What Is Buy Now, Pay Later? And Why You Should Avoid It

15 MIN READ | JUN 19, 2026

By

By

Key Takeaways

- Buy now, pay later (BNPL) lets shoppers split purchases into smaller payments over time.

- The problem is, smaller payments can make it easier to overspend and buy things that aren’t in the budget.

- Missing payments can lead to late fees or high interest rates, with some services charging up to 36% interest on longer-term financing options.

- BNPL companies profit when shoppers spend more and take on additional payments.

- BNPL is still a form of debt. Paying with cash is the best way to avoid borrowing and extra costs.

Picture this: You’re scrolling Instagram when you’re hit by an ad for the exact shoes you’ve been wanting. Naturally, you click. The shoes are a little too pricey—especially since you’ve already blown your budget this month. But then you see a banner at the bottom of the page: “Buy now, pay later! Only four easy payments of $19.50.”

Here's A Tip

Buy now, pay later (BNPL) is a financing option that lets shoppers split purchases into multiple payments over time. While many BNPL plans advertise interest-free installments, they can encourage overspending by making it easier to buy things you can’t actually afford.

And that’s exactly what makes them so tempting.

Four payments of $19.50? Shoot, I can afford that right now! Maybe I should go ahead and buy these beauties.

Stop.

Pump the brakes.

Don’t do anything until you hear the truth behind these buy now, pay later payment plans.

What Is Buy Now, Pay Later?

Buy now, pay later is a short-term installment loan that breaks up a purchase into equal payments that you pay over a set amount of time. Most buy now, pay later companies use a pay-in-four model, where you make your first installment payment at checkout and then three more interest-free payments every two weeks. Think of it as layaway and credit falling in love, getting married, and having a baby—a really ugly baby.

Unfortunately, the use of BNPL has skyrocketed. The dollar value of BNPL loans in the U.S. grew from $2 billion in 2019 to $156.7 billion in 2025.1 And according to the most recent industry data available, 53.6 million people took out at least one BNLP loan in a single year, borrowing an average annual amount of $848.2

What’s really scary is that people aren’t just using BNPL for online impulse buys anymore. Many shoppers now use installment plans for everyday expenses like groceries or utilities (or that DoorDash order that’s apparently an emergency). You can walk into a store, open an app, and split a purchase into payments on the spot. Yep, you can get a case of soda for four easy payments of $2.99.

How Does Buy Now, Pay Later Work?

