Paid off $65,000 in 14 months.

“I decided to get serious about paying off debt. No spouse, no kids, just a good time to hustle and lay a good financial foundation.”

Real people just like you make their final student loan payments every day. Use this calculator to see your payoff date and learn how to get there faster with the debt snowball method.

If you stick to minimum payments, student loans hang around for decades. That’s why so many people feel stuck. But when you use the debt snowball, get on a budget, and throw extra money at your loans, things finally start moving. We've seen people cut their payoff timeline from 10–20 years down to 5–7 years! Enter your loan details to see your debt-free date—and how much sooner you can kick Sallie Mae out of your life for good.

Your debt-free date is either a gut check or a green light. Either way, the next step is the same: Find extra money to close that gap faster.

Let’s break down your options using an example. Olivia is an average student loan borrower. Using the debt snowball method, she listed out her debts, smallest to largest, regardless of interest rate. She quickly paid off her credit card debt and can now put an extra $200 toward her minimum payment on her student loans. Here’s how it breaks down with—and without—using the snowball.

Student Loan Balance

Interest Rate

Monthly Income

NO DEBT SNOWBALL

Debt-free date: 14 years away

Interest Paid

Monthly Payment

USING THE DEBT SNOWBALL

Debt-free date: 7 years away

Interest Paid

Monthly Payment

That extra $200 a month could help Olivia save over $10,000 on her loans. Even better, she could spend fewer years weighed down by debt and more years putting her money toward dreams like travel and homeownership.

Wondering how you can find extra money in your budget to throw at your debt? Set up your budget in EveryDollar—Ramsey’s budgeting tool designed to help you make the most of every dollar you have coming in.

We’re big believers in the debt snowball method—paying off your debts from smallest to largest, regardless of interest rate. Here’s why it works:

Personal finance is 80% behavior and only 20% head knowledge. People don’t quit because of math. They quit because they lose steam. Small wins keep you motivated. And motivation is what helps people stay the course and become debt-free.

Paying off student loans by working the debt snowball is part of Dave Ramsey's 7 Baby Steps, specifically Baby Step 2. That’s right in between saving up a $1,000 starter emergency fund (Baby Step 1) and saving up a fully funded emergency fund of 3–6 months’ worth of expenses (Baby Step 3).

Paid off $65,000 in 14 months.

“I decided to get serious about paying off debt. No spouse, no kids, just a good time to hustle and lay a good financial foundation.”

Paid off $83,000.

“I wasn’t stressed about student loans . . . I knew as long as I stuck to the budget, I was going to be okay.”

Paid off $82,000

“When I saw it went under 20 grand, I was like ‘Ooh, let’s go.’”

“I cried the first time we finished a month and actually had money left over. That had never happened before.”

“Now we talk more about our money, we make decisions together, and it’s not stressful anymore.”

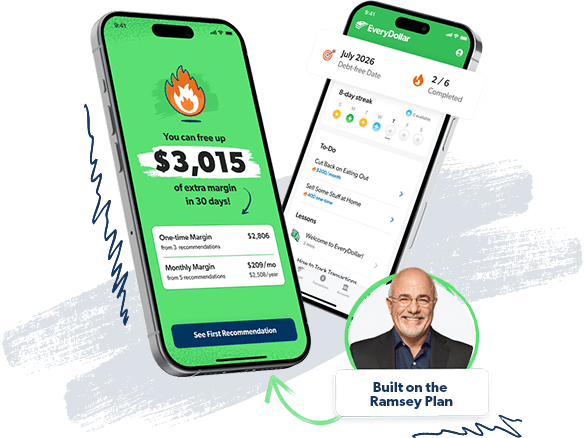

You just saw how much you could save in dollars and time by adding extra money to your minimum payment. EveryDollar shows you exactly where that money is hiding in your current budget—without earning a dollar more. The average user finds $3,015 in the first 15 minutes.*

*Based on the average new user.

This is the original amount you borrowed before interest starts piling on.

Your loan balance is the amount you have left to pay on your student loans. If you took out a loan for $35,000 and paid $5,000 toward the principal, your balance would be $30,000.

This is what the lender charges you to borrow the money. And yep, it’s why student loans can stick around forever if you only make minimum payments.

Your minimum payment represents the total amount you must pay each month toward your student loans. The more you pay in addition to the minimum payment, the faster you can get rid of your student loans.

Making extra payments toward your principal balance on your student loans can help you save money on interest and pay off your loan faster.

This is how long you have to pay off your student loan. But trust us, you’re better off speeding up that timeline by making extra payments.

Amortization is just a fancy word for paying off your loans through fixed monthly payments over time. An amortization table shows how long it’ll take to pay off your student loans, how much of each payment goes toward the principal, and how much goes toward interest.

The debt snowball method is a debt payoff strategy where you pay off debts from smallest to largest balance, regardless of interest rate. You make minimum payments on all your debts and throw every extra dollar at the smallest one until it’s gone. Then you take that payment and throw it at the next-smallest debt—and so on. Each payoff builds momentum, helping you stay motivated and keep attacking your debt.

You can find your student loan balance and interest rate by logging in to your loan servicer account or, if you have federal student loans, visiting studentaid.gov. There, you’ll see your current balance, interest rate, monthly payment and loan status. If you have private student loans, check directly with your lender.

The fastest way to pay off student loans is to use the debt snowball method. After listing out your debts smallest to largest, you’ll create a budget and uncover any extra money you can put toward paying off your debt. Then you’ll pay off your smallest loan first while making minimum payments on the rest. As you knock out each balance, you’ll build momentum and free up more money to throw at the next loan.

If you really want to speed up your debt payments, you've got to cut expenses, increase your income, and put any extra money—like tax refunds or bonuses—straight toward your debt.

If you only make minimum payments, it could take 10–20 years to pay off your student loans. But when you start making extra payments, you can speed up your payoff timeline big-time. Use the Student Loan Payoff Calculator to see how increasing your monthly payment could help you get out of debt faster and keep more of your money.

Yep, this calculator works for Parent PLUS Loans. You can enter your balance, interest rate and monthly payment information the same way you would for any other student loan. The payoff estimates will still show how extra payments can help you get out of debt faster.

Extra payments reduce your principal balance faster, which means less interest builds up over time. That can shorten your payoff timeline and lower the total amount you pay overall. Pro tip: Make sure your lender applies extra payments to the principal instead of future scheduled payments.

Pay off your student loans in Baby Step 2 before you start investing in Baby Steps 4–7. Paying off debt frees up your income and gives you more margin to build wealth later.

The calculator showed you what's possible. EveryDollar shows you how to make it happen, starting with the money already in your budget.

Start EveryDollar for free and tell your money where to go—so you can finally experience financial peace.