What Is Full Retirement Age? And What Does It Mean for Your Retirement?

8 MIN READ | APR 21, 2025

By

By

Key Takeaways

- Your full retirement age (FRA) depends on when you were born. It’s age 66 for anyone born from 1943 to 1954—then it increases by two months for each birth year from 1955 to 1959, and age 67 for those born in 1960 or later.

- Benefits are calculated based on your average earnings over your highest-earning years, using a complex formula to figure out your monthly payment.

- You can start receiving reduced monthly benefits at age 62, wait until your FRA for full benefits, or delay until age 70 for increased benefits.

- Don’t rely on Social Security alone to support you in retirement. Planning, saving and investing are essential for financial peace in your golden years.

We tell people all the time that retirement isn’t an age—it’s a financial number. And it’s true! With careful planning and consistent investing, you can retire on your own terms well before you’re “supposed” to retire.

But Social Security didn’t get the memo, apparently. They have something called a full retirement age (FRA), which is used to figure out when folks can receive their full Social Security benefits.

Hopefully you’ll be living your dream retirement by then, but let’s talk about full retirement age and what it might mean for your retirement future.

What Is Full Retirement Age?

Full retirement age, sometimes known as normal retirement age, is the age when you can start receiving your full Social Security retirement benefits.1 But not everyone has the same FRA.

What Is My Social Security Full Retirement Age?

Your full retirement age depends on what year you were born. For anyone born from 1943 to 1954, your FRA is age 66. After that, the full retirement age increases little by little for folks born from 1955 to 1960 until it reaches age 67. If you were born in 1960 or later, you become eligible for full Social Security retirement benefits once you hit age 67.2

That’s where things stand today, but there have been discussions about raising the full retirement age at some point to keep Social Security’s retirement trust fund from getting tapped out.3 It’s all just talk at this point, but it is something to keep an eye on.

|

Social Security Retirement Age Chart |

|

|

Year of Birth |

Full Retirement Age |

|

1943–1954 |

66 |

|

1955 |

66 and 2 months |

|

1956 |

66 and 4 months |

|

1957 |

66 and 6 months |

|

1958 |

66 and 8 months |

|

1959 |

66 and 10 months |

|

1960 and later |

67 |

How Is My Full Retirement Age Benefit Calculated?

Your FRA benefit is calculated based on how much money you’ve made during your working career. The Social Security Administration (SSA) uses a math formula and something they call bend points to figure out how much your benefit checks should be.

Don’t worry, we’ll walk you through all of it nice and slow. So, grab a pencil and a sheet of paper—it’s time to do some math!

Average Indexed Monthly Earnings (AIME)

The first thing the SSA will do is figure out your average indexed monthly earnings (AIME). In plain English, that’s your average monthly pay over the last 35 years.4

They’ll find that number by adding up your annual income from your top 35 earning years and then dividing that amount by 420 (that’s the number of months in 35 years).

So, let’s say your average salary from your top 35 earning years is $50,000. In this case, your AIME is (drum roll, please) . . . $4,167. But we’re not stopping there.

Bend Points

Next, we have to run that AIME number through those bend points we were talking about earlier. The math nerds at SSA use this equation to figure out your actual full retirement age benefits. Bend points work just like tax brackets, except they’re designed to give you money instead of taking money away . . . so, that’s nice!

Here’s how it works: The less money you’ve made throughout your career, the higher percentage of your salary you’ll get back from Social Security in retirement. That way, SSA benefits replace a bigger chunk of lower-wage workers’ income in retirement.

For those of you who start getting benefits in 2025, you can figure out your full retirement benefit with this formula.5

90% of the first $1,226 of your AIME

+

32% of your AIME between $1,226 and $7,391

+

15% of your AIME over $7,391

=

Your Full Retirement Age Benefit

Now that we’ve got the equation laid out, let’s run that $4,167 average monthly payment we used earlier through those bend points. First, you’ll keep 90% of the first $1,226 ($1,103)—then 32% of everything you made between $1,226 and $4,167 ($941). Since your AIME is below $7,391, we don’t have to worry about that third bend point.

So, if you wait until your full retirement age to claim your retirement benefits, you can expect monthly Social Security checks in retirement of around $2,044 . . . a little more than half of the money you would’ve earned each month during your career.

Make an Investment Plan With a Pro

SmartVestor shows you up to five investing professionals in your area for free. No commitments, no hidden fees.

Ramsey Solutions is a paid, non-client promoter of participating pros.

Do I Have to Wait Until Full Retirement Age to Start Taking Benefits?

Here’s some good news: You don’t have to wait until you reach your FRA to start getting money from Social Security.

In addition to waiting until full retirement age, you have two other options: Take retirement benefits early starting at age 62, or delay taking benefits up until your 70th birthday.6

Both have their pros and cons, so let’s take a closer look at early and delayed retirement age benefits.

