The State of Personal Finance in America Q1 2026

5th Anniversary Edition

By

By

Introduction

Five years ago, Ramsey Solutions launched The State of Personal Finance, a research study asking everyday Americans about their money habits and opinions—everything from budgets and bills to debt and investing for the future.

In those five years, a global pandemic sent everyone into isolation. Inflation hit 40-year highs. Controversial elections divided the country. Artificial intelligence began transforming the workforce. Even the demographic makeup of the country has changed, with more baby boomers entering retirement and Gen Zers becoming adults and entering the real world (Gen Z survey respondents were age 18–24 in 2021 and are now 23–29).

But through it all, Americans have kept going, managing their money through these moments of uncertainty—and making real progress.

This special edition of The State of Personal Finance marks this five-year milestone with a comprehensive look at some of the data we’ve been tracking all that time. And it’s a mixed bag: While some Americans are doing better with their money, financial pressure has intensified for others.

Executive Summary

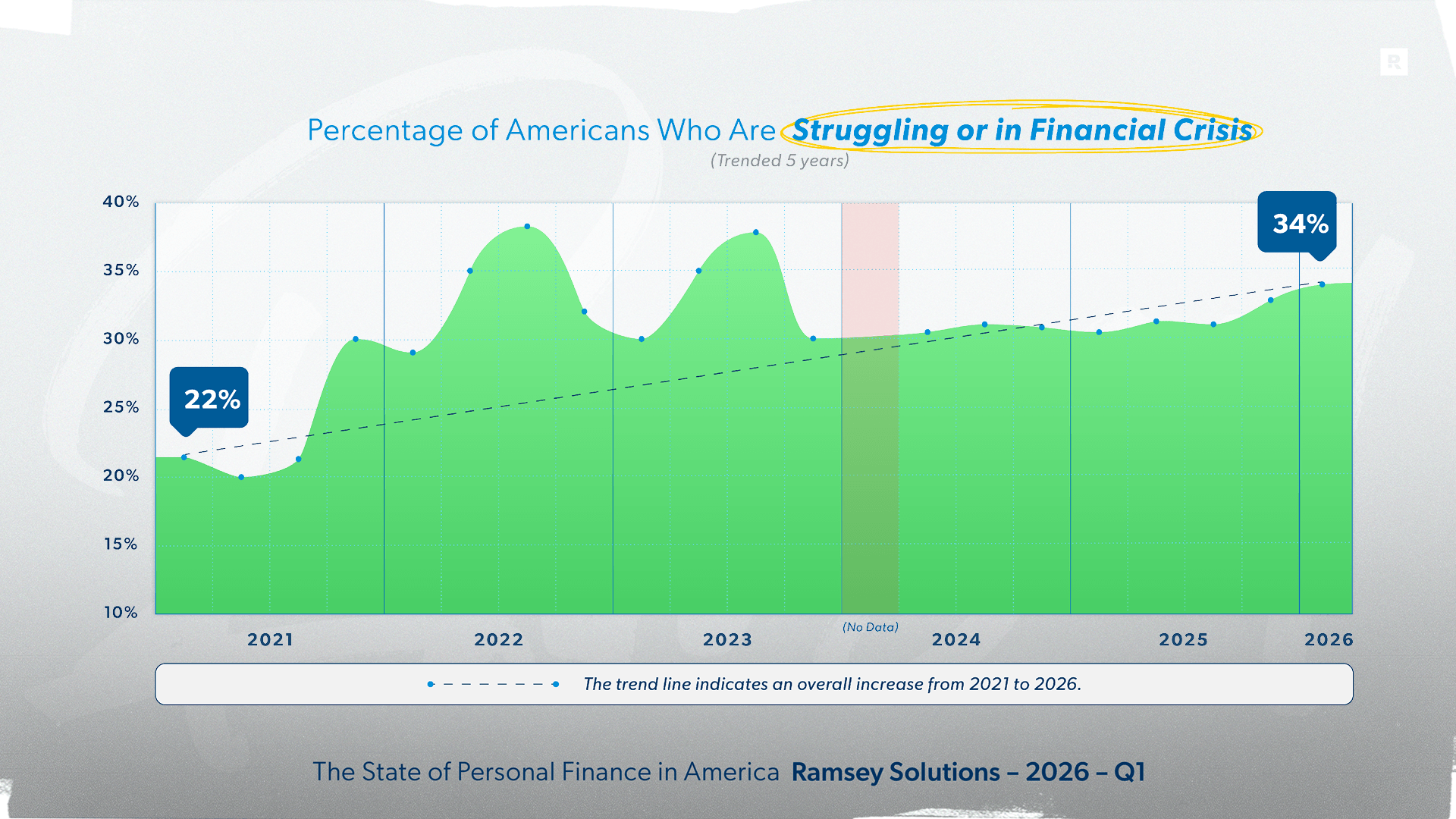

- 34% of Americans (approximately 88 million adults) in 2026 describe their financial situation as “struggling” or “in crisis,” up from 22% in 2021—a 55% increase in five years.

- Difficulty providing the basics of life (housing, bills, food) has increased in the last five years—though homeowners have had the least difficulty.

