How to Get Out of a Car Loan

By

By

Maybe you had your eye on the car for a while. Or maybe it was the only decent one you could find after you totaled your old Toyota (RIP Blue Steel).

Either way, you took out a car loan to secure your new (or new-to-you) wheels. And the dealer made it seem like you’d have no problem affording the monthly payments. But now that car loan is starting to feel like a real thorn in your side. And you’re thinking, Will I always have a giant car payment?

Don’t let your ride wreck your finances. We’re going to show you how to get out of a car loan once and for all!

How to Get Out of a Car Loan

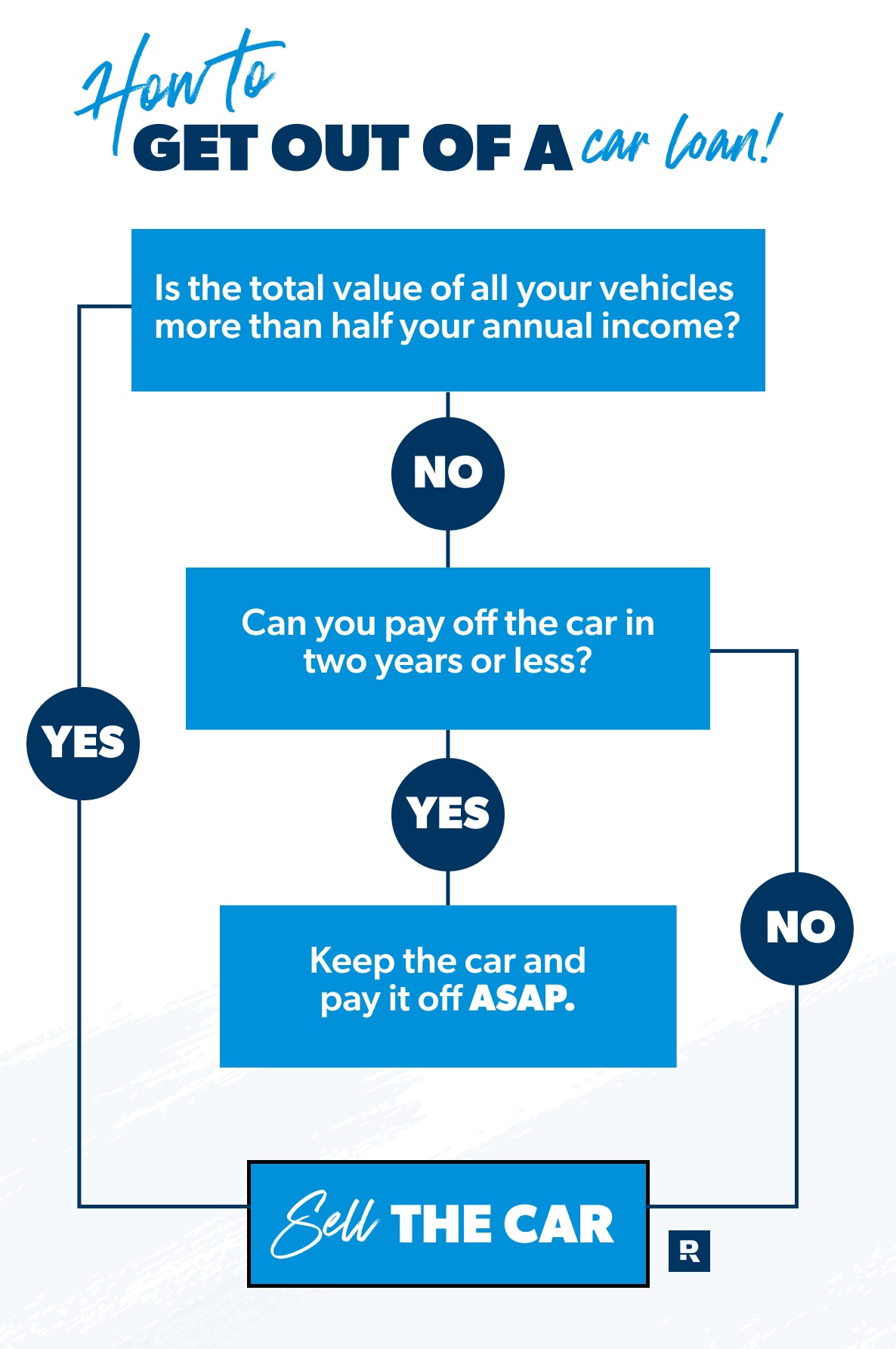

So, how do you get rid of a car payment? Well, you’ve got two main options: Pay off the loan or sell the car. And which one you should do comes down to how you answer these two questions:

1. Is the total value of all your vehicles (things with a motor in them) more than half your annual income?

If yes, sell the car. If not, move on the next question.

2. Can you pay off the car in two years or less?

If yes, keep the car and pay off the loan. If not, sell it.

That’s the super quick answer, but let’s break down each option.

Sell the car.

The quickest way to get rid of your car loan is to sell your car. And if your car payment is tying up your income and keeping you from becoming debt-free in the next two years, then it’s definitely time to get rid of it.

We know this can be painful (especially if it’s your dream car). And we’re not saying you can never drive that same car again later on. But you deserve to own your car, not have your car own you.

Your first step is to check out Kelley Blue Book to find out how much your car is currently worth. The market for used cars is hot right now, so you might be able to get more for it than you think.

Next, start spreading the word that you’re selling. Try Craigslist, social media sites, word of mouth, etc. Then, once you sell the car, you’ll have enough to pay off the loan and get something in your price range (more on that in a minute)!

Find More Margin. Beat Debt Faster.

