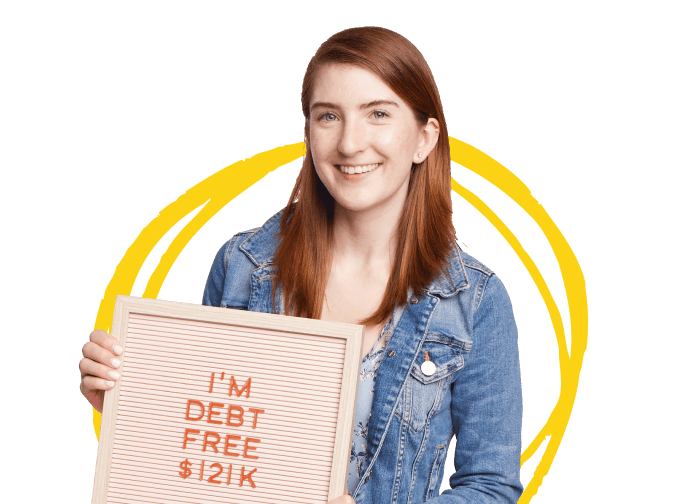

"I paid off $121,000 in 28

months. I feel strong! The

burden is gone!"

Feeling stuck? This Debt Snowball Calculator shows when you’ll be free from debt—and how to get there faster with a simple, step-by-step plan.

Use the debt calculator to find your exact debt-free date by entering each debt’s balance, interest rate and minimum payment—plus any extra amount you can put toward your debts each month. Then the Debt Snowball Calculator will figure out the month your total balance will reach zero and how much sooner that could be if you throw extra money toward it.

Want to see how fast you can get out of debt? Start here.

Include credit cards, medical debt, car loans, student loans and personal loans.

This is the total amount you owe on each debt.

This is what you’re required to pay each month to avoid penalties.

This is usually written as a percentage and is often called the APR. Log in to your account and look for account details, or download a monthly statement. If you don’t know one of your rates, the calculator will suggest one based on national averages and the type of debt.

Add up your salary, side hustles, bonuses, spouse’s pay and any other income.

Think: What's left after you’ve taken care of your Four Walls (food, utilities, shelter and transportation)?

That’s okay! Just put in your best guesses for now. We just want to help you get a picture of where you’re at.

You’ll add each debt to the calculator one by one. Include credit cards, car loans, student loans and all other nonmortgage debt.

If you’re not sure about this, when you choose the specific debt type, we’ll fill in the average rate for that kind of debt.

Remember, this is the total you still owe on that specific debt.

This is what your statement says is owed each month.

Go ahead and give the debt a name so you can keep them all straight.

Take the total you added up in the What You’ll Need section.

Use the extra money you added up in the What You’ll Need section.

Then, the calculator will show how quickly you can be debt-free.

Take that date in for a second. This is the date you kick debt for good. If it feels far away, don’t panic—you’ve got options. Tighten up your budget, cut a few expenses, or bring in extra income.

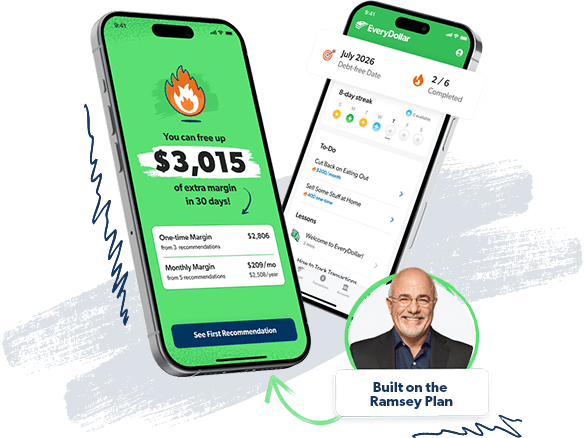

The best way sort out the money mess is with our budgeting app, EveryDollar. It helps you set goals, find extra money in your budget, and easily track your expenses.

You might have never budgeted before, or maybe you’ve tried and quit. But listen, this is where it gets real. Getting out of debt takes focus and intensity—but it’s temporary. And on the other side? You’ll live like no one else.

Your money will be yours.

You’ll be able to say yes more than no.

You’ll finally have breathing room.

Stay locked in. You’re closer than you think. And you don’t have to do this alone! Millions of people have done it—and you can too.

This is how people actually get out of debt. Dave Ramsey has taught the debt snowball method for over 30 years. It’s actually pretty simple. Here’s how it works:

Those quick wins of paying off the smaller debts give you the boost you need to stick with the plan until you’re debt-free. Small wins turn into big progress, and that’s how you get out of debt for good. But it all starts with a budget.