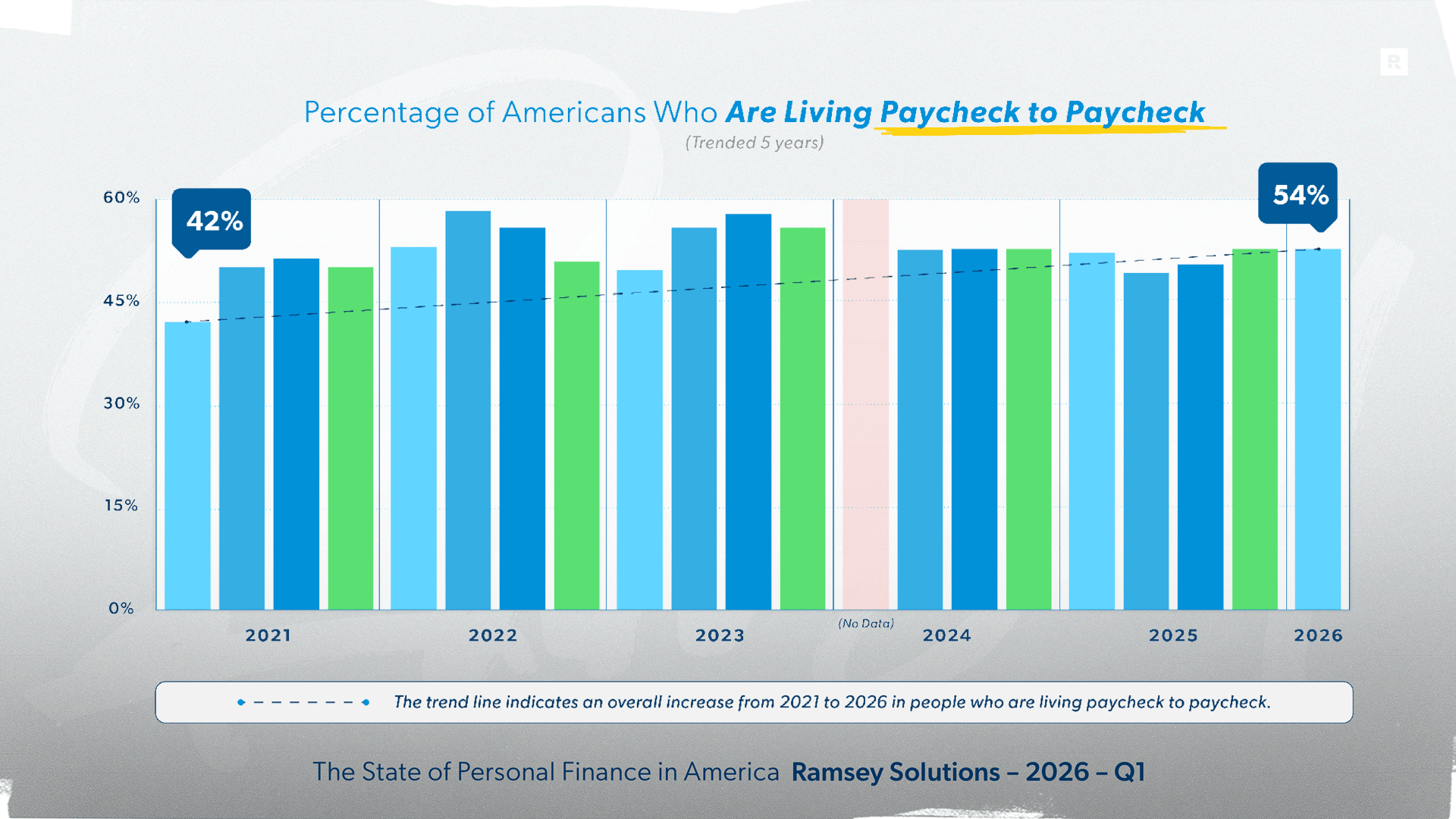

- In 2021, 42% of Americans said they were living paycheck to paycheck. Today, that number is up to 54%.