Paying off debt doesn’t have to take forever. With the EveryDollar budgeting app, you’ll find extra margin every month so you can pay off debt faster.

Pay off the loan.

If the total value of your vehicles isn’t more than half your income and you can be debt-free within two years, it’s time to get serious about paying off your car loan early.

Listen, we know that car payment is already giving you trouble. And the idea of paying more than you are right now might seem impossible. But the sooner you knock out this car loan, the more money you’ll save in interest—and the sooner you’ll be driving a paid-for car!

Plus, there’s a lot you can do to pay off your car loan faster. Start by getting on a budget, cutting back your spending, and picking up a side hustle. Throw as much money as you can toward your car loan. It’ll take some discipline and determination, but you can do it.

But we’ve got one more question for you: Do you really love your car? Like, love it enough to let it keep you in debt longer? Even if you can pay it off in less than two years, you might want to sell it and get something cheaper for a while. (And yeah, you can actually find something cheaper—even in this market!).

What Not to Do With Your Car Loan

What Not to Do With Your Car Loan

Okay, so now that you know which path to take to get out of your car loan, let’s talk about some options you should avoid. They may be tempting, but trust us, they’ll only leave you worse off than when you started.

Refinance Your Current Car Loan

While you might be able to lower your interest rate or get a slightly lower monthly payment by refinancing over a longer term, you’re only addressing a symptom of a much bigger problem. Having a car payment keeps you in debt and paying way more for a car in the long run than you should. Not. Worth. It.

Surrender Your Car

You might think you can just surrender your car back to the lender (that’s called voluntary repossession) and you’ll be off the hook. But that’s a big mistake. Why? The lender will most likely sell the car at auction for a much lower price than you could get for it if you sold it yourself. And then they’ll sue you for the difference.

It’s a giant mess to deal with and totally trashes your credit. And while we don’t put much stock in credit scores, there’s a big difference between having no credit score because you don’t borrow money, and ruining your credit because you’ve made some bad decisions with money. Moral of the story? You want to do everything you can to avoid a repossession.

Default on Your Car Loan

You know what comes before having your car repossessed? Defaulting on your car loan. Yeah, it would be nice to just stop making payments on your car, but that doesn’t come without consequences. It’s only a matter of time before the repo man comes knocking at your door—and then you’re stuck with a lawsuit and no car.

If you signed on the dotted line, you’re responsible for making your car payments, and if you have the money, you should pay it. Otherwise, sell the dang car.

Can I Return a Car I Financed?

Were you so excited the day you got your new ride, only to realize you bought a car you couldn’t afford? It’s easy to get googly-eyed over those heated leather seats and catch a case of car fever. But after that first car payment comes out of your bank account, you might wonder if you’ve made a huge mistake. Can you just take it back to the dealership?

Here’s the deal: Returning a car isn’t as easy as returning a sweater that doesn’t fit. Unless a dealer has listed a specific return policy (usually within a certain time frame or under a certain mileage), that car is legally your responsibility the moment you drive it off the lot. And that means you have to make the payments on it.

The only other way you could return a car after you bought it is if your car is a lemon (aka a car with a manufacturing problem). But lemon laws differ by state, and sorry, but they don’t cover buyer’s remorse.

How to Get Out of an Upside-Down Car Loan

If your car loan is worth more than the value of your car, you’ve got an upside-down car loan on your hands. In this case, your best option is to sell the car for as much as you can, use that money to pay down the loan, and then cover the difference out of pocket.

If you don’t have the cash to pay off the remaining loan amount and get the title from the lender, you’ll need to get an unsecured loan (one that doesn’t require any collateral) to pay off the car loan.

Yeah, you’ll still owe money, but it’ll be way easier to pay off a $5,000 loan than a $15,000 loan—and you won’t have an underwater car pulling you even deeper into debt. Then you can attack that loan with everything you have until it’s going . . . going . . . gone!

How to Buy a Car Without a Loan

So, after you ditch the car loan, what do you do about getting another car? Great question. You buy a car with cash! Yep, you heard that right. You pay for the whole thing in full and up front—no loans, no financing, no leasing.

Here’s how you do it: You find a car you can actually afford. Whether you have $3,000 or $33,000 to spend, you need to stick to your budget. Yes, you can find decent cars without major problems in your price range—you just need to do your research. (And it’s still smarter to buy a used car right now, no matter what everyone’s telling you!)

Now, you may have to settle for a clunker that looks like something your grandma would drive (no offense, granny) and makes a weird noise every time you turn left. But you don’t have to drive a hooptie forever! You just need something cheap to get around while you use the money you were paying toward a car loan to save up for another car.

Let’s say you previously had a $500 car payment. After one year of saving that same amount every month, you’ll have $6,000—and after two years, you’ll have saved $12,000 to buy yourself a better ride! And you can repeat the process as many times as you like. It’s the opposite of instant gratification, but it’s worth it.

How to Get Rid of Your Car Loan for Good

Cars are the most expensive thing we buy that go down in value. It’s like lighting a match to a pile of money every time you drive down the road! And while there’s nothing wrong with having a car, you don’t want to be in debt over it.

But what if you could put that car payment into your bank account instead of handing it over to a lender every month? Imagine driving a paid-for car, having a solid emergency fund, and still having enough money to put toward your future. This isn’t just a dream—it’s totally possible.

If you’re tired of debt holding you back, check out Financial Peace University (FPU). This course teaches you how to take control of your money and make the best financial choices to get where you want to be. And in Lesson 2 of FPU, you’ll learn how to dump your debt (including your car loan) for good!

Don’t let your car loan keep you stuck. It’s time to make progress. Start FPU today!

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.