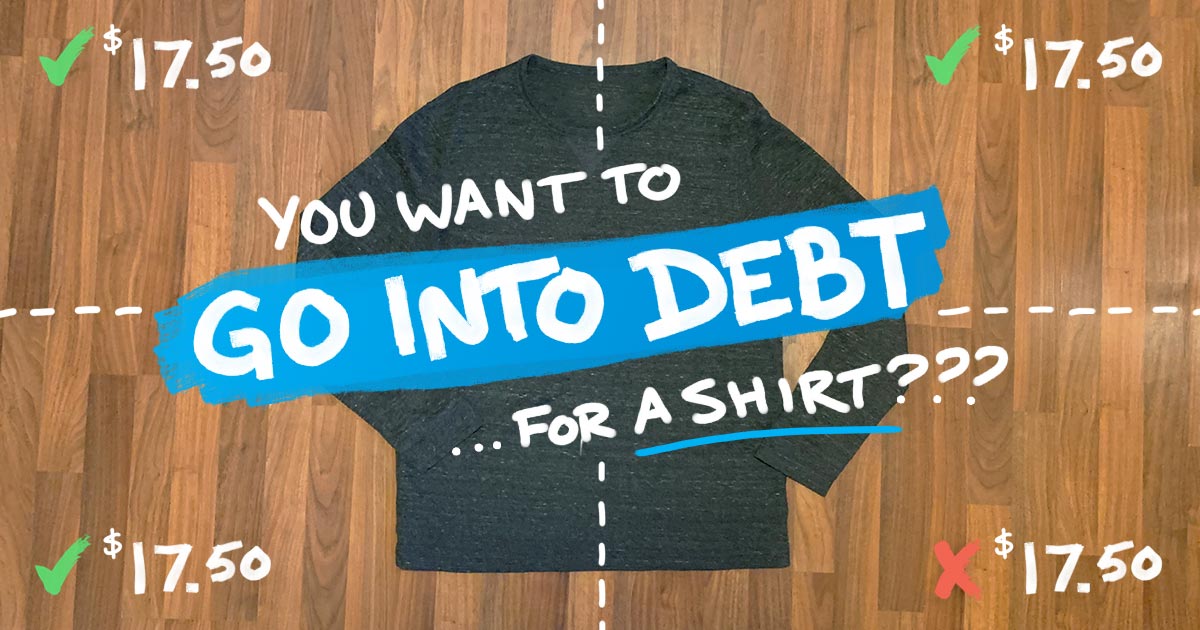

So, let’s say you’re browsing online and spot a new shirt on sale at your favorite store. It’s a little expensive and out of your budget at $70—but because the store uses a buy now, pay later plan, you can have that shirt delivered to your door and only have to pay $17.50 right now.

Oh. But wait. There’s more. (There’s always more.)

Two weeks from now, you’ll owe another $17.50. And another . . . and another—until you pay off the balance. If you’re keeping up with the math here, you’re still paying $70, but it’s broken up into four “easy” payments. Some BNPL services don’t charge interest, but if you miss even one of those payments (oops!), you’ll get hit with a late fee.

For example, if you’re using Afterpay, they’ll slap an $8 fee on the balance you already owe. And every week you don’t pay, they’ll tack on another $8 until the bill is paid (or the fees total up to 25% of the balance).3 Woof.

While late fees are bad, interest is arguably worse. Let’s look at an example from the Flex Pay website (another popular BNPL provider). Say you spend $1,500 on plane tickets to Mexico and choose to finance the trip over a couple years instead of paying for it up front. Looking at the monthly payment alone, $70 a month doesn’t sound too bad.

But if you look in the fine print, you’ll see that some Flex Pay loans come with APRs up to 36%.4 In the example above, even at a relatively low 15% APR, you’d pay back $1,750 over 24 months for a $1,500 trip. Think of all the tacos, burritos and guacamole you could have enjoyed in Mexico with that extra $250 in your pocket. No bueno.

Even if you do make your payments on time, the big problem is that it numbs you to the reality of how much you’re really spending. Instead of making you feel that sticker shock, installment payments are just feeding your “I want it now” mentality . . . and hiding the cost of what you’re buying.

You might be wondering how BNPL companies make money on interest-free loans. Well, they collect a percentage of sales (around 3–5%) from the businesses that use their services. What’s in it for the businesses? They know shoppers will spend way more money if they’re able to buy now and pay later.

Should You Use Buy Now, Pay Later?

When it comes to BNPL, you’re going to want to take a hard pass. Seriously, just say no! These companies promise flexibility and convenience, but that’s exactly what makes them dangerous. By breaking purchases into smaller payments, BNPL can make it easier to spend money you don’t actually have (on things you probably don’t need) and harder to recognize how much you’re really spending.

Pro tip: If it walks like debt, talks like debt, and smells like debt—it’s debt. And these “easy payments” that companies are boasting about aren’t any different. They aren’t a smart way to buy things you want. They aren’t more harmless than a credit card. And they aren’t a fancy way to “budget” for a purchase. They’re just wannabe credit cards dressed in shiny clothes, pretending to be your ticket to having it all.