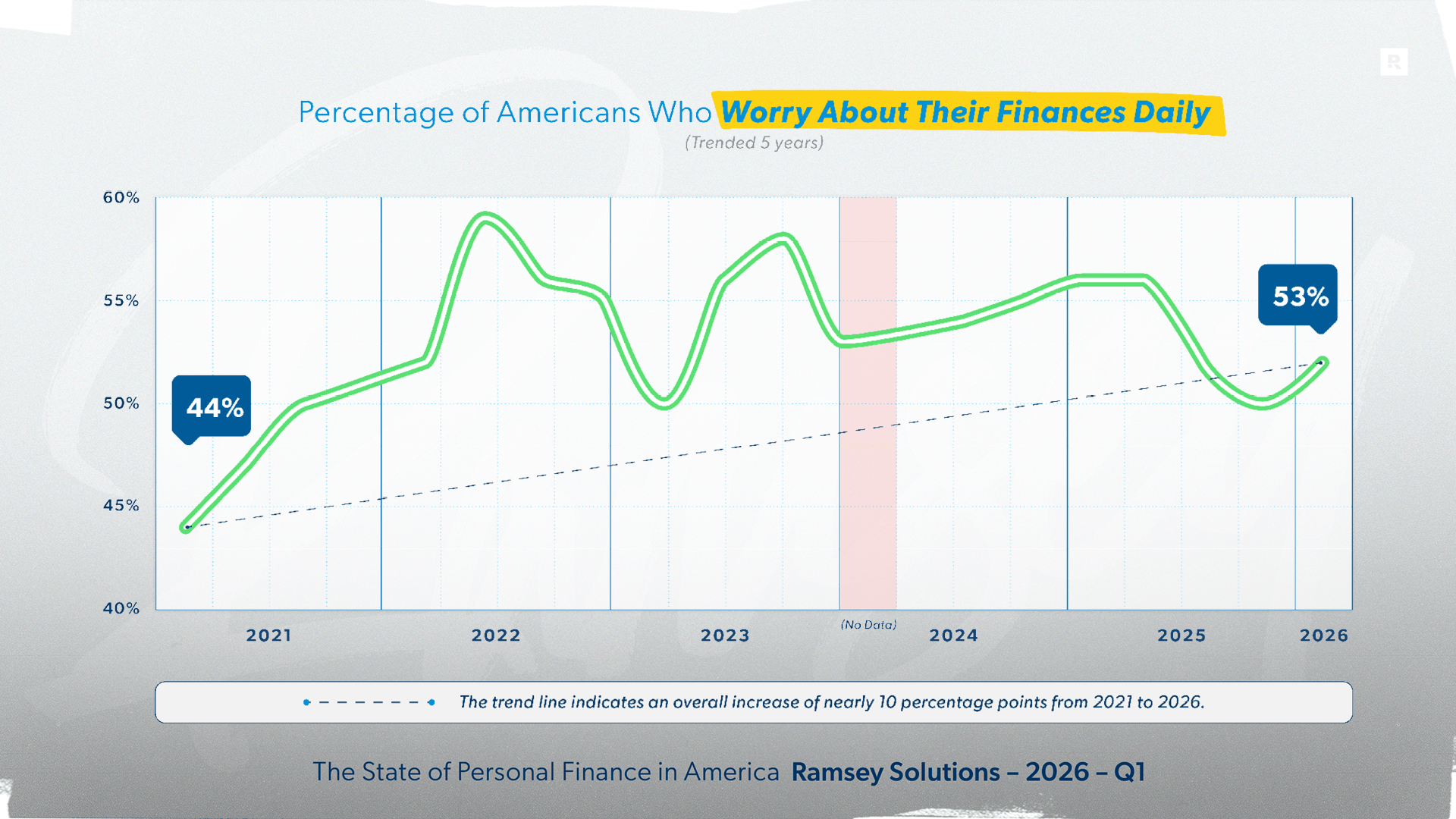

- Five years ago, 44% of Americans said they worried about money every single day, and that figure has climbed to 53% in 2026.

