What to Do if You’re Drowning in Debt

By

By

Key Takeaways

- If you’re drowning in debt, know that there’s hope . . . but it comes with work and serious behavior change.

- Start by creating a zero-based budget that gives every dollar a job and covers your basics first.

- Cut unnecessary expenses, pause investing, avoid new debt, and boost your income so you can free up as much cash as possible to attack your debt.

- Use the debt snowball method—paying off debts from smallest to largest—to build momentum and stay motivated as you work toward becoming debt-free.

- Follow the Baby Steps plan to move from financial survival to long-term wealth building, one intentional step at a time.

When you’re drowning in debt, it can feel like the world is caving in around you. Your thoughts are swirling and just won’t stop. You’re not sleeping, and you’re worried your next paycheck won’t be enough to provide for your family. And then the questions fueled by endless worry begin: How will I make ends meet? How in the world will I cover my housing expenses this month? Will these debt collectors call my boss? How embarrassing.

You’re not alone. In fact, half of Americans (51%) today are living paycheck to paycheck.1 That means you’re not the only person who’s ever been overwhelmed by debt. Student loan statements, spiraling credit card balances (thanks to those oh-so-high interest rates), and the never-ending cycle of car payments—they all add up fast. It’s no wonder so many wake up each day feeling like they’re carrying a backpack filled with bricks—only these bricks have dollar signs on them.

With bills sneaking up from all directions, it’s easy to see why that sense of financial pressure never lets up. The weight of mounting obligations leaves people wondering how they’ll ever get ahead. But there comes a point when you have to decide that enough is enough. You have to choose—right now—to start changing the way you handle money.

Did you know that personal finance is 80% behavior and only 20% head knowledge? That means with a plan—and a lot of hard work—you can be standing on solid ground in no time. And who knows? You could even become a Baby Steps Millionaire.

Take a breath. You can do this. We believe in you!

Steps To Take if You’re Drowning in Debt

There’s a famous proverb that goes something like this: How do you eat an elephant? One bite at a time.

Your debt might look insurmountable now, but small, focused steps add up over time. Each time you make a bit of headway on your balance, you build confidence and momentum.

It’s about changing your behavior—one step at a time—not just doing complicated math. You’ll savor each victory, no matter how small. Before you know it, you’ll look back and realize all those small choices were moving you forward, turning your mountain of debt into a molehill.

So here are some steps you can take today to kick that debt to the curb.

1. Get on a budget.

Making a budget is one of the most important steps you can take when you’re drowning in debt. It’ll show you where all your money is going and why you feel overwhelmed. This is your first step toward taking control of your money—and never feeling like you’re in over your head in debt again.

When making your budget (and we recommend a zero-based budget), you might be tempted to cover your extra expenses first, like debt payments. But really, you need to make sure your basic needs are met by budgeting for the Four Walls first:

- Food

- Utilities

- Shelter

- Transportation

Now, after you’ve budgeted for groceries, water, electricity, your rent or mortgage, and gas to get you to work (in that order), you can start assigning any leftover dollars to other important needs. Do you have student loans or a car payment? Are those hospital bills piling up? Or maybe your dad’s birthday is next month and you at least need to send a card. Whether it’s $50 or $500, all expenses have to go in the budget. Remember: In your zero-based budget, income minus expenses should equal zero!

Find More Margin. Beat Debt Faster.

Paying off debt doesn’t have to take forever. With the EveryDollar budgeting app, you’ll find extra margin every month so you can pay off debt faster.

2. Cut back on the extras.

Now that every dollar has been given a job to do, it’s time to see where you can cut back.

Start by reviewing your recent bank transactions. Where does your money actually go each month? Are you stopping for coffee every morning? Did that “treat yourself” online order turn into a weekly habit? By looking back at what you’ve really spent, you’ll spot patterns and find those sneaky expenses hiding in plain sight.

Take inventory of any automatic payments that might be draining your bank account. Maybe you have a $7 subscription to the Clean Beard Club. We’re not knocking beards (especially clean beards), but these kinds of expenses add up quickly. Plus, that free gift they offered you when you signed up is probably long gone, leaving you with a subscription you keep forgetting to cancel every single month—and more beard oil than you know what to do with. This isn’t about guilt—it’s about getting honest with yourself.

Don’t get us wrong. We love a good mail day as much as the next person. But if you’re drowning in student loan debt, credit card debt or just-plain-debt debt, you’ve got to make some pretty big changes. You guessed it. We’re talking about cutting back on nonessential items and getting your “want-itis” under control. Here are some tips:

- Make coffee at home (skip the $10 lattes until you’re not drowning in debt).

- Cut back on your grocery bill by clipping coupons and going without the kids so you’re not tempted to overspend on Oreos (leftovers are your friend).

- Don’t even step foot in a restaurant (unless you’re working there).

- Sell everything that’s not nailed down (so much that the kids think they’re next).

Tracking your spending helps you shine a light on places where you can cut back. And those extra dollars you find? They can be put straight toward your debt payments, helping you move toward debt freedom faster.

