds for retirement. Split your portfolio evenly across these four types of mutual funds:

- Growth

- Aggressive growth

- Growth and income

- International

How to Combine a 401(k) and Roth IRA

Is it complicated to invest in two retirement accounts? Nope! The hardest part is investing consistently—in other words, behaving yourself. When you invest in your workplace 401(k) and a Roth IRA, you combine the power of the match in your workplace 401(k) with the tax-free withdrawals and flexible fund options of a Roth IRA. That’s a winning combo.

|

Step |

Where to Invest |

Why |

|

1 |

401(k) up to employer match |

Free money! |

|

2 |

Roth IRA (max it out) |

Tax-free growth and flexibility |

|

3 |

Back to 401(k) |

Reach 15% total investing goal |

Let’s say you choose the Ramsey way and invest 15% of your gross income for retirement. If your income were $100,000 in 2026, for example, you’d invest $15,000 into retirement savings.

How do you divide that between your traditional 401(k) and Roth IRA? If you follow our match beats Roth beats traditional rule, here’s what to do:

- If your employer matches contributions up to 4% of your pay, for example, then start by contributing $4,000 to your 401(k) to get the match. You have $11,000 left to invest.

- Next, max out your Roth IRA by investing $7,500. You still have $3,500 to go.

- Go back to your 401(k) and invest the rest to get to your 15% goal. Done!

Bottom line: Your 401(k) and a Roth IRA complement each other really well! Put them to work together to help you make the most of the stock market’s growth, limit your risk, and save for a secure future.

Next Steps

- Learn more about the similarities and differences between a traditional 401(k) and Roth 401(k) so you can make smarter decisions for your retirement.

- Check out the free tools and resources on the Ramsey Investing Hub to get an idea of how much money you’ll need to retire on your own terms.

- Don’t know where to start? Our SmartVestor program can connect you with investment professionals who can help you invest for retirement.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

This article provides general guidelines about investing topics. Your situation may be unique. To discuss a plan for your situation, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.