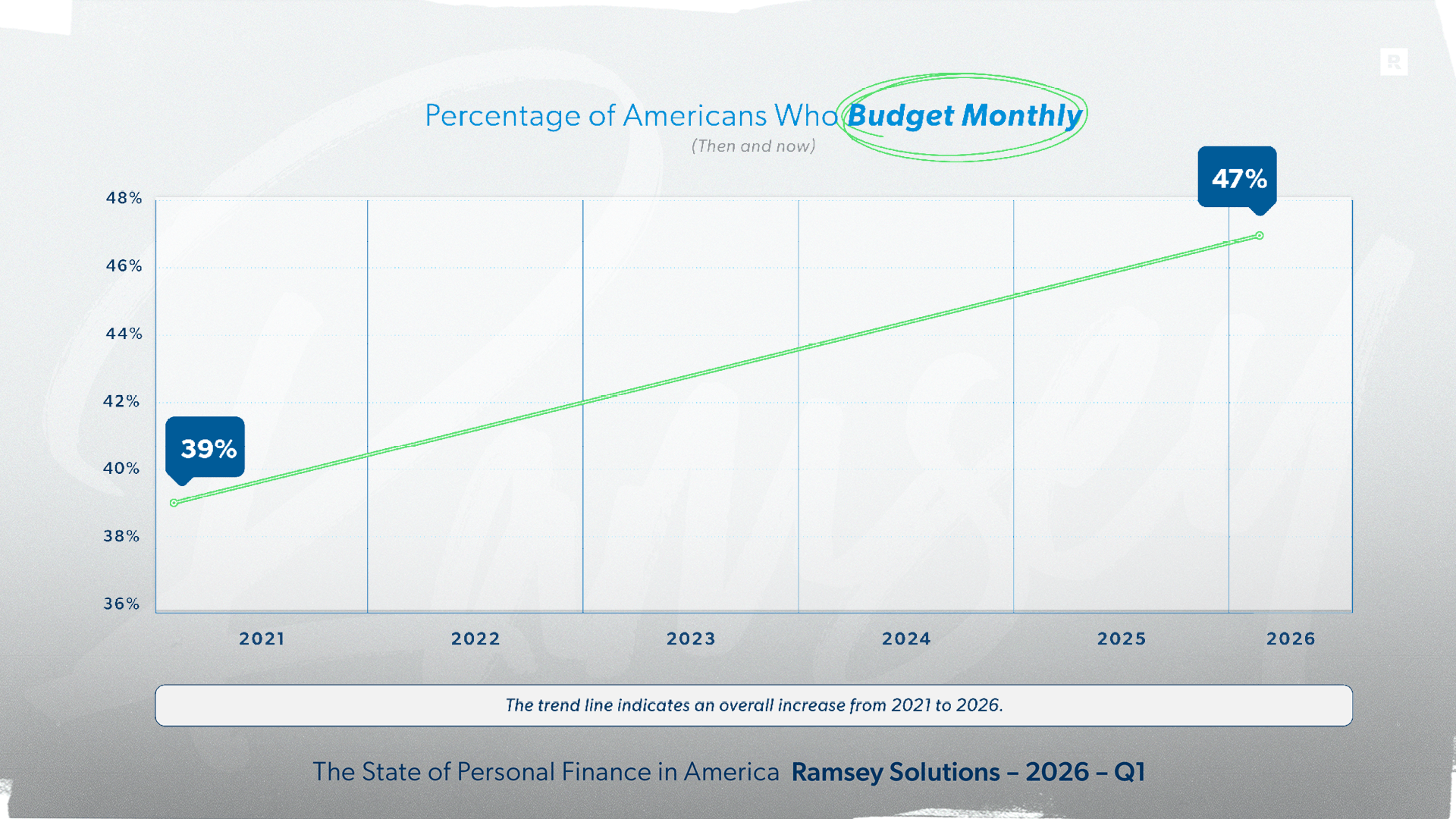

- The number of Americans who say they follow a monthly budget has grown from 47% in 2021 to 53% in 2026. The biggest gains are from Gen Z and middle-income households.

- Debit card usage among U.S. adults has increased from 35% in 2021 to 41% in 2026, while reliance on credit cards has edged down from 42% to 39%.

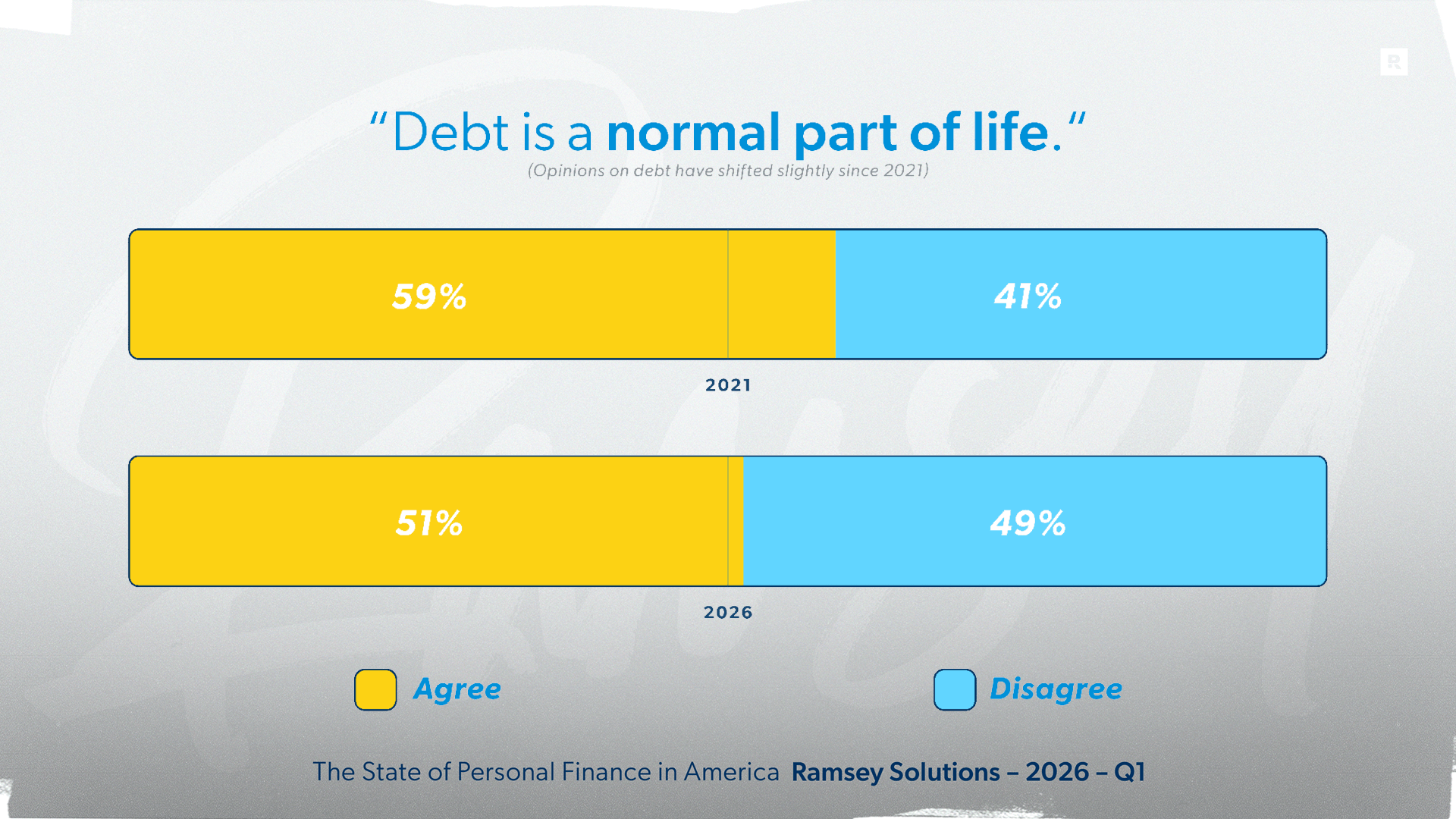

- Back in 2021, 59% of Americans agreed with the statement that “debt is a normal part of life.” In 2026, that number is 51%.

