How Does Health Insurance Work?

11 MIN READ | OCT 14, 2024

By

By

Health insurance is complicated stuff—premiums, deductibles, coinsurance, bronze, silver, gold plans (what is this, the Olympics?!). Then throw in HSAs, HMOs, PPOs . . . what?! Trying to figure it out can be tough.

If all these terms have you scratching your head, wondering how health insurance works, don’t worry. We’ve got your back.

We’ll break down exactly how health insurance works. Because it’s a heck of a lot easier to get the right coverage if you actually understand it.

What Is Health Insurance?

Health insurance is a way to pay for the costs of health care by transferring risk to an insurance company. Once you pay your deductible, the insurance company will cover some or all of your care. This way you won’t find yourself drowning in medical bills and facing financial ruin.

While there are a boatload of different kinds of plans, there are really only two main types of health insurance—private and public. Every plan falls underneath one of these.

Private coverage is the kind you get through your employer, union or the armed forces. You can also buy it on your own through the government’s marketplace—Healthcare.gov—but only during a certain time of year called open enrollment.

Public insurance is provided by the government. Think Medicare (for those 65 years or older), Medicaid (for low-income families) or care from the Department of Veterans Affairs.

Basic Health Insurance Terms

Since there’s practically a health insurance term for each letter of the alphabet, here are some definitions that will help you better understand how health insurance works.

Your premium is the amount you pay monthly (sometimes annually) for coverage.

Your deductible is the amount you have to hand over before your insurance money kicks in. For example, if your deductible is $3,000, you’d have to pay $3,000 for care before your insurance company ponies up.

Your maximum out-of-pocket costs are the max of what you’ll pay in a given year. So if your plan’s maximum out-of-pocket costs are $6,000, once you pay that amount, your insurance will pay everything over that during the rest of the year.

Coinsurance is related to the maximum out-of-pocket costs. It’s a way to split the costs of medical services with your insurance carrier after you’ve hit your deductible.

Your copay is a set amount you pay for things like doctor’s visits or other services. It applies even before you hit your deductible. For instance, if your copay is $20 to see a doctor about that bug that flew in your ear, and now you’re hearing a constant buzzing noise, you’ll only pay $20. The insurance carrier will cover the rest. Nice!

Covered costs are services your insurance company will help pay for. Think doctor’s visits, tests, preventative care, etc.

And this is only the tip of the health insurance iceberg (crazy, right?). There’s a ton of other terms—HMO, PPO, HDHP, HRA and HSA, just to name a few. We won’t get into all of them here (you’re welcome), but you can definitely dig into these plans next time you’re looking for some light beach reading . . .

Who Needs Health Insurance?

Everyone. If you’re alive on Planet Earth, you need some form of health insurance. It’s the best way to protect yourself from the financial problems that can easily happen due to unexpected medical events. No one’s totally immune to serious medical situations. That’s why health insurance is a must.

You and your family need that extra layer of protection. It’s like keeping an umbrella in the car for rainy days. Most times you don’t need it. But when it does rain, it really comes in handy. In fact, medical bills are the number one cause for bankruptcy in America. It’s really easy to rack up hundreds of thousands of dollars in medical expenses.

Even if you’re unemployed, you still have options like COBRA insurance to make sure you’re covered. And if you’re self-employed, you won’t be able to get an employer plan, but you can still buy coverage on your own.

The bottom line? Whatever your situation, you need health insurance. Period. Full stop.

Insurance Can Be Confusing. We Have Someone Who Can Help.

RamseyTrusted insurance pros are pre-vetted—which just means we’ve filtered out all the duds. And they make getting health insurance one less thing to stress about. Plug in your zip code to connect with an agent and get started.

How Does Health Insurance Work?

So, how does health insurance work?

First, you pay a monthly premium to your insurance company. They then agree to pay for any medical costs you might need throughout the year—but only after you pay your deductible. So no matter what, you’re going to have some out-of-pocket costs.