Now that you’ve read about the snowball method, let’s talk about the avalanche method. In this method, you pay off the highest interest rate first—and technically, the math shows that can save you some money over time. But if this was about math, you wouldn’t have gotten into debt in the first place.

Medical Bill

Credit Card

Student Loan

RAMSEY RECOMMENDS: SNOWBALL METHOD

Start with the $500 medical bill to get a quick win.

$500 medical bill

Quickly paid off

$2,000 credit card

Goes faster with money from step one

$10,000 student loan

Knocked out last with your full snowball of payments

THE ALTERNATIVE: AVALANCHE METHOD

Start with the 18% credit card to save interest—if you finish.

$2,000 credit card

Takes a few months

$10,000 student loan

Long stretch with no wins

$500 medical bill

If you even get to this after losing momentum

The avalanche saves more money if you stick with it the whole time. But there’s something you likely aren’t considering.

Let’s get real. After working with people for over 30 years, we’ve learned that personal finance is 80% behavior and only 20% head knowledge.

Most people don’t quit because of math. They quit because they get discouraged. With the avalanche method, when the first win takes too long, motivation drops. And when motivation drops, people stop.

The debt snowball method gives you quick wins early, keeping you motivated so you keep going.

The debt avalanche method may win on paper. But the debt snowball method wins in real life—because it helps people stay in the fight long enough to finish.

You don't have to do the plan perfectly, but you can't get out of debt on accident. Like Dave says, “Winning is an intentional act.” You just have to keep showing up every day and push toward your goal.

You’ve got your debt-free date. Now it’s time to make a plan to get there. That plan starts with a budget.

A budget is how you take control of your money. Before the month begins, you tell every dollar where to go—so you don’t end up wondering where it went. You’ll see what you can cut, what you can keep, and how much you can throw at your debt. You’ll feel like you just got a raise!

Ready to build your budget? Get started for free with our EveryDollar budgeting app.

This is where the 7 Baby Steps come in. This is the plan Dave Ramsey has taught for over 30 years to help millions get out of debt, build savings, and create lasting wealth. Here’s a rundown of the first few steps:

There are four more steps after that, but the end goal is learning how to live and give like no one else—able to cover all your bills while building wealth for the future and being free to give generously! Want to see the full plan? Check out all 7 Baby Steps and what comes next.

Trusted by over 10 million people.

"I paid off $121,000 in 28

months. I feel strong! The

burden is gone!"

“We're not stressed anymore. Our journey's in our hands now. We get to choose what we want to do."

"There’s freedom on the other side of debt. You don’t have to live like everyone else. I wanted something different for my family."

This is the smallest amount you must pay each month to stay current on a debt. Example: A $2,000 credit card may have a $40 minimum payment.

This is the total amount you currently owe on a debt, or what you would pay if you paid it off in full today.

Your rate is the fee a lender charges when you borrow money. It’s usually a percentage of the balance. Example: The average credit card has a 21% interest rate.

This refers to the original amount you borrowed, not including interest. Example: If you take out a $10,000 loan, that $10,000 is the principal.

This includes all debt except your home loan, like credit cards, car loans and student loans.

This is the estimated date when all your nonmortgage debt will be paid off.

This method is where you pay debts from smallest to largest balance to build momentum.

A debt calculator uses your balances, interest rates and minimum payments—plus any extra payments you can add—to help you see when you can be debt-free.

The debt snowball method pays off the smallest balance first. The avalanche method targets the highest interest rate first. The avalanche can save you a little money on interest. But the snowball builds momentum with early wins, which helps you stick with it and actually pay off all your debt.

It depends on your total balance, interest rates, minimum payments and how much extra you throw at it. Many people with $20,000–50,000 in debt become debt-free in 18–48 months with focused effort. Use the calculator to get your exact date.

• Name of each debt

• Type of debt

• Current balance

• Interest rate (APR)

• Minimum monthly payment

• Any extra money you can afford to add

You can use estimates. Just get started so you can see what’s possible.

Yes. Research shows that early wins matter. Paying off smaller debts first builds momentum and keeps you motivated to keep going. That’s why millions of people have used the debt snowball method to get out of debt.

Yes. It’s completely free, and you don’t need to create an account or give us your email.

Your debt-free date is the month and year your last debt will be paid off—the moment you owe nothing on your nonmortgage debt.

The debt snowball focuses on nonmortgage debt like credit cards, car loans and student loans. In the 7 Baby Steps, you pay off your home later—after all other debt is gone.

Don’t waste another night lying awake, staring at the ceiling, stressed about money. Start EveryDollar for free today and take your first step toward financial peace.