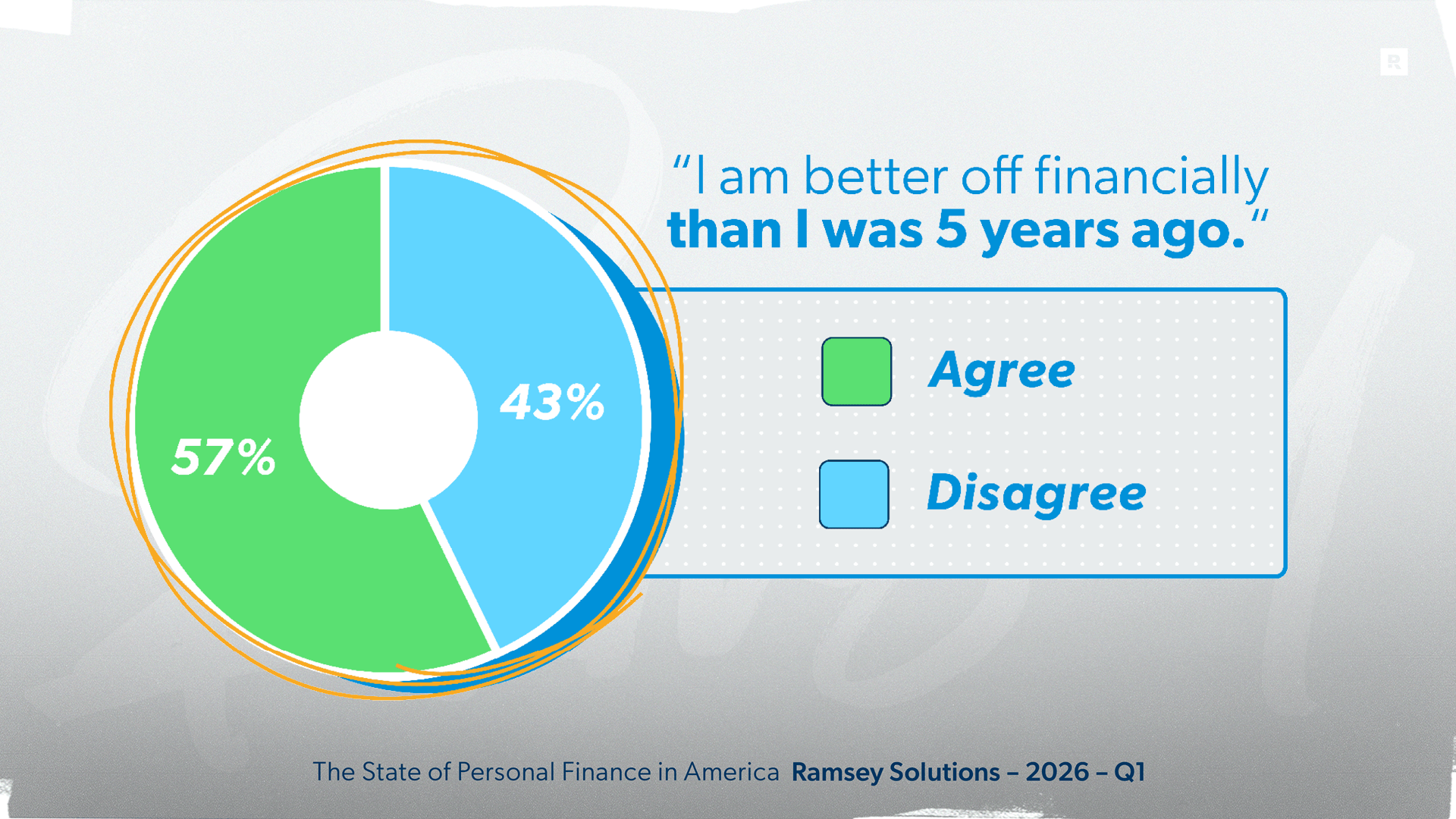

- Though only a quarter of Americans (26%) say they’re better off financially today than they were a year ago, a sizeable majority (60%) say they are better off today than they were five years ago.

- About half of U.S. adults (51%) experienced an unexpected money emergency in the last five years—and rates were substantially higher among those with debt and children.