If you want to pay fewer out-of-pocket costs, you can go with a lower deductible—but you’ll pay a higher monthly premium. And vice versa, if you want to pay a lower premium—less per month—you can opt for a higher deductible.

Once you hit that deductible, you can file a claim. If it’s covered, your insurer will cover the costs of the care. If they deny your claim, you can appeal it. Worst-case scenario, you’ll have to cover the costs on your own.

Another thing to keep in mind is that, depending on your plan, you may be limited to a certain network of providers. Some plans don’t let you simply use any doctor you want. You have to work inside of an established network.

What Does Health Insurance Cover?

Health insurance helps cover most of the costs of medical care. Things like prescription drugs, hospital stays, emergency care, preventive and non-preventive care, regular doctor’s visits, and other medical services like X-rays, CT scans or meeting with specialists (depending on your plan). And remember that some of this care only kicks in after you’ve met your deductible.

Because of changes from the Affordable Care Act (ACA), health insurance has to cover at least these 10 essential services:

- Preventive care—like routine checkups for you or your kids

- Hospitalization

- Lab tests—think blood work

- Pregnancy, maternity and newborn care for that new little one

- Emergency room care—depending on the circumstances, your insurance might still cover this if it’s out of network.

- Mental health, substance-abuse services

- Rehabilitation services

- Outpatient care—service you get when you don’t have to stay at the hospital

- Pediatric services (along with oral and vision care)

- Prescription drugs1

Another change due to the ACA is that insurance companies are no longer allowed to deny you based on preexisting conditions. So if you have diabetes, you’ll now be able to get covered.

What Does Health Insurance Not Cover?

There’s always a catch, isn’t there? Health insurance isn’t a magic bullet that addresses every possible thing that could go wrong. There are some things it usually doesn’t cover.

Here are a few examples:

- Plastic surgery—Sorry, your insurance won’t cover that nose job you’ve always dreamed of.

- Alternative or homeopathic medicine like acupuncture, massage or naturopaths.

- Experimental stuff—If there’s new technology out there that your doctor is recommending, it probably won’t be something your carrier will cover. Just check in advance to see if it’s an option.

- Long-term care—A big misconception about health insurance is that it covers long-term care. It doesn’t. And this myth can cause real problems since long-term care is so pricey.

- Elective surgery—These are things you might want done but your doctor can’t prove you need.

- Weight-loss surgery—Although some plans do cover this if it’s deemed medically necessary, most times you’ll have to pay for this out of pocket.

- Medical care that’s unapproved—This means you didn’t get the sign-off from your health insurer before you got the care. Pro tip: Check with your insurance company before you get the medical care to make sure they’ll cover it.

The moral of the story? Carefully read your Summary of Benefits Coverage to confirm that whatever medical care you need is actually covered. And reach out to your insurance company to double-check.