Early Retirement Age

You can start taking Social Security benefits as early as age 62 (any time between age 62 and your full retirement age is considered early retirement age).

But there’s a catch: The sooner you take retirement benefits, the less money you’ll get from Social Security each month—and once you decide to start taking monthly payments, you’re stuck with those payments. No take backs!

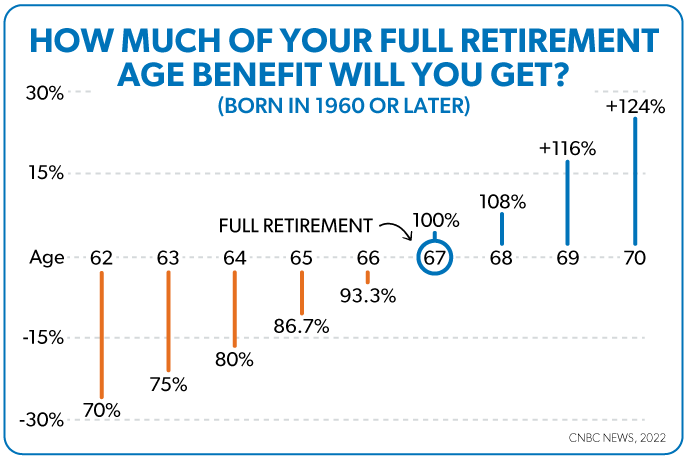

For example, if you were born in 1960 or later and you start taking retirement benefits at age 62, you’ll receive 70% of your full retirement age monthly benefit (if you were born before 1960, those percentages are a little different).7 But on the plus side, you can put that money to use right away, and you don’t have to wait five-ish years to start getting Social Security checks.

Delayed Retirement Age

If you don’t need the money right away, you can hold off on taking benefits until after you reach full retirement age and receive a larger monthly benefit. Anything beyond your full retirement age is considered delayed retirement age, and your benefit increases until your 70th birthday.

If you wait until age 70 to start receiving retirement benefits, then you’d get monthly payments that are larger than your full retirement benefit (124% of your FRA benefit if you were born in 1960 or later, to be exact).8

Using our example above, let’s say you decide to take early retirement benefits at age 62. That means your monthly benefits payment would be about $1,430. But what if you waited until age 70? Then, Social Security would send you monthly checks worth about $2,535.

So, When Is the Best Time to Start Taking Social Security Benefits?

All this raises the question: Should you wait until full retirement age—or later—to start taking Social Security benefits? Or does it make more sense to take the benefits as soon as you can?

Financial expert Dave Ramsey says it makes sense (in most cases) to take the money early and often. Social Security payments die when you die, so you might as well get all you can get as fast as you can get it. And if you don’t need that Social Security money, you can always invest it in good growth stock mutual funds and just let it grow. That way, the money at least becomes part of your estate. If you take nothing, you get nothing!

But at the end of the day, these Social Security benefits shouldn’t really matter all that much. Remember, Social Security is designed to replace some of your income in retirement—not all of it.

If you invest 15% of your income in tax-advantaged retirement accounts during your working career, you’ll have so much money in your nest egg that Social Security will simply be the icing on the cake . . . a cake made of all the money you’ve invested in retirement accounts, like your 401(k) and IRAs!

What Is the Average Retirement Age?

Do most people wait until they reach full retirement age to call it quits? While waiting until then means a larger retirement benefit check, most people don’t wait that long to retire. In fact, the average retirement age for current retirees is 62. Meanwhile, people still in the workforce expect to work a little longer—they think they’ll retire at age 66.9

Can I Collect Social Security Benefits and Keep Working?

Once you hit full retirement age, you can continue to work and earn as much as you want and still receive your full retirement benefits at the same time.

What if you start receiving benefits before full retirement age and keep working? Then it’s likely at least some of your retirement benefit will be withheld. Womp womp. But it’s not all bad: Social Security will send you a higher monthly benefit once you reach full retirement age to make up for it.10

Either way, with a constant dark cloud of uncertainty around whether Social Security will keep providing full benefits in the years to come, it’s more important than ever to take charge of your retirement future.

Next Steps

- If you want a better understanding on where you are now and how much you’ll need to save for the retirement you want—without having to rely on Social Security—take the R:IQ retirement assessment.

- Ready to start budgeting for today and your future? Check out EveryDollar. Our free budgeting app will help you make a solid zero-based retirement budget so you can give every one of your hard-earned dollars a job.

- And don’t forget, if you need help planning for retirement, we can match you with an investment pro in your area for free through the SmartVestor program.

This article provides general guidelines about investing topics. Your situation may be unique. To discuss a plan for your situation, connect with a SmartVestor Pro. Ramsey Solutions is a paid, non-client promoter of participating Pros.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.