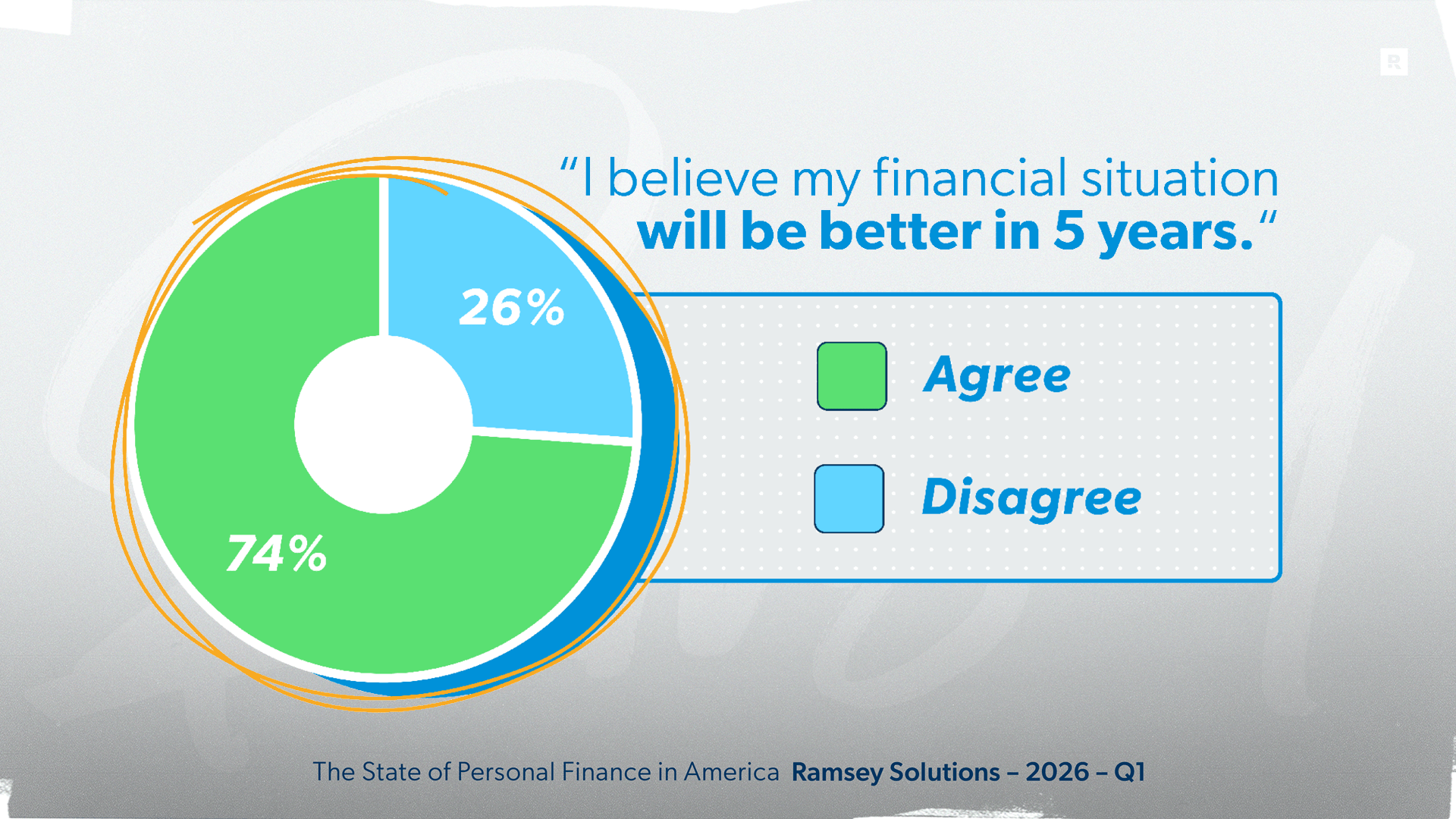

- Looking to the future, three-quarters of U.S. adults (74%) believe they will be better off financially five years from now.

Download a PDF version of this report.

Download a full electronic press kit (EPK)

of the report, including full-size graphics.

How Have Americans’ Finances Changed in 5 Years?

Five years ago, the world was still in the thick of the pandemic. Millions were out of work or underemployed. And government stimulus checks were temporarily propping up many family budgets.

You might think that compared to 2021, fewer people would be struggling in 2026. However, 34% of Americans (approximately 88 million adults) describe their financial situation as “struggling” or “in crisis” in 2026, up from 22% in 2021. That’s a 55% increase in five years. Nearly every demographic has felt the jump, but the biggest increases have been among women (26% in 2021 to 42% in 2026), Gen X (27% to 41%), lower-income households (39% to 53%) and people with debt (28% to 43%).

For married Americans, the “struggling” or “in crisis” rate has barely moved—sitting at 22% in 2021 and 21% in 2026. But for singles, it’s a different story: The rate jumped from 30% in 2021 to 45% in 2026.