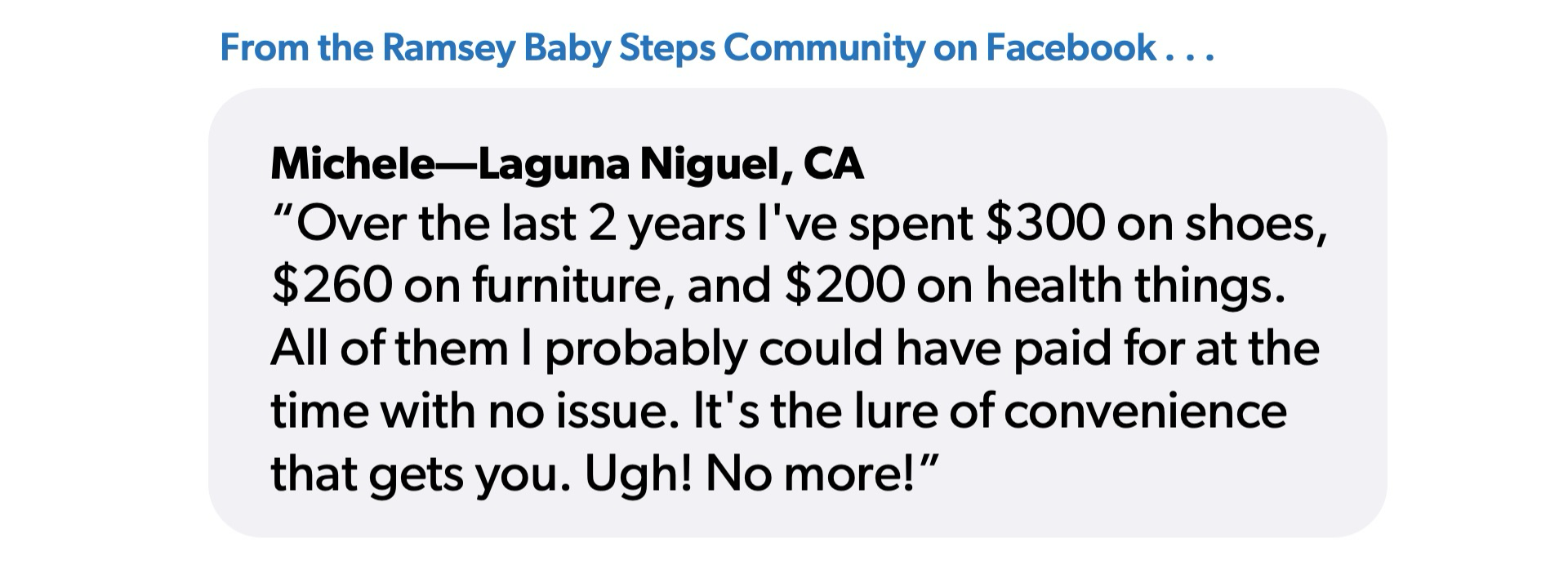

But don’t just take our word for it. After adding up her BNPL purchases, Michelle, a member of our Ramsey Baby Steps Community Facebook group, shared this:

“Over the last two years I’ve spent $300 on shoes, $260 on furniture, and $200 on health things. All of them I probably could have paid for at the time with no issue. It’s the lure of convenience that gets you. Ugh! No more!”

Whatever you do, don’t fall for an installment payment plan—unless you plan to stay broke.

Whatever you do, don’t fall for an installment payment plan—unless you plan to stay broke.

How Buy Now, Pay Later Affects Your Credit

While most buy now, pay later companies run a soft credit check on you, they don’t really do much more than make sure you’re over 18 years old and have a phone number and bank account. That means a lot of people get approved but don’t really understand the potential consequences of BNPL.

This “anyone can use it” idea is a sure way to get a lot of people into trouble—fast. Not only that, more and more shoppers are buying now and forgetting to pay later. And there are consequences for that.

Several years ago, Experian (the major credit reporting bureau) started recording shopper’s digital installment payments from these buy now, pay later companies.5 Yep—if you’re behind on payments, it could hurt your credit score. That makes these companies seem less appealing, doesn’t it?

Credit bureaus are saying this move could help consumers build their credit scores if they use these digital installments the right way. But here’s the truth: Buy now, pay later schemes are just going to dig you deeper into debt (and mess with your credit—but we don’t care about that).

Credit scores only tell you how well you’ve used (and abused) debt throughout your life. In other words, a credit score is basically an “I love debt” score. The higher your score, the more you've proven to lenders that you know how to borrow money and pay it back.

Not only that, they keep you chained to the idea that you need a credit score to survive. That’s a myth! You don’t need a credit score to win with money. But that’s another rant for another day.

Popular Buy Now, Pay Later Apps Compared

If you try to buy anything online these days, you might be greeted by one of these heavy hitters in the world of easy payments:

- Afterpay

- Affirm

- Klarna

- PayPal

- Sezzle

- Zip

- Uplift

- Splitit

Most of these buy now, pay later companies give consumers the option to pay in four installments by making four interest-free payments every two weeks. But some offer shoppers different ways to pay that are even sketchier.

Afterpay

Afterpay’s service allows buyers to split their bill into four equal payments, with the first paid up front and the rest billed every two weeks. Like a credit card company, Afterpay can increase how much you’re allowed to spend over time. The more they trust you to borrow, the more they may let you borrow. Sounds familiar, doesn’t it?

