How to Build Wealth in Your 40s

By

By

Key Takeaways

- Your 40s are likely your highest-earning years. Don’t let them go to waste. Save for retirement now and feel good about your future.

- Baby Steps 4, 5 and 6 are your road map to building wealth: Invest 15% of your income, save for your children’s college fund, and pay off your mortgage.

- The median Gen X retirement savings is $107,000, which is far below what you’ll need.1 But there’s still time to change that.

- Consistently investing in good growth stock mutual funds inside a Roth IRA and 401(k) is a proven path that works.

The median Gen X worker has saved around $107,000 across all their retirement accounts.2 If that number made your stomach drop a little, good. That means you’re paying attention. Because $107,000—while enough to live off for maybe a year or two—isn’t going to fund a 20- or 30-year retirement.

But take a breath! This isn’t the time to throw in the towel. Your 40s can be a game-changing decade for building wealth. Your income is likely higher than it’s ever been, and you still have time on your side. Maybe not as much time as you’d like, but enough to make a real difference if you get your tail in gear now.

Here's A Tip

To build wealth in your 40s, invest 15% of your income in good growth stock mutual funds in a Roth IRA and 401(k). Start saving for your kids’ college, make extra mortgage payments, and protect your income with term life insurance. Follow the Baby Steps in order. They’re Ramsey’s proven plan for financial peace. The decisions you make in your 40s will define the decades that follow.

Why Are Your 40s So Important for Building Wealth?

Like we said, your 40s can be your best decade for building wealth because you’re most likely earning more than you ever have. The median weekly income for full-time employees ages 45–54 is $1,435.3 Your income is your most powerful wealth-building tool, and you still have 20-plus years to invest a chunk of it to grow your nest egg.

Think about what’s probably true right now: Your salary has grown. The kids are older (or getting there). The potential for lifestyle creep is real. But so is the opportunity. People who have $107,000 in retirement savings are doing what’s normal. Their income is going toward debt payments, vacations, renovations and car upgrades. So be weird and use your income to build a nest egg that will allow you to retire with dignity.

And look, you can’t rely on the government to take care of your retirement expenses. Social Security was never meant to be your only retirement plan. The average monthly benefit is only a little over $1,900 (barely enough to cover rent in most cities).4 So if you’re counting on Uncle Sam to fund your golden years, it’s time for a reality check.

But you’re not starting from zero. You have income, experience and the ability to make bigger financial moves than you could in your 20s or 30s. You have the chance now to shift your wealth-building into high gear. Let’s do this.

For more on the principles that work at every stage of life, see our complete guide on how to build wealth.

What Baby Steps Should You Be On in Your 40s?

In your 40s, you’ll ideally be working Baby Steps 4, 5 and 6. That means investing for retirement, saving for your kids’ college, and paying off your house. But life doesn’t always follow a tidy schedule. Let’s pinpoint where you are:

- Still carrying debt (other than a mortgage)? You’re on Baby Step 2. Attack that debt with everything you have using the debt snowball—smallest balance first. Every month you carry debt is a month you’re not building wealth.

- Debt-free but your emergency fund isn’t fully funded? That’s Baby Step 3. Build 3–6 months of expenses in savings before you move on.

- Debt-free with a fully funded emergency fund? You’re ready for Baby Steps 4, 5 and 6. And this is where things get exciting.

|

Baby Step |

Goal |

Key Action in Your 40s |

|

Baby Step 4 |

Invest 15% of your household income for retirement. |

Put money in your 401(k) up to your company match and then max out a Roth IRA. If you need to, invest more in your 401(k) to reach 15%. |

|

Baby Step 5 |

Save for your kids’ college fund. |

Open an ESA or 529. Don’t sacrifice retirement to fund college. |

|

Baby Step 6 |

Pay off your home early. |

Make extra payments so you can have a mortgage-free retirement. |

Baby Step 4: Invest 15% of your household income for retirement.

This is the engine of your wealth-building plan. Invest 15% of your gross household income in good growth stock mutual funds spread across four categories: growth, growth and income, aggressive growth, and international. Use tax-advantaged accounts by contributing to your 401(k) up to the employer match, then maxing out a Roth IRA. If you still need to reach your 15% goal, increase your 401(k) contributions.

