7 Employee Retention Strategies Your Business Needs Right Now

By

By

Key Takeaways

- Employee retention—keeping great team members long term—starts the day someone is hired, not months or years later.

- The top reasons employees leave include burnout, lack of flexibility, limited growth, leadership issues and lifestyle changes.

- Warning signs like disengagement, low morale and reduced productivity indicate it’s time to lead and support—not micromanage or replace.

- Retention strategies include internal promotions, competitive pay, meaningful benefits, regular recognition and building trust.

- Financial wellness benefits like SmartDollar empower employees to manage money well—boosting morale and improving retention.

“I don’t understand why our retention rates are so low . . . we give them challenging, important work, and we let them do it for 40 hours a week.” Sound familiar? Maybe you’ve heard something like that at work—or even thought it yourself.

Here’s the deal: Employee retention (aka keeping your people around) should be a top priority for every business leader. But too often, leaders don’t have a solid strategy to help team members actually want to stay.

If you take away just one thing from this article, let it be this: The best retention strategies start the moment you hire someone—not 90 days later and definitely not two years in.

Let’s dig into why employee retention matters and how you can build a strategy that strengthens your team and shapes your company culture.

What Is Employee Retention?

Employee retention refers to the steps a business takes to keep its employees around. When a good employee leaves and takes their skill set out the door with them, their institutional knowledge—everything they know about your company culture and how things work—is even harder to replace than their skills. That’s why it’s important for companies to have a practical, organized strategy that helps them reduce turnover while increasing productivity and profitability.

Why Would an Employee Leave?

The truth is, it’s impossible to have a 100% retention rate. But employees that leave a job fall into one of two big buckets: They’re going to something better (benefits, pay, title, etc.) or they’re getting away from something they don’t like at their current job. Your job is to know which one.

And within those two buckets are several reasons why someone might leave. Here are some of the biggest reasons employees give for changing jobs:

- They’re burned out.

- Their job lacks a flexible schedule.

- They have minimal growth opportunities.

- They’re experiencing a lifestyle change.

- They’re leaving their leaders.

Understanding why your employees may leave their job gives you a helpful perspective into what they’re thinking and feeling. That way, you can be proactive about addressing their needs instead of dealing with the fallout when they leave.

How Can You Tell When an Employee Is Ready to Leave?

Before we get into the details, let’s be crystal clear: This isn’t a witch-hunt. You’re not looking for employees who are slacking so you can fire them before they decide to leave on their own. A lot of the signs we’re talking about are actually opportunities to either help your employees or improve your business. Let’s take a look.

Lack of Engagement

Employees with low or no engagement at work have a hard time feeling passionate about their job. If you see a drop in an employee’s engagement, that’s an opportunity to lead them and help them find what they’re passionate about. If you have a different role in the company they can fully engage in, you both win!

No Longer a Culture Fit

If you’re noticing a team member’s personal values are clashing with the company culture, sit down with them to figure out why they’re struggling and how you can support them. Sometimes the best option is to set them free to find a workplace that aligns better with their values. But other times, their perspective might shine a light on issues the company can address.

Drop in Productivity

A worker’s productivity depends a lot on their engagement level. Low levels of productivity from employees who are capable of accomplishing more are a red flag you need to dig into. But keep in mind, productivity issues aren’t always a sign an employee is ready to leave their job. They could be experiencing a tough season in their personal life—and it’s important for you to know how to support them if that’s the real issue.

Lower Morale

Workplace morale refers to the way your employees think and feel about their job. You can get a good gauge on employee morale by listening to how your team members talk about work and how they behave while they’re at work.

Are they excited to come to work? Are they confident with a sense of purpose? Do they feel and act like they’re part of a team working for a company with a bright future?

If your employees’ words and actions don’t at least point in this direction, you’ve likely got a morale problem, and it’s time to dig deeper.