Unlike some BNPL companies, Afterpay doesn’t just stop at online shopping. Through its app and digital wallet features, shoppers can use Afterpay in stores too. Yikes. Some users can even qualify for a "no payment upfront" feature that lets them take home an item before making the first payment. Because apparently paying later wasn’t late enough.

While Afterpay doesn’t charge interest on its standard Pay in 4 plan, missed payments can result in late fees of up to 25%. For orders above $40, the initial late fee is $10 and the total fee is up to 25% of the order value, capped at $68.6

Affirm

Unlike Afterpay, Affirm offers several different ways to pay over time. Customers can choose from a pay-in-four option or longer-term installment loans with monthly payments.

In addition to its buy now, pay later options, Affirm offers an Affirm Card that lets users turn eligible purchases into payment plans. So while many people think of Affirm as a simple BNPL service, it’s increasingly becoming an everyday payment tool.

One thing Affirm loves to point out is that it doesn’t charge late fees. Sounds nice, right? Well, not so fast. Depending on the loan and your credit profile, APRs can reach as high as 36%, and interest begins accruing as soon as the loan is funded.7 In other words, you could end up paying far more than the original purchase price.

Klarna

With its bright pink logo and promise that it “makes shopping smooth,” Klarna is like that adorable baby girl who’s got Mom and Dad wrapped around her finger—or rather, millennials and Gen Z wrapped up in debt.

For the most part, Klarna looks a lot like Afterpay with its popular pay-in-four option. But like Affirm, Klarna also offers other payment plans, including a pay-in-30 option (nothing due until 30 days are up) and financing up to 24 months that comes with interest at an annual rate up to 28.99%. Be warned: If you miss a payment on the financing option, Klarna may charge a late fee of up to $7 or 25% of the outstanding balance (whichever comes first).8

Sezzle

We’ll admit, it’s got a fun name, but that’s the only thing that’s fun about Sezzle. On its website, Sezzle says it “puts you in control of how you pay.” We see it differently. If you have to keep making payments after you’ve already taken the item home, you’re still tied to that purchase. The most control you’ll ever have over your money is when you can pay for something in full with cash.

And don’t assume “pay in four” comes without a cost. In one example on its website, Sezzle shows a $300 purchase costing $307.49 after a $7.49 service fee is added.9 Seven bucks may not sound like much, but it’s a reminder that these companies aren’t doing this out of the kindness of their hearts.

Sezzle also offers paid subscription plans that unlock additional spending features and purchasing options. So now you can pay a monthly subscription fee for the privilege of taking on even more debt!

Zip

Zip promotes the idea that you can “buy now, pay later anywhere.” Anywhere? Yep—Zip is accepted anywhere Visa is accepted . . . which is pretty much everywhere. You can even get a virtual card. That’s great news if your goal is to put every purchase imaginable on a payment plan.

But don’t assume paying later is free. According to Zip’s own disclosures, some purchases come with fees up to $124. In one example on its website, a $400 purchase ends up costing $418.97 after fees are added.10 That’s right—you can pay extra for the privilege of paying later.

Flex Pay by Upgrade

Flex Pay is a buy now, pay later financing option that’s commonly used for travel purchases like flights, hotels, cruises and vacation packages. Instead of paying the full cost up front, travelers can split the purchase into fixed monthly payments.

But convenience comes at a cost. Depending on your credit score and financing offer, Flex Pay loans can carry APRs of up to 36%.11 Dang!

And Flex Pay doesn’t require you to finish paying before you use what you bought. According to the company, you’re free to travel before the balance is paid off. So, while your vacation memories may fade, those monthly payments can stick around for months—or even years. Nothing says “buyer’s remorse” quite like making a payment on a beach trip you can barely remember.

Splitit

Splitit takes BNPL to a whole new level because it’s linked to an existing credit card. It basically lets you split a large credit card purchase into monthly or biweekly payments. The idea here is that if you pay off your credit card bill each month (and we know a lot of people don’t), you won’t have to pay interest on a big purchase.

When you buy something with Splitit, your card is charged for the first payment and preauthorized for the remaining payments. (This means your credit limit is lowered by that amount but not actually charged.) Every month, Splitit will make an additional charge for a payment (and lower the preauthorization amount) until whatever you bought is paid for.

If that sounds complicated, it’s because it is. Paying in cash is a whole lot simpler.