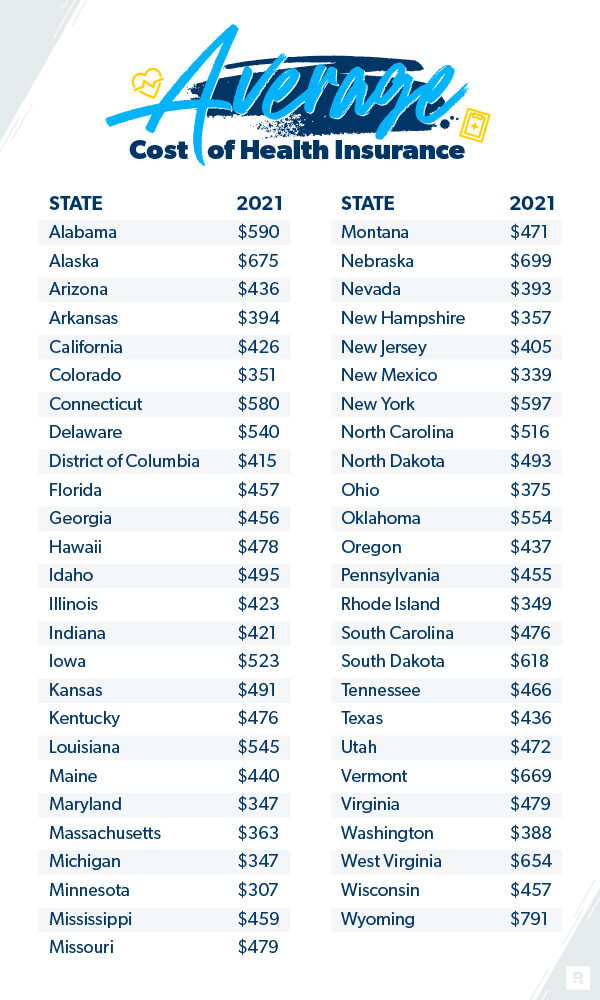

How Much Does Health Insurance Cost?

The cost of health care insurance varies pretty widely and can be hard to pin down. But there is some data on it.

The average American pays $452 per month for marketplace health insurance.2 The average family can expect to pay $1,779 per month.3

And if it seems like health care insurance is getting more expensive, it’s because it is. Over the last decade, costs have risen significantly. For example, the average family is paying 55% more in their premium in 2020 versus 2010 according to the Kaiser Family Foundation.4 And that number is up 22% since 2015.5 But premiums have only risen 4% when comparing 2020 against 2019.6

Health care costs are based on a ton of different factors—things like your age, how many people are on your plan, your level of coverage, where you live and who your employer is. Some of these things aren’t in your control, but some are.

There are some things you can do to save money on your health insurance premiums. And as we saw earlier, if you want to pay less now (but more later), opt for a lower premium and higher deductible. If you’d rather pay more up front, pay a higher monthly premium and a lower deductible.

A Health Plan Example

So, we’ve dug into the health insurance terms, broken down how health insurance works, and learned what is and isn’t covered. Now we’re ready to look at a few real numbers. Health insurance can make a huge difference in covering life’s unexpected events and keeping you out of medical debt.

Let’s pretend you got in a serious car accident (I know, it’s not fun to think about but bear with us).

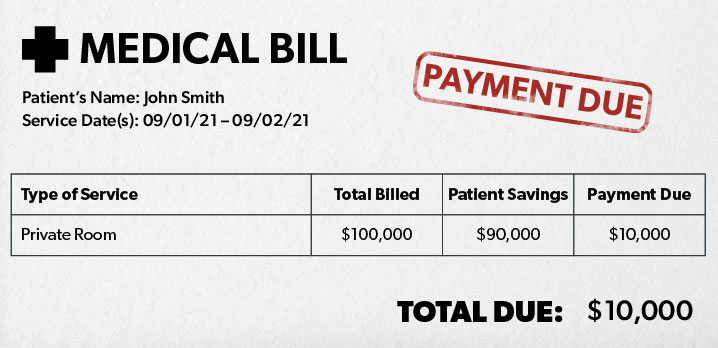

You get home from the hospital after making a speedy recovery (great job!). You open your mail. You’re thinking the bill might be maybe around $10,000. Maybe $20,000 tops. Nope. A whopping $100,000. What?! But I was only in the hospital for two days, and the food wasn’t even that good.