3. Pause all investing.

Really? Yep. Saving for your future when you’re living paycheck to paycheck (or worse) isn’t the best idea. At least not yet. If you’re still trying to pay off credit cards, an upside-down car loan, or a huge pile of student loan debt, it’s time to press pause on investing—temporarily. This frees up extra cash you can use to pay down your debt.

Here’s another idea: Instead of putting money in investments right now, save $1,000 as fast as you can for a starter emergency fund. It’s just a little more security as you dig yourself out of that hole of debt.

Don’t worry—you’ll get back to investing once you’re debt-free.

4. Don’t take on any new debt.

None. We know it’s hard (and maybe not what you’re used to), but trust us—taking on debt robs you and your family of a secure financial future. The choices you make right now will impact future generations of your family tree. So don’t take on even another penny of debt.

To start with, it’s time to get out your favorite pair of scissors and do a plasectomy. Yup—we’re talking about cutting up those credit cards! The best part? No medical experience required.

You may feel your heart start to race and your hands begin to sweat. But hear us out: Having a credit card for emergencies seems like a good idea until your next “emergency” looks like your next afternoon coffee run. When you cut up those cards, you’re choosing to put an end to that awful cycle of debt for good.

5. Stay current on all your debts.

While you’re working your way out of debt, it’s crucial to keep your accounts in good standing. That means making at least the minimum payments on all your debts each month to keep those scummy debt collectors at bay.

Once you’ve covered those minimums, you can focus on tackling your balances with a solid debt repayment strategy (more on that later). The key here is consistency: Don’t skip minimums in the rush to pay down other balances, no matter how pumped up you are to kick debt to the curb. Keeping everything current keeps your financial game strong and your stress level lower.

6. Increase your income.

Now that you’re on a budget and you’ve decided to stop taking on new debt, it’s time to figure out how to increase your income. Take a second job or pursue a side hustle to bring in the extra money you need (as quickly as possible) to throw at your debt. Whether that’s working at your local coffee shop, mowing lawns, or driving for Uber or Lyft, you’ve got to bring in more cash.

We get it. No one wants to work around the clock. But to see that mountain of debt turn into a valley, you’ve got to start doing something different. Remember: This isn’t forever. You won’t be skipping out on time with family and friends for the long haul. But to get on the right track, you’ve got to make some sacrifices now.