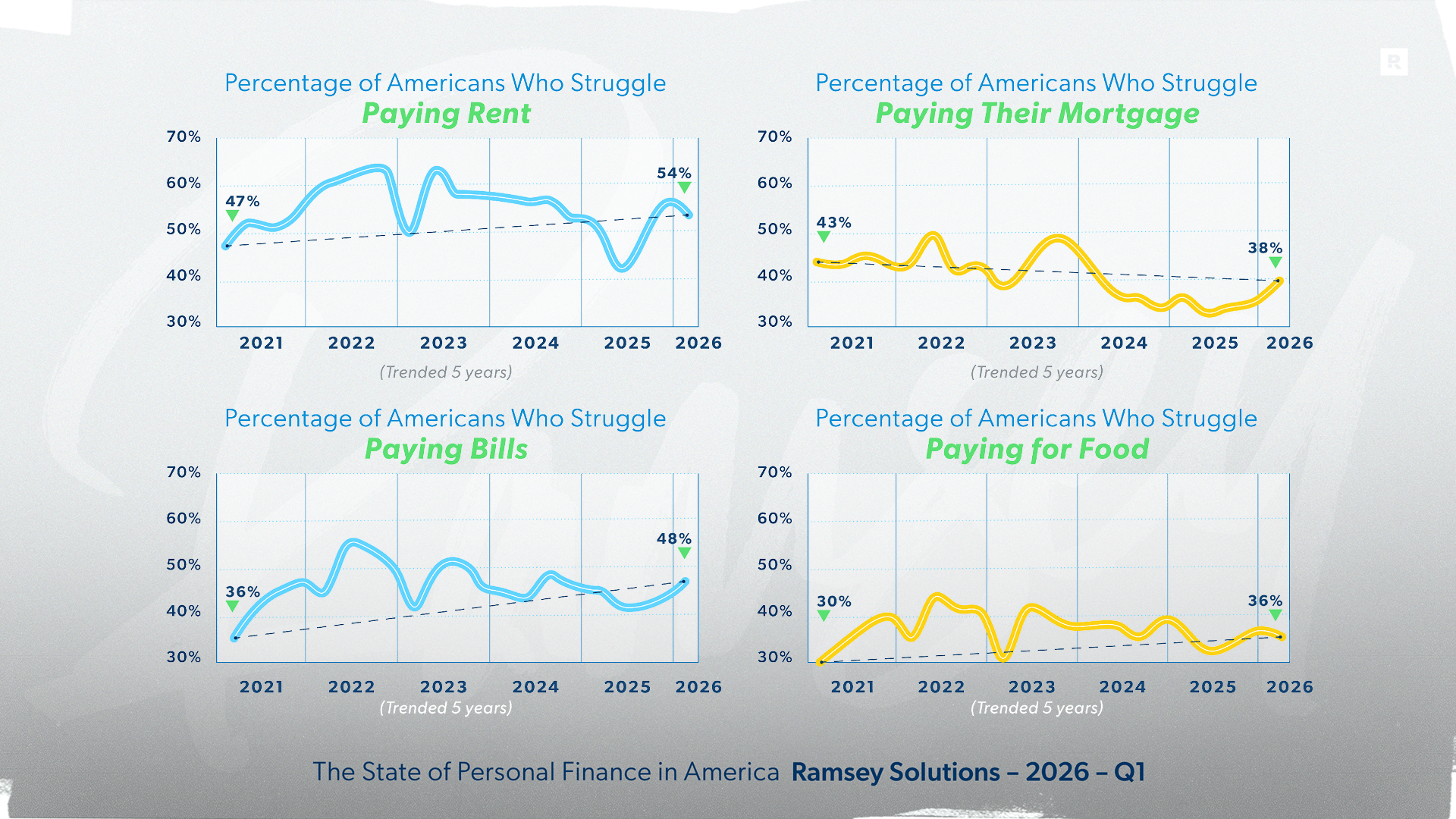

Whether you’re single or married, when money is tight, it’s smart to protect your Four Walls first: food, utilities, shelter and transportation. But over the last five years, more people have had a hard time covering some of these life basics.

Today, 54% of renters say they struggle with making rent every month—an improvement from the 64% peak during the inflation surge of 2022 but still worse than where renters stood in 2021 (47%). Homeowners have been somewhat more stable overall, with the number of people struggling to make their mortgage payments down from 43% in 2021 to 38% in 2026.

Bills have become an even bigger pressure point. The share of Americans who have difficulty paying their monthly expenses has climbed from a third (36%) in 2021 to almost half (48%) in 2026—a 33% increase in five years. That challenge has been hardest on women (38% in 2021 vs. 54% in 2026), Gen X (33% vs. 52%), lower-income households (50% vs. 64%) and those with consumer debt (46% vs. 62%).

Food costs tell a similar story. The inflation spike of 2022 sent food prices soaring. And while inflation has stabilized, people are still feeling the strain of higher food prices. Today, 36% of Americans say providing food is a challenge, up from 30% in 2021.

The struggle to pay for basics is often the result of living paycheck to paycheck, where money disappears as soon as it’s earned with virtually nothing left over. And many more Americans are caught in this dangerous cycle.

In 2021, 42% of Americans said they were living paycheck to paycheck. Today, that number is 54%—meaning half the country is one missed paycheck or unexpected expense away from serious financial trouble. The rate is especially high among lower-income households (74%), singles (64%) and Americans with consumer debt (65%). Younger generations are also feeling this pressure: 63% of millennials and 61% of Gen Z say they live paycheck to paycheck.

When you aren’t able to save money because your whole paycheck is going toward bills, you can’t create a buffer to cover unexpected expenses. And the unexpected always comes—whether it’s a car repair, a medical bill or a broken appliance. When there’s no cushion, a small money emergency can quickly become a full-blown crisis.

About half of U.S. adults (51%) experienced an unexpected money emergency in the last five years. Rates were substantially higher for people who have debt (64%) and families with children (63%), possibly because what qualifies as an “emergency” often depends on your situation. Someone in debt, for example, could see a

$1,000 car repair as a catastrophic emergency that will drive them deeper down the hole instead of just a minor inconvenience. This is why having an emergency fund is crucial to financial peace, no matter your income level.

The growing difficulty to cover basic expenses combined with the insecurity of living paycheck to paycheck have naturally increased Americans’ money stress.

Five years ago, 44% of Americans said they worried about money every single day. Today, that figure has climbed to 53%—about half the country. The increase has been sharpest among Gen X (46% in 2021 vs. 58% in 2026), lower-income households (52% vs. 66%) and people with debt (54% vs. 63%).

Sleep loss tied to money worries peaked in 2022 and has edged back since then, but it remains elevated: 39% of Americans today report losing sleep because of financial concerns, compared to 35% in 2021.

All these financial stresses (both internal and external) are affecting Americans’ short-term financial outlook, and more people are adopting a troublesome little-guy-can’t-get-ahead attitude. Just over half of Americans (54%) now say they can’t get ahead financially, a significant shift from where that number stood five years ago (44%).

In addition, the number of Americans who say they’re better off now than last year has fallen from 30% to 26%.

Money Behaviors and Beliefs Have Shifted Positively Since 2021

Even though Americans are feeling financial stress and pressure, there is a silver lining: Many Americans are making better choices with their money. These gains have been gradual, but they’re a step in the right direction. And several findings might suggest that younger Americans are taking sound money advice to heart more than their parents and grandparents.

One of the most encouraging pieces of data is that the number of people who use a budget—the foundation of a good financial plan—has increased. In 2021, 39% of Americans said they created a monthly budget. That number has grown to 47% in 2026. And the biggest gains come from Gen Z (38% vs. 53%) and middle-income households (37% vs. 49%).