Automation is the key to staying consistent with your investing. Set up your retirement accounts so money is automatically invested before you have a chance to spend it. Pretty soon, you won’t even miss it.

Baby Step 5: Save for your kids’ college fund.

Once you’re investing 15% for retirement, it’s time to start saving for college. An Education Savings Account (ESA) or a 529 plan are your two best tools.

Parents, listen up: While it’s great to help your kids go to college, don’t sacrifice your retirement to fund their education. They’ll have other options to cover college costs, like scholarships, grants and part-time work. To have the savings you need to retire with dignity, Baby Step 4 has to come first!

Baby Step 6: Pay off your home early.

Any extra dollar beyond your retirement investing and college savings should go toward your mortgage. The goal is simple: a mortgage-free retirement. Seriously, imagine not stressing over a house payment ever again. We’ll dig into this more below, but even small extra payments can mean you’re debt-free years sooner.

How Much Should You Have Saved for Retirement in Your 40s?

We recommend having a big enough nest egg to withdraw 7–8% a year. Your retirement savings goal depends on how much income you’ll need in retirement.

For a lot of people, that means you need to have roughly three times your annual salary saved by age 40, building toward four to six times your income by 50. By the time you retire, you’ll need roughly 10 times your annual income.

Here’s how that math usually shakes out:

- Let’s say you’re 40 years old and earning about $70,000 a year—a little over the national average.5 If you’re aiming for the high end of the common retirement benchmark, you’d want to have about $210,000 saved for retirement.

- Now let’s say that by age 50, you’ve built your career and are earning $100,000 a year. Using the high end of the age-50 benchmark, your retirement savings goal would be about $600,000.

|

Age |

Annual Income |

Recommended Benchmarks |

Retirement Savings Target |

|

40 |

$70,000 |

3x salary |

$210,000 |

|

50 |

$100,000 |

6x salary |

$600,000 |

Okay, we get it. Those are some big numbers to aim for. But if you’re behind on those goals, you’re not alone. And beating yourself up about it won’t add a single dollar to your retirement account.

You know what will? Increasing your income and directing every available dollar toward your current Baby Step. If you’re on Baby Step 2, that means attacking debt relentlessly. If you’re on Baby Steps 4, 5 and 6, that means building wealth through retirement investing, saving for your kids’ college, and paying off your home.

Sell some stuff. Pick up extra work. Cancel those subscriptions you forgot you were paying for (you know the ones). Don’t overthink it. Start where you are and do what you can. That’s how you keep moving forward.

Here's A Tip

If you’re behind on retirement savings, your single most powerful tool is your income. A raise, a side hustle, or cutting lifestyle expenses you won’t miss can free up hundreds of dollars a month that you can put toward investing.

How Do You Invest in Your 40s?

Investing during your 40s means consistently putting 15% of your gross household income to work through tax-advantaged retirement accounts invested in good growth stock mutual funds.

Here’s the order of operations:

- Contribute to your 401(k) up to the employer match. That’s free money! Don’t leave it on the table.

- Max out your Roth IRA. In 2026, each person can contribute up to $7,500. If you’re 50 or older, that limit increases to $8,600.6 The IRS calls this a catch-up contribution, and it gives you an extra opportunity to boost your savings as you near retirement. If your company offers a Roth 401(k) with good investment choices, you might be able to invest your entire 15% in one account.

- If you haven’t reached 15% yet, increase your contributions to your 401(k) until you do.

Inside those accounts, invest in growth stock mutual funds (with good track records) diversified across four categories: growth, growth and income, aggressive growth, and international. Don’t invest retirement money in single stocks, cryptocurrency or anything else being billed as the “next big thing.”

Should I use a Roth IRA or 401(k) in my 40s?

Both! Seriously. Start with your 401(k) up to the employer match, then max out a Roth IRA. If you still need to reach your 15% goal, increase your 401(k) contributions. The Roth IRA is especially powerful in your 40s because any money you invest now grows tax-free for potentially 20 or more years. That’s a significant advantage.