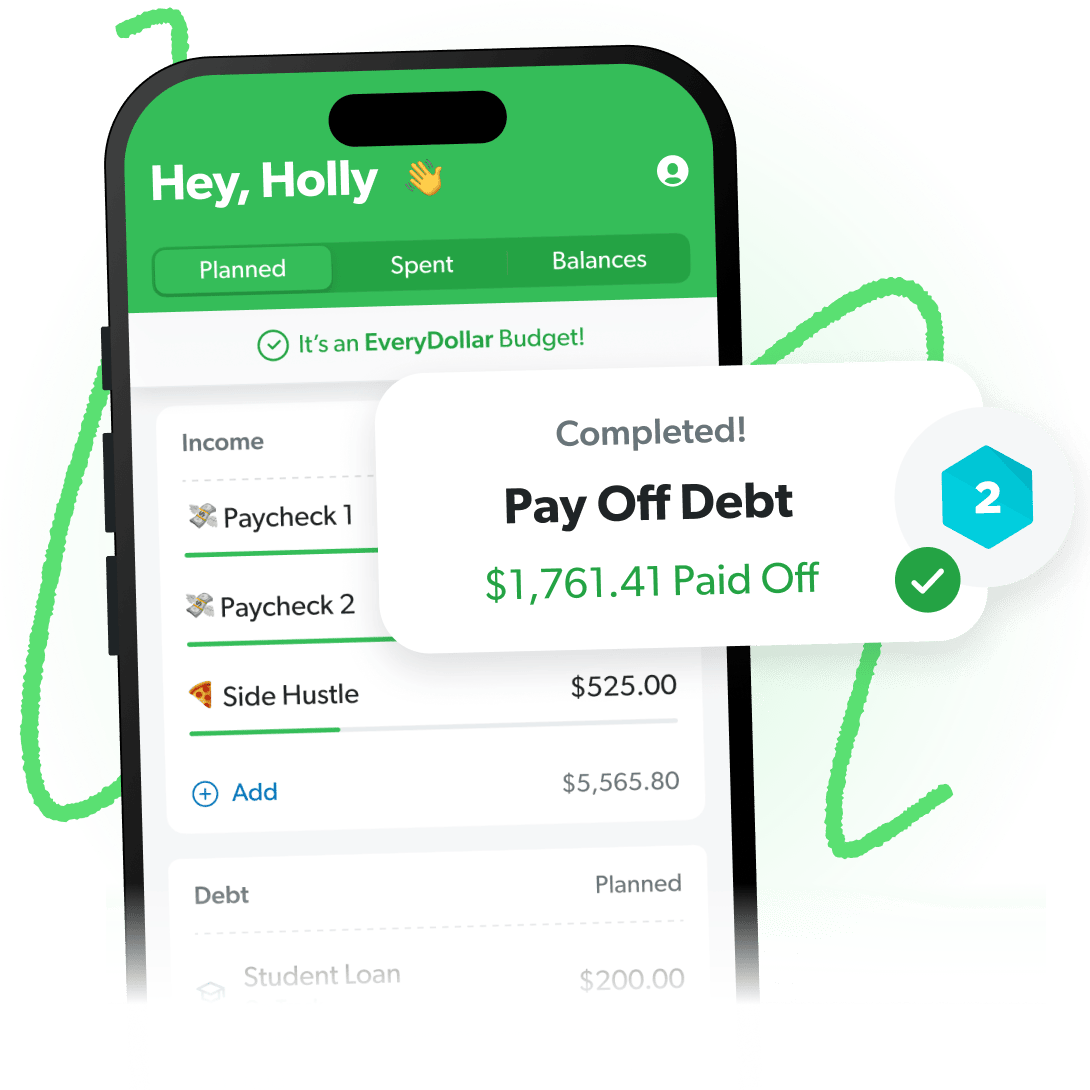

7. Start working the debt snowball.

Now that you’ve got some extra money coming in each month and your $1,000 starter emergency fund standing between you and the unexpected, it’s time to start paying off your debt with the debt snowball method:

- List your debts from smallest to largest—no matter the interest rate. Keep making minimum payments on all of them except the one with the smallest balance.

- Attack your smallest debt with everything you have. Did you sell the couch? Great! Throw your earnings at this debt. Keep putting anything extra you make toward it until it’s gone.

- Once that debt is paid, take what you were paying on it and throw it at the next-largest debt while making minimum payments on the rest.

- Keep this snowball rolling until you’re debt-free!

Debt-Free Date Calculator

Why attack one debt at a time? When you toss your extra money at all your different debts at once, it barely makes a dent anywhere. It’s like trying to bail water out of a sinking boat with a thimble—you just won’t see real progress, and you’ll probably give up before you ever reach dry land.

When you zero in and attack one debt with everything you’ve got, you start to feel some serious traction. Knocking out that first debt (no matter how small) gives you a big emotional win. Suddenly, you’re motivated. You see the progress happening, and you get fired up to tackle the next one. That momentum builds, helping you crush each balance one by one.

Remember, this is about behavior.

Trust us, feelings of progress and accomplishment matter more than you might think. And when you throw all your extra cash at a single target, the principal drops a lot faster—because you’re not spreading your efforts thin across too many fronts. Keep your eyes on one balance at a time, and watch your debt disappear faster than you ever thought possible.

8. Stop the comparison trap.

Comparison is one of the worst things you can do while you’re getting out of debt, and social media is one of the biggest triggers. If you’re scrolling through your news feed and see your friend (who you haven’t talked to in years) on a European vacation with her mom, that doesn’t give you permission to plan a fancy vacation too. Nope. Europe will still be there when you’re completely debt-free.

When you’re in debt and going after it with gazelle intensity, it’s hard not to compare your financial situation to someone else’s. But here’s the truth: You don’t actually know their situation. You don’t know if your friend put her fancy vacation on a credit card. But you do know that once you’re out of debt, you’ll be able to plan exciting (and paid-for) trips of your own. Listen: The Joneses are broke. If you’re falling into the comparison trap, it might be time to take a much-needed break from social media.

9. Start (or keep) working the Baby Steps.

The tips we’ve gone through here are more than just good ideas. They’re part of a proven and practical plan to change your financial future. They’re called the Baby Steps—seven steps to help you pull yourself out of the debt quicksand and onto more stable ground.

Baby Step 1: Save $1,000 for your starter emergency fund.

Baby Step 2: Pay off all debt (except the house) using the debt snowball.

Baby Step 3: Save three to six months of expenses in a fully funded emergency fund.

Baby Step 4: Invest 15% of your household income in retirement.

Baby Step 5: Save for your children’s college fund.

Baby Step 6: Pay off your home early.

Baby Step 7: Build wealth and give.

We’ve already covered Baby Steps 1 and 2 in this article. Once you’re out of debt, you can go even further and really change things for yourself and your family!

Get Started With EveryDollar

It may feel like you’re drowning in debt right now. But like we said earlier, you can change that—starting today. Once you’ve had it with debt (and we hope you have), you can climb your way out of it. Remember: one bite at a time.

Want a tool that will help you make your debt-free dreams come true? Try EveryDollar. This one-stop shop will help you create a budget, give you a customized plan to reach your goals, and provide resources to keep you motivated.

Next Steps

- Review your last 30 days of bank transactions and cancel at least one unnecessary subscription or expense.

- Set aside your first $1,000 for a starter emergency fund as quickly as possible, even if that means selling items or picking up extra work.

- List all your debts from smallest to largest and make a plan to start attacking the smallest one with every extra dollar you can find.

- Create a zero-based budget in EveryDollar and make sure your Four Walls—food, utilities, shelter and transportation—are covered first.

Don’t have EveryDollar? Download it today!

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.