What Can You Use Buy Now, Pay Later For?

Once upon a time, BNPL was mainly used for online shopping. Now, it’s available for just about anything you can think of.

That shiny new $1,000 iPhone? It could be yours now for just four installments of $250!

How about a $2,500 ticket for a two-week Mediterranean cruise? No need to save up—you’ll definitely feel relaxed on the deck knowing you’ve still got a year’s worth of payments long after your tan fades.

Craving a pint of ice cream? Nothing is sweeter than being able to dig in now and pay later when you grocery shop online.

We hope you caught all of our sarcasm there. Unfortunately, we’re not joking. You can buy all of those things with an installment payment plan—and then some. So, the better question might be: What can’t you use buy now, pay later for?

Do Buy Now, Pay Later Plans Make You Spend More Money?

Let’s just say they definitely don’t make you spend less money.

Remember, these companies want you to believe they aren’t out to make money off you. But hey, if people just so happen to spend more when using their service, well, that’s fine with them. And it’s not a secret. These buy now, pay later businesses are actually pretty proud of helping you blow your budget.

Afterpay brags that shoppers who use their services spend 58% more than people who don’t.12 Klarna tells businesses that they can boost the average order price by 40%.13 And not to be shown up by its buddies in the business, Affirm boasts a 70% increase in average order values!14 Is your stomach turning now? Yep, ours too.

The numbers don’t lie—people spend more when they use installment payments like these. And it makes sense. If you get to the checkout online and see you can get $125 worth of items by paying just $31.25 now, then you might go ahead and add a few more items you had your eye on—because why not?

No wonder 54% of American workers are living paycheck to paycheck.15 Thanks, Afterpay.

Don’t be fooled by these guys. They aren’t your friends. They don’t want to swoop in and save the day so you can buy that $250 leather jacket you deserve. They want to make money off you. They’re betting you won’t be able to make a payment, and they’ll get to cash in on it. If they can lure you in and make you comfortable, then they’ve got you right where they want you—with your guard down and cozied up with more debt.

What’s the Best Alternative to Buy Now, Pay Later?

We all want things now rather than later. But the best alternative to using a BNPL installment plan is a save now, buy later plan. Yes, it sounds old fashioned, but saving up to buy something you really want is the way to go.

The hard reality is that we might not have the money to foot the entire bill at the moment (sorry, instant gratification). But using an installment payment plan isn’t the answer.

Want to know what really works? A zero-based budget. When you give every dollar a job, you can see where your money is going, make adjustments when needed, and start setting aside money for future purchases or debt payments.

Sure, saving up for something over time takes willpower. But you can do it! It’s called delayed gratification. And that monthly budget we’re talking about is your key to success.

With a budget, you can save up to buy what you want using cash. And you’ll know for sure if you can even afford it without having to rely on using someone else’s money. So, step away from the buy now, pay later schemes and start using EveryDollar—the free budget tool that empowers you to give, save and spend . . . no digital installment payments necessary.

Next Steps

- Create a budget with EveryDollar to see where your money’s going and make a plan for upcoming purchases.

- Set aside money each month and save up for larger purchases before buying them.

- Skip buy now, pay later plans and pay with cash when it’s time to make the purchase.

-

Is buy now, pay later considered debt?

-

Yes. Buy now, pay later is debt—plain and simple. It’s a short-term loan that lets you take home a purchase today and pay for it over time. The payments may be smaller, but you’re still borrowing money to buy something you can’t pay for right now.

-

Does buy now, pay later hurt your credit score?

-

It can. Some BNPL providers report payment activity to credit bureaus, which means missed or late payments could show up on your credit report and hurt your score.

-

What happens if you miss a buy now, pay later payment?

-

You could face late fees, interest charges, credit score damage, or even collections, depending on the provider. Either way, a missed payment can turn a small purchase into a bigger problem.

-

Does buy now, pay later make you spend more money?

-

Yes. Breaking a purchase into smaller payments makes it easier to spend more than you planned. Retailers love buy now, pay later because it often leads shoppers to buy more.

-

What’s the best alternative to buy now, pay later?

-

Save now, buy later. It may not be flashy, but it works. Create a zero-based budget, give every dollar a job, and set aside money each month for the things you want to buy. When you pay with money you’ve already saved, you don’t have to keep up with payments, worry about late fees, or have debt hanging over your head.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.