How Americans pay for everyday purchases over the last five years has also seen positive change. Debit card usage has increased from 35% in 2021 to 41% in 2026, while reliance on credit cards has edged down from 42% to 39%—with Gen Z showing the sharpest decline (27% to 20%).

But credit cards are still causing problems. The share of Americans who have maxed out a credit card has ticked up slightly, from 19% in 2021 to 23% in 2026. However, the number of Americans signing up for a new credit card in the last three months is about the same (19% vs. 17%).

Americans’ relationship with debt itself is a problem that has only compounded in the last five years (total household debt in the U.S. is now at $18.8 trillion!). When people believe debt is normal and simply a part of life, they’re hardly motivated to fight it. But when they see debt as the huge problem that it is, they’re more likely to make the sacrifices necessary to get free of it.

Feelings toward debt may be shifting, but it’s been a slow shift. In 2021, 59% of Americans agreed with the statement that “debt is a normal part of life.” In 2026, that number has dropped to 51%. And the biggest downward shifts have come from millennials (71% to 49%) and men (64% to 55%).

Surprisingly, older generations are turning to credit cards more frequently, while younger generations are pulling back. Both baby boomers and Gen X had upticks in maxing out cards and signing up for new ones. Yet three times as many Gen Zers than baby boomers are still maxing out cards (10% vs. 30%).

While Americans have gotten wiser in some areas, there have been setbacks—including things as crucial as retirement savings. The share of Americans who are actively investing for retirement has declined over the last five years, from 51% to 42%.

One explanation for the decline is that as baby boomers (a large segment of the population) retire, they stop investing and start living on the retirement savings they’ve built. However, the decline could also, in part, be a result of people cutting out retirement investing as they’ve felt more pressure on their budgets—a much less encouraging trend.

Even though the number of Americans investing in their retirement has declined, the desire to retire early has grown significantly over the last five years—from 48% to 59%—with especially large increases among men (50% to 62%).

The desire to retire early may be driving a more positive trend: More Americans are seeking professional financial guidance. A good financial advisor can help people make smarter long-term decisions, even during difficult seasons. The share of Americans who work with a financial advisor or other financial professional has made a 10-point jump from 35% to 45% over the last five years.

Americans Look Forward With Perspective

The last five years have had their financial ups and downs—but not without genuine progress. And despite the real challenges they face today, Americans remain remarkably optimistic about what lies ahead.

While only a quarter of Americans say they’re better off financially today than they were a year ago, a sizeable majority (57%) say they are better off today than they were five years ago. Men (66%) and higher-income households (76%) are most likely to report improvement, but the majority across most demographics agree that

their financial situation has improved over the past five years.

Along the same lines, 59% of Americans say their net worth has increased over the last five years, with higher-income households (82%) the most likely to report growth. For all the pressure Americans are feeling in their day-to-day finances, many have built real wealth over this period.

Americans are incredibly optimistic about where they will be in the future. Three-quarters of U.S. adults (74%) believe they’ll be better off financially five years from now. That’s a striking number when set against the backdrop of so many Americans feeling squeezed today. It suggests that while the day-to-day feels hard, most Americans are hopeful about where they’re headed.

Statistically, hope has returned to where it was when this study launched, even though the financial circumstances are harder in many ways. In 2021, 38% of Americans described themselves as hopeful about their financial future. That number dropped sharply in 2022 as inflation ramped up. But since 2022, hope has been steadily recovering, gaining 13 points over the last three years. Today, 39% of Americans describe themselves as financially hopeful. And all demographics are pretty much within that range.

The fact that Americans still believe in the possibility of financial peace is a positive sign. While many people will have to change the way they handle money to make their vision of a better financial future a reality, those who believe their situation can improve are more likely to take the actions that lead to progress.

Conclusion

When The State of Personal Finance launched in January 2021, the country was managing a series of crises. Today, Americans are carrying more financial stress, living paycheck to paycheck at higher rates, and struggling to shake the feeling that getting ahead is out of reach.

But the story isn’t all doom and gloom. Net worth is up. The number of Americans who budget is up. Americans are growing less dependent on credit cards, and fewer believe that debt is a normal part of life. Most Americans—6 in 10—say they’re actually better off than they were five years ago. Things feel harder, but many key indicators point to progress.

That gap between feelings and reality is exactly where financial behavior matters most. Because winning with money is 80% behavior and 20% head knowledge. The outside forces—inflation, interest rates, politics, global instability—are real. But they are not the final word on your financial future. You are.

So, get on a budget. Attack your debt. Build an emergency fund so the next crisis doesn’t knock you down. And invest in your future. The five-year data shows that Americans who have made those choices are better off—and that’s not a coincidence. It’s the result of intentional behavior over time.

The next five years will no doubt bring their own surprises, challenges and opportunities. The people who come out ahead will be the ones who commit to a plan and stick to it—no matter what the headlines say.

About the Study

The State of Personal Finance is a quarterly research study conducted by Ramsey Solutions to gain an understanding of the personal finance behaviors and attitudes of everyday Americans. The nationally representative sample of 1,095 U.S. adults was fielded from March 3–13, 2026, using a third-party research panel. Margin of error was ±3.08%.

Since January of 2021, The State of Personal Finance has surveyed over 20,000 U.S. adults. Data from the study has been shared on over 1,000 media outlets, including Forbes, Fox News Channel, The New York Times and Good Morning America.

Previous Reports

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.