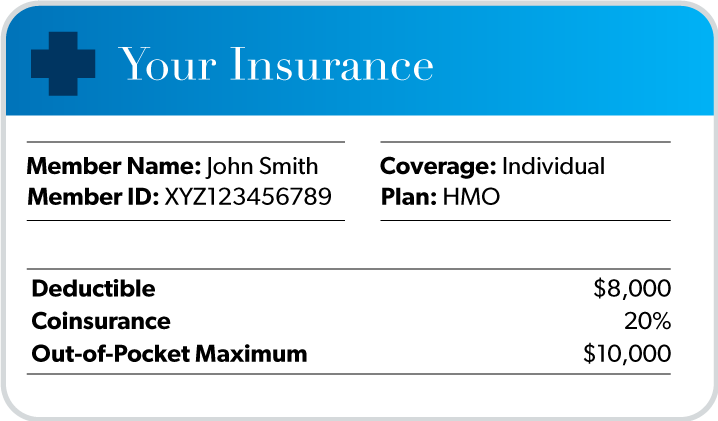

Thankfully you thought ahead for moments like this. You have solid health insurance coverage in place. Here’s what it looks like:

- Your deductible: $8,000

- Your coinsurance: 20%

- Out-of-pocket maximum: $10,000

Assuming your care was from doctors and hospitals that were inside your insurance company’s network, here’s what happens to that $100,000 bill.

Assuming your care was from doctors and hospitals that were inside your insurance company’s network, here’s what happens to that $100,000 bill.

First, you have to pay the $8,000 to meet your deductible.

Next, you’re going to need to pay 20% of the costs until you hit your out-of-pocket maximum. So you’ll end up paying another $2,000 until you hit that $10,000 limit.

But here’s the good part. Even though you just spent $10,000, your insurance company will (finally) kick in and cover the rest of the bill.

So here’s the summary of what you’d end up paying in total after the $100,000 event:

Total cost of medical care: $100,000

Your share: $10,000

Your insurance company’s share: $90,000

It’s obvious just how helpful health insurance can be in times like this. Without it, you’d be stuck with that $100,000 bill. Not good.

It’s obvious just how helpful health insurance can be in times like this. Without it, you’d be stuck with that $100,000 bill. Not good.

What Are the Benefits of Health Insurance?

Even though it might seem like a pain, there are a lot of benefits to health insurance.

Here are just a few:

- You’ll save money. Health insurance helps offset what can sometimes be sky-high health care costs. You won’t be stuck paying for every penny out of pocket.

- Access to a Health Savings Account. Certain plans will allow you to put money in a pretax account called a Health Savings Account (HSA). HSAs are like a superpower when it comes to paying for medical expenses. If you can get one, you should.

- You’ll be healthier. Having health insurance—with typically no out-of-pocket costs for preventive care—will mean you’ll catch health issues early on.

- Peace of mind. You’ll sleep better knowing you and your family are protected if something unexpected happens.

- Avoid financial ruin. Health insurance will keep you out of bankruptcy or fighting hospitals over hundreds of thousands of dollars in medical care. Yuck!

What’s the Best Way to Get Health Insurance?

There are a couple different ways to get health insurance. First, you can purchase it through your employer’s plan. Sometimes it’s cheaper to buy it this way since they can get a discount from buying in bulk. But this isn’t always the case. You should consider other options instead of just automatically signing up for an employer’s plan.

Another way is through the government marketplace. Around 175 insurance companies offer packages there. And depending on your income, you could qualify for government tax incentives that will bring down the cost of your premiums. A third way is to buy it directly from health insurance companies.

Finally, since health insurance can be super complicated, it can be hard to figure out the best plan for you and your family. You don’t want to overpay or underpay. That’s why put together a list of proactive next steps you can take today to understand what's best for you and how to get the right coverage in place.

Next Steps

- Read more about why health insurance is an essential part of a smart financial plan.

- Go deeper to learn more about how to get health insurance.

- To choose the right type of health insurance for you and your family, talk to our RamseyTrusted health insurance partner Health Trust Financial. Their independent agents really know their stuff. In fact, they've been serving Ramsey fans for over 20 years. When you work with Health Trust Financial, they can set you up with the best health insurance quotes and policies for your situation and explain all of the insurance jargon to you. Plus they'll never try to sell you something you don't need. Connect with them now!

Interested in learning more about health insurance?

Sign up to receive helpful guidance and tools.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.