One more thing: Don’t touch your 401(k) or Roth IRA! That means no loans or early withdrawals. Borrowing from your retirement accounts is a wealth killer. You lose the compound growth on that money. You’ll likely pay taxes and penalties. And if you leave your job with an outstanding 401(k) loan balance, you’ll need to repay it shortly after or the remaining balance becomes a taxable distribution.

In short: Leave your retirement accounts alone and let them grow.

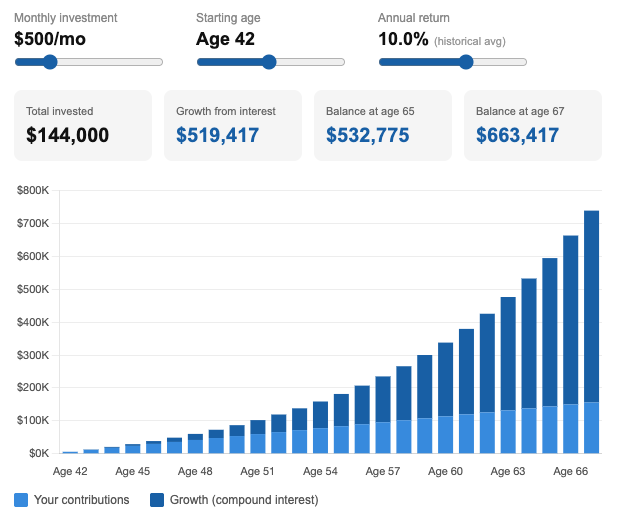

Chart assumes a 10% average annual return—a conservative estimate based on the historical average of the S&P 500 being 10% to 12%. Investments shown in pre-tax growth stock mutual funds inside a Roth IRA or 401(k). Past performance does not guarantee future results.

Should You Pay Off Your House Early in Your 40s?

You don’t want to have a mortgage payment when you retire, so now’s the time to make extra mortgage payments.

The math is pretty compelling. If you have a $250,000 balance on a 15-year fixed-rate mortgage at 4% interest and you pay an extra $400 each month, you’ll pay off your home three years and four months early and save about $20,000 in interest. That’s not a theoretical number. You can run your own numbers with the Ramsey Mortgage Payoff Calculator.

Here's A Tip

Even $100–200 in extra mortgage payments per month adds up over time. Run your own numbers with the Ramsey Mortgage Payoff Calculator. Most people are surprised by how much a small extra payment can shorten their payoff timeline.

If you have a 30-year mortgage, think about refinancing to a 15-year fixed-rate mortgage if the numbers make sense.

A shorter term with a lower rate puts you on the fast track to owning your home outright, which means you can use the money you were paying on your mortgage to invest more for retirement.

What Insurance Do You Need in Your 40s?

Building wealth in your 40s means protecting it too. Insurance doesn’t grow your money, but one bad event without the right coverage can erase everything you’ve built.

Here’s what you need locked in:

- Term life insurance: If people depend on your income, get enough coverage to replace 10–12 times your annual income. Term life is the only kind of life insurance Ramsey recommends. Whole life is a rip-off!

- Disability insurance: Long-term disability insurance protects your income if you can’t work. Many employers offer disability insurance as a benefit.

- Long-term care insurance: You don’t need to obsess over this yet, but it’s worth putting on your radar as you approach 60.

You’ll need to review your life and disability coverage as your financial situation changes. Don’t guess on coverage. Connect with a RamseyTrusted® insurance pro to make sure you’re protected so nothing derails the wealth you’re building.

What If You’re Starting From Scratch in Your 40s?

If you haven’t started saving for retirement, it’s not too late! Maybe you’re just now getting out of debt or never had a real budget. Maybe you’re 44 and just have a few thousand dollars saved. You’re behind, but you’re not out of the game.

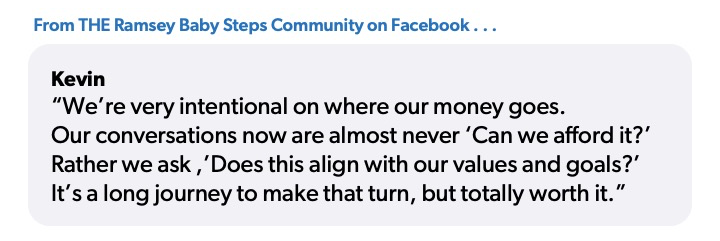

Kevin N. shared his story in THE Ramsey Baby Steps Community Facebook group to encourage people in that exact situation. He went through a divorce at age 42 and buckled down to work the Baby Steps about a year later. “I’ve since remarried, and we are likely within several months of millionaire status,” Kevin said. “We’re very intentional on where our money goes. Our conversations now are almost never ‘Can we afford it?’ Rather, we ask, ‘Does this align with our values and goals?’ It’s a long journey to make that turn, but totally worth it.”

Kevin is right. Getting serious about saving in your 40s is a challenge. But the worst thing you can do is continue putting it off. So, yeah, the best time to get started was years ago. You know what the second-best time is? Right now! Here’s what matters today:

- Increase your income. A second job, a promotion, freelance work, selling things you don’t need. More money coming in means more money to put toward the Baby Steps.

- Cut back on spending. This isn’t forever. This isn’t a punishment. But for right now, get gazelle intense. The people who turn their finances around in their 40s and 50s are the ones who stop pretending the problem will fix itself.

- Stay invested. If you’re starting to invest in your mid-40s, you still have 20 years of compound growth ahead of you. Time is one of your greatest investing advantages—and you still have plenty on your side.

- Work the plan. The Baby Steps are a proven system that’s helped millions of people get back on track, even when they felt way behind. Follow them in order, one step at a time. They work because people do the plan, not just know the plan.

Here's A Tip

“Your most powerful wealth-building tool is your income.” — Dave Ramsey

How Can a Financial Advisor Help You Build Wealth in Your 40s?

By the time you’re in your 40s, your financial life has gotten more complex. You might have a 401(k) from a previous employer sitting around doing nothing. You might have a mortgage, college costs on the horizon, and no clear picture of how it all adds up to retirement.

Working with a good financial advisor can help you see the whole picture and build a coordinated plan so none of your goals fall through the cracks.

They should have the heart of a teacher and can sit you down and help you build a plan that works for your life—without talking down to you. So if you’ve been winging it on your own, this is your sign to get a pro in your corner.

Next Steps

- Find out which Baby Step you’re on.

- If you’re on Baby Step 4, connect with a SmartVestor Pro to build a retirement plan designed for your specific situation.

- See how long it’ll take you to completely own your house with the Ramsey Mortgage Payoff Calculator.

- Start budgeting with EveryDollar so you know exactly how much you can put toward investing each month.

This article provides general guidelines about investing topics. Your situation may be unique. To discuss a plan for your situation, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

-

Is it too late to build wealth in my 40s?

-

No. Your 40s can be one of the best decades to build wealth. Your income is likely higher than it’s ever been, and you still have 20-plus years for compound growth to work in your favor. The key is to stop waiting and start with the Baby Steps now.

-

How much should I be investing in my 40s?

-

Once you’re debt-free and have a fully funded emergency fund, invest 15% of your gross household income for retirement. That’s Baby Step 4. Use your employer’s 401(k) and a Roth IRA to invest in growth stock mutual funds diversified across four types: growth, growth and income, aggressive growth, and international.

-

Should I pay off debt or invest in my 40s?

-

Follow the Baby Steps in order. If you still have non-mortgage debt, pay it off first (Baby Step 2). Once you’re debt-free with a fully funded emergency fund, then invest. Don’t invest while you’re in debt.

-

What’s the best retirement account for me in my 40s?

-

A Roth IRA is one of the most powerful tools in your 40s because your money grows tax-free. Combine it with your employer’s 401(k) to reach your 15% investing goal. If you’re 50 or older, take advantage of catch-up contribution limits to accelerate your savings.

-

How do I catch up on retirement savings in my 40s?

-

Increase your income, cut your lifestyle expenses, and direct every extra dollar toward Baby Steps 4, 5 and 6. Use catch-up contributions once you’re 50. Don’t try to time the market. Just continue to invest consistently.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.