A Guide to Life Insurance

Learn the difference between term and whole life insurance so you can confidently decide which is right for you. The key is knowing the true purpose of life insurance: to replace your income.

What's Term Life Insurance?

Term life insurance provides you with simple and affordable coverage for a specific amount of time (hence the word term). If you die at any point during that term, your beneficiaries receive a life insurance payout.

What's Whole Life Insurance?

Whole life insurance is coverage that lasts your whole life. It also includes a cash value account that grows over time. The idea behind whole life is two-fold: It provides a payout when you die and acts as a savings account.

Product Comparison

Let’s look at the differences between term life and whole life insurance.

Term Life

-

Coverage is temporary

-

More affordable

-

No cash value account included

-

Increasing or renewing your policy can be expensive

-

No cancellation fees

Whole Life

-

Coverage lasts your whole life

-

Costs significantly more

-

Most policies pay either the death benefit or the cash value—not both

-

Cash value account grows very slowly

- Can have high cancellation fees

Compare the Cost of Term and Whole Life

Monthly Cost by Age

| Term Life | Whole Life | Savings |

|---|---|---|

| $12.18 | $142.12 | $129.94 |

| Term Life | $12.18 |

| Whole Life | $142.12 |

| Savings | $129.94 |

Life Insurance the Ramsey Way

Here at Ramsey, we teach people how to beat debt, build wealth, and take control of their money for good. That teaching is summed up into our 7 Baby Steps.

Part of the goal of the Baby Steps is to make you self-insured, without the need for life insurance, within 15–20 years. That looks like having 3–6 months of expenses saved, investing 15% of your income for retirement, having college funds for the kids, and owning your home debt-free. But to get there, you need the right life insurance that won’t slow you down. That’s term life.

What You Need and Why

We recommend getting a 15–20-year term life policy worth 10–12 times your annual income. It’s simple, affordable, and does what life insurance is supposed to—it replaces your income if you die. And because term life is way more affordable than whole life, you can invest the extra money you’ll save in good growth stock mutual funds that yield way better returns.

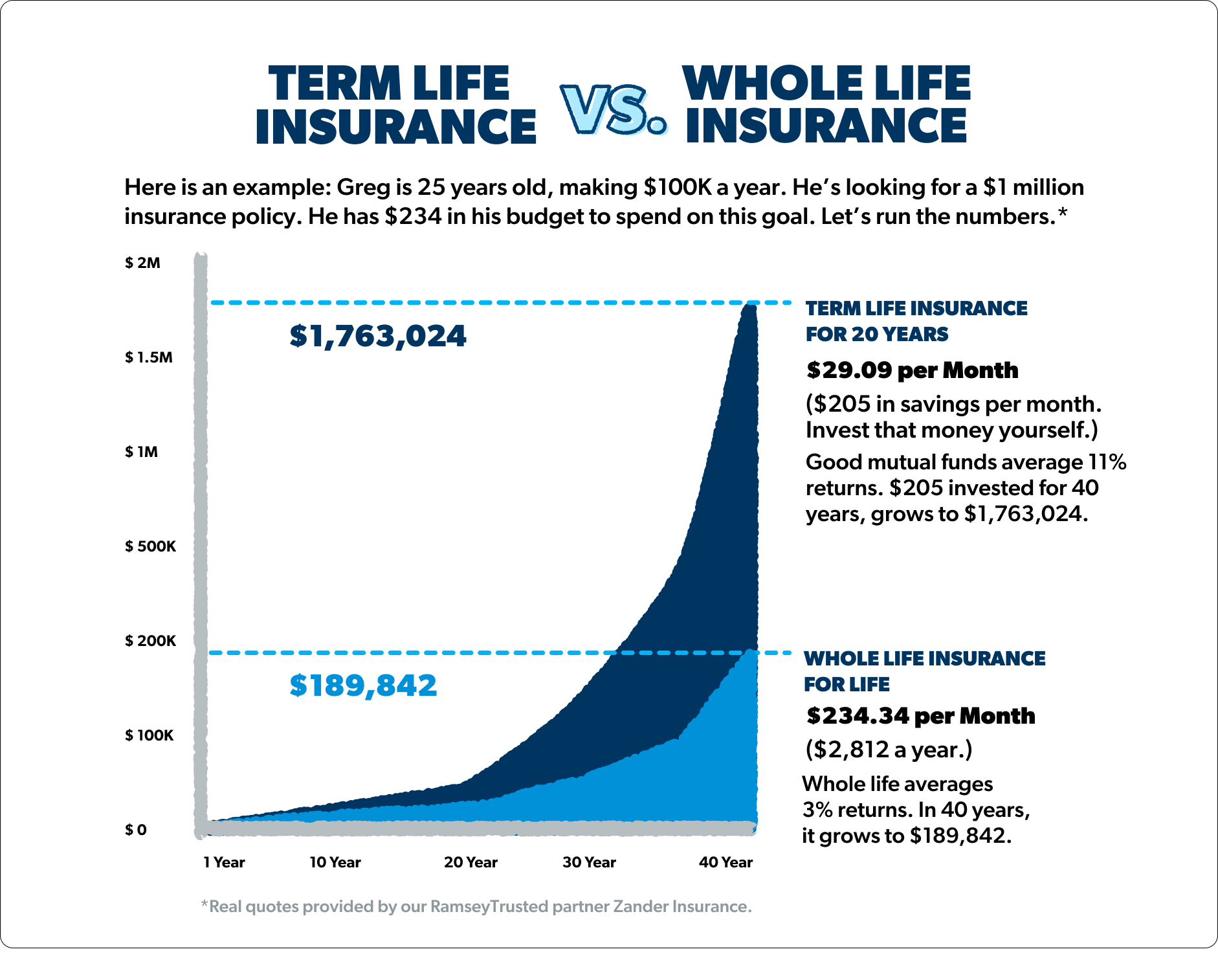

Investing and Life Insurance

We believe that insurance and investing should stay separate. Here is a chart that walks you through how to invest the extra savings you get from a term life policy.

Bottom Line—Get a Plan in Place

Term life is the perfect pairing to the Baby Steps—because by the time you’re on Baby Step 7, you’ll look up and realize you’ve built enough wealth to become self-insured (and then some). The goal is not to depend on life insurance forever, but to use it as a temporary safety net while you’re building lasting wealth. And because term life is much less expensive, it leaves room in your budget to do exactly that.

But you might be wondering if becoming self-insured is really possible. Here’s the truth: it’s absolutely possible. We see millions of people like you do it every day.

Now you have the facts and the time. You can make the choice to change your family tree forever. It’s gonna take some grit—but you can do this.