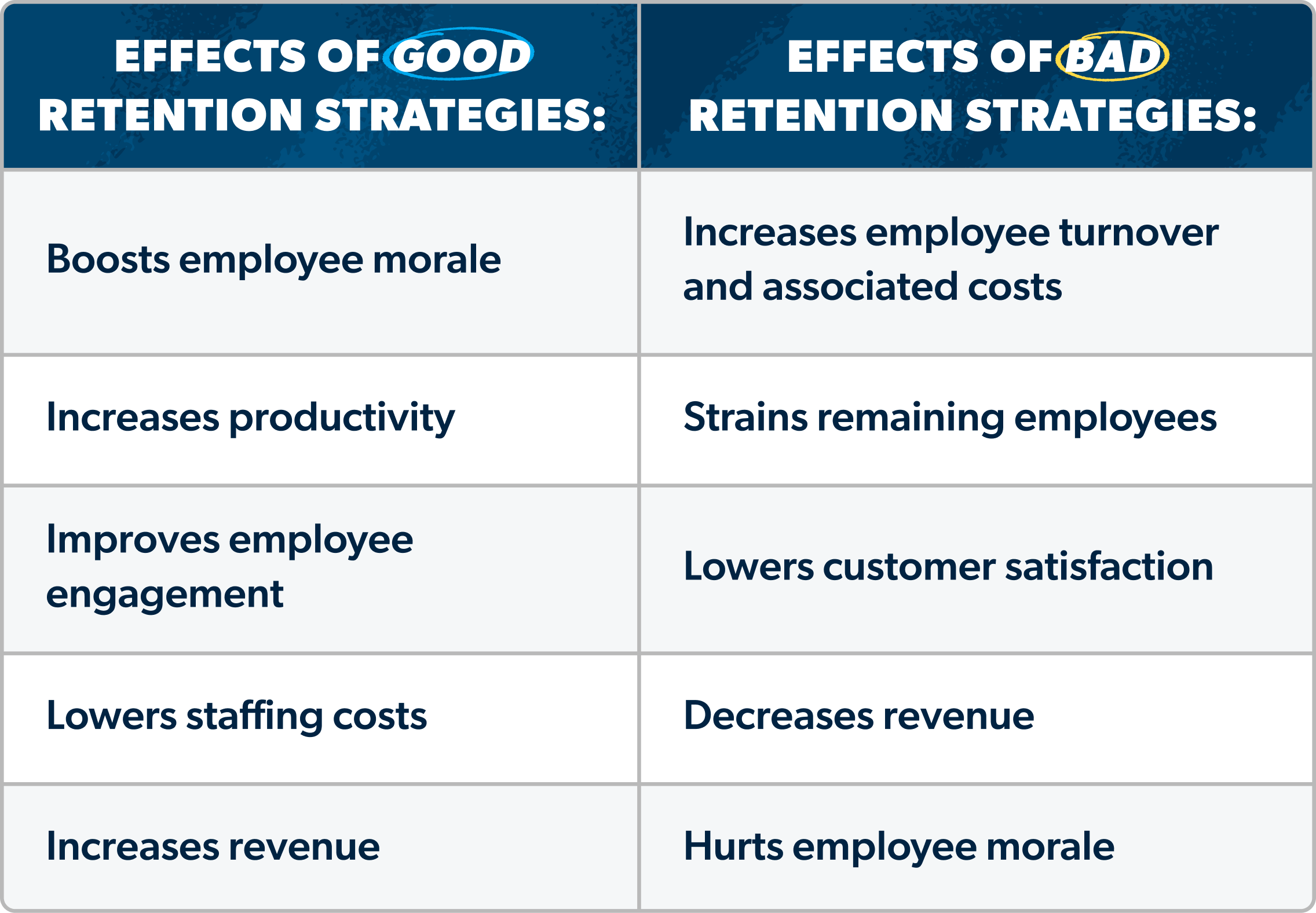

How Retention Affects Your Business

Replacing an employee costs anywhere from one-half to double that employee’s annual salary.1 So it’s easy to see how high turnover can impact a company’s bottom line. But that’s not all. Here’s a simple breakdown of how your retention strategies (good, bad or absent) can affect your business:

7 Employee Retention Strategies Your Business Needs Right Now

Retention doesn’t happen on its own. You have to want it, and you have to earn it! (Cue the motivational music.)

Here are seven employee retention strategies you can try with your business. Some you can start right away, while others might take a little more legwork to get going.

1. Prioritize internal hires over external hires.

It’s always best practice to look at your current team first when trying to fill a new role. You hired these people initially because they align with your company values, so it makes sense to invest in their growth. Employees need the opportunity to grow in their careers at your company if they’re going to stay long term.

Without a clear path to career growth, your employees will feel like their job is just a step along the way to their ideal landing spot—aka a job with another company.

2. Offer competitive pay.

Too many companies pay their employees below market value and wonder why they can’t keep them around. You can’t expect employees to feel great about working at your company if you pay them less than they can make somewhere else.

Take an honest look at your compensation and benefits and see how they stack up in your industry. If it’s not competitive, make a plan to get it that way—ASAP. And if it is competitive, great work! Stay on top by scheduling regular compensation studies for all your roles so you don’t fall behind the market.

3. Provide life-changing benefits.

The days of offering only the basic benefits are over. That won’t cut it anymore.

Here’s the truth: If you want to be competitive when it comes to both recruitment and retention, determine which benefits will impact your employees the most.

- Childcare benefits

- HSA company match

- Long-term disability insurance

- Paid sabbaticals

- Profit sharing

- Student loan repayment

- Tuition assistance

- 401(k) match

But no matter the benefits you offer, employees are always looking for help with their finances. The 2022 SmartDollar Employee Benefits Study found that 78% of employees believe it’s important for an employer to provide financial resources and tools, like a financial wellness benefit.

SmartDollar is a financial wellness benefit that teaches employees how to budget, get out of debt, save for the future, and retire with confidence. Talk about a life-changing benefit!

4. Show recognition.

Employees aren’t just workers—they’re people who need to feel appreciated. And let’s be clear: Incorporating meaningful recognition into your employee retention strategies means doing more than putting plaques up on the wall for employee of the month.

A lot of times, employees just want some good old-fashioned, genuine appreciation—in private conversation and in front of their peers. Even something as simple as finding out someone’s go-to coffee order is an easy way to brighten their day months down the line.

