How to Roll Over Your 401(k) to an IRA

7 MIN READ | MAR 9, 2026

By

By

Key Takeaways

- A 401(k) rollover moves your retirement funds from one account type to another, usually after you change jobs or go through a major life change.

- If you want to roll over your 401(k) to an IRA, first choose which IRA you want to transfer the funds to (or open a new account), request a direct transfer rollover, and then choose your investments.

- Once the rollover is done, you’ll have more control, more options, and less work to stay on top of everything.

- Talk with a financial pro about how to make your 401(k) rollover process easier.

Starting a new job can be overwhelming—with meetings, training, and all those new names and faces you’re supposed to remember (wait, that guy you just met. . . was that Bob or Todd?). Those first few weeks are a never-ending whirlwind of information you have to absorb. It can be exciting, but let’s be honest— it can also feel like a lot.

While you’re settling into your new gig, don’t forget about the 401(k) retirement funds you worked so hard to build at your old job. If you’re stressed about what to do with that money, don’t worry—you have options. One of the smartest things you can do with your old 401(k) is roll it over to an Individual Retirement Account (IRA).

What Is a 401(k) Rollover?

A 401(k) rollover lets you transfer your retirement savings from a 401(k) you had at a previous job into an IRA (or into the retirement plan offered at your new job).

Since 401(k) rollovers don’t count toward the annual IRA contribution limit, there’s no limit on how much you can roll over into an IRA from your old 401(k). Plus, there’s no limit on how many 401(k) rollovers you can make in a single year.

So if you have thousands of dollars just sitting inside a dozen (or more) 401(k) accounts from old jobs, you could turn around and roll over every single penny from each of those accounts into an IRA without a problem!

How to Roll Over Your 401(k) to an IRA

Ready to get started? Great! Rolling over your 401(k) to an IRA isn’t too complicated. In fact, you can finish the whole process in four easy steps:

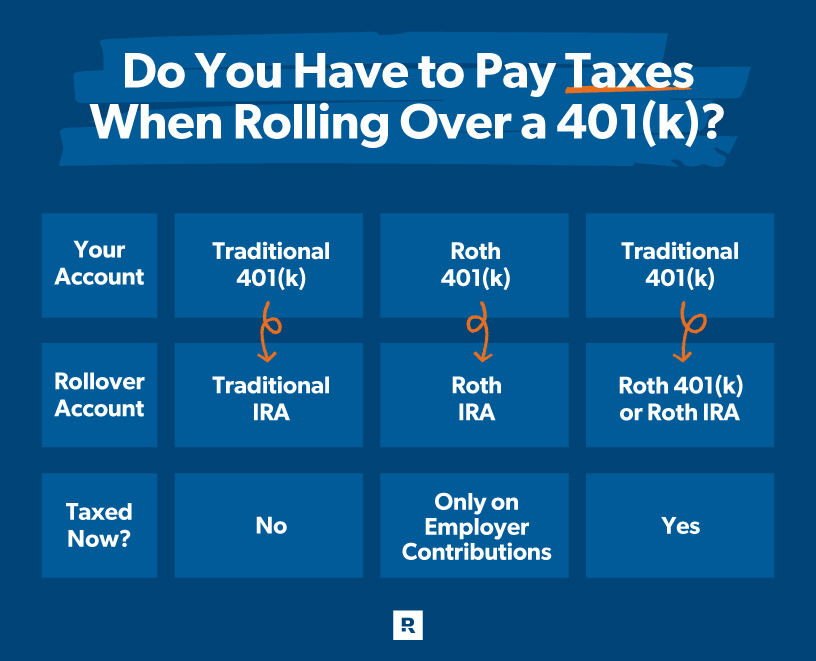

1. Decide between a traditional or Roth IRA.

The type of IRA you roll your old 401(k) money into will depend on what kind of 401(k) you’re transferring the money from.

In most cases, you should roll your old 401(k) accounts into an IRA that has the same type of tax treatment. For example, if you have a traditional 401(k), you should roll those funds into a traditional IRA. And if you have a Roth 401(k), you can transfer most of that money into (you guessed it) a Roth IRA.

Let’s dive a little deeper into each of those scenarios:

Rolling Over From a Traditional 401(k)

If you’re transferring money from a traditional 401(k), then your best option is to roll the money into a traditional IRA. That way, you won’t pay taxes on the money now (but remember, you will have to pay taxes when you start withdrawals for retirement).

But what happens if you roll over money from a traditional 401(k) into a Roth IRA (aka a Roth conversion)?

The bad news is, you’ll have to pay taxes on the money you transfer now. But the upside is that from now on, that money will grow inside your Roth IRA tax-free and you won’t pay taxes on it when you’re ready to withdraw from the account in retirement.

You should only do a 401(k) rollover with a Roth conversion when you’re on Baby Step 7 and have enough cash on hand to pay the tax bill (don’t use money from the account to pay the taxes!). Otherwise, just roll over the money into a traditional IRA and call it a day.

Rolling Over From a Roth 401(k)

If you’re rolling over from a Roth 401(k), that means your contributions to that Roth account were taxed up front, so you can roll that portion (which includes all the growth of your contributions) over to a Roth IRA without having to worry about taxes. And the best part about going with a Roth IRA is that it will continue to grow tax-free—and your retirement withdrawals will also be tax-free. Nice!

Here's A Tip

Your employer’s contributions to a Roth 401(k) are treated like traditional 401(k) contributions. Since that money hasn’t been taxed yet, those funds need to either be rolled over into a traditional IRA or you can pay the taxes to roll them into a Roth account.

Whew! That’s a lot of information, but just remember: Traditional to traditional, tax-free today. Roth to Roth, mostly tax-free today and tax-free in retirement.

2. Open a new IRA or transfer to an existing IRA.

Okay, now you’ll need to open up a new IRA (or choose an existing IRA) to transfer your old 401(k) funds into. Opening a rollover IRA can be as simple as visiting a bank or brokerage firm’s website and filling out an application online. But the best way to open an IRA is to talk with your investment professional. If you don’t have one, we can help you find a pro to help you open up an IRA to move the money into.

If you already have an IRA, you’re ahead of the game. Simply work with your pro to transfer the funds into your existing account—no need to create a new one!

3. Request a direct transfer rollover from your old 401(k).

There are two types of rollovers—a direct rollover and an indirect rollover. Always go with the direct rollover. Here’s why.

A direct rollover transfers the money you had in one retirement account—like your old 401(k) plan—to another retirement account (like an IRA) without you ever touching the money. This is a key detail, because if the money never passes through your hands, you won’t have to pay any taxes or penalties on it.

An indirect rollover, however, is not only more complicated but also riskier. Instead of money being directly transferred from one retirement account to another, the cash goes to you first. At that point, you have 60 days to deposit the funds into a new retirement plan before you get hit with taxes and penalties.

There’s no reason to ever choose an indirect rollover since it leaves you open to a massive tax bill and lots of penalties. Not to mention the temptation to spend some or all of your retirement savings once it’s in your hands! Keep it simple and easy—stick with a direct rollover.

4. Choose your investments.

If you think of your IRA or 401(k) like a piece of luggage, your investments are all the stuff you’ve packed inside it for your trip to your golden years. Once you request a direct transfer rollover to your IRA, you get to pick and choose which investments you want to pack.

We recommend spreading out your investments evenly between four different types of growth stock mutual funds:

- Growth and income (or large-cap) funds

- Growth (or mid-cap) funds

- Aggressive growth (or small-cap) funds

- International funds

Look for funds that have a long track record of strong returns (meaning the fund is at least 10 years old and regularly outperforms other funds in its category). Once you’re all set up, remember to continue investing 15% of your income for retirement so you can keep your nest egg growing!

Invest Like No One Else

From investing advice to wealth management, find a SmartVestor Pro who speaks your language.

Ramsey Solutions is a paid, non-client promoter of participating pros.

What Are the Benefits of Rolling Over a 401(k) to an IRA?

When it comes to rolling over your 401(k) funds to an IRA, there are three major benefits to consider:

You can manage all your investments in one place.

Having two, four or a dozen different retirement accounts from every job you had in the past makes managing your funds a lot more complicated than it needs to be. It can also make it harder to plan for your retirement future. Keep things simple—roll over all your money into one IRA so you can have more control over your retirement funds.

An IRA will give you more investment options.

Most employer plans only give you a handful of investment options, and they’re not always what’s best. Rolling your 401(k) funds into an IRA means you’ll have thousands of mutual funds to choose from—including the top performers in the fund types we mentioned above.

You’ll have more control over your investments.

If you’re already working with an investment professional, you can roll over your 401(k) into an IRA that’s already under their management. That way, your financial advisor can work with you to make sure your money is invested the way you want it.

If the rollover process has seemed too complicated (or you’ve just been procrastinating), don’t stress. It’s pretty simple—especially if you have a pro to help you figure it out!

Next Steps

- Check out your retirement investment potential with our investment calculator.

- Learn more about IRAs, how they work, and the different options they give you.

- If you still have questions about rolling over a 401(k) to an IRA, our SmartVestor program can help you find a financial advisor to guide you through the process.

This article provides general guidelines about investing topics. Your situation may be unique. To discuss a plan for your situation, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

-

Is there a limit to the amount of money I can roll over to an IRA?

-

No, there’s no limit on the amount of money you can roll over into an IRA. However, there are annual contribution limits for IRAs.

-

Does my rollover count as a contribution?

-

Nope! Your rollover to an IRA doesn’t count as a contribution, so it also doesn’t count toward your annual contribution limit, which is great news! That means you can invest more and get to your retirement goals that much faster.

-

Can I take money out of my IRA before I retire?

-

Taking money out of your IRA to use as a down payment or pay off debt is tempting, but it’s a terrible idea. Don’t even consider it unless it’s to avoid bankruptcy or foreclosure. You’ll be hit with crippling early withdrawal penalties and lots of taxes. Plus you’ll be stealing from your future self!

When you treat your IRA like an ATM or emergency fund, you lose out on all the money you would have earned with compound growth. Do your future self a favor and take raiding your IRA before retirement off the table.

-

What’s the difference between a 401(k) and an IRA?

-

A 401(k) is an employer-sponsored plan for retirement savings. Employees can set aside a specific amount from each paycheck to go automatically into their 401(k) for retirement savings. There are two basic types of 401(k)s—traditional and Roth. Both are employer-sponsored retirement savings plans, but they’re taxed in different ways.

An Individual Retirement Account (IRA) is a tax-favored savings account that allows you to invest for retirement with some special tax advantages—either a tax deduction now with tax-deferred growth (with a traditional IRA), or tax-free growth and withdrawals in retirement (with a Roth IRA).

Unlike a 401(k), an IRA is not sponsored by an employer. Instead, you can open an IRA through a bank, brokerage firm, or with help from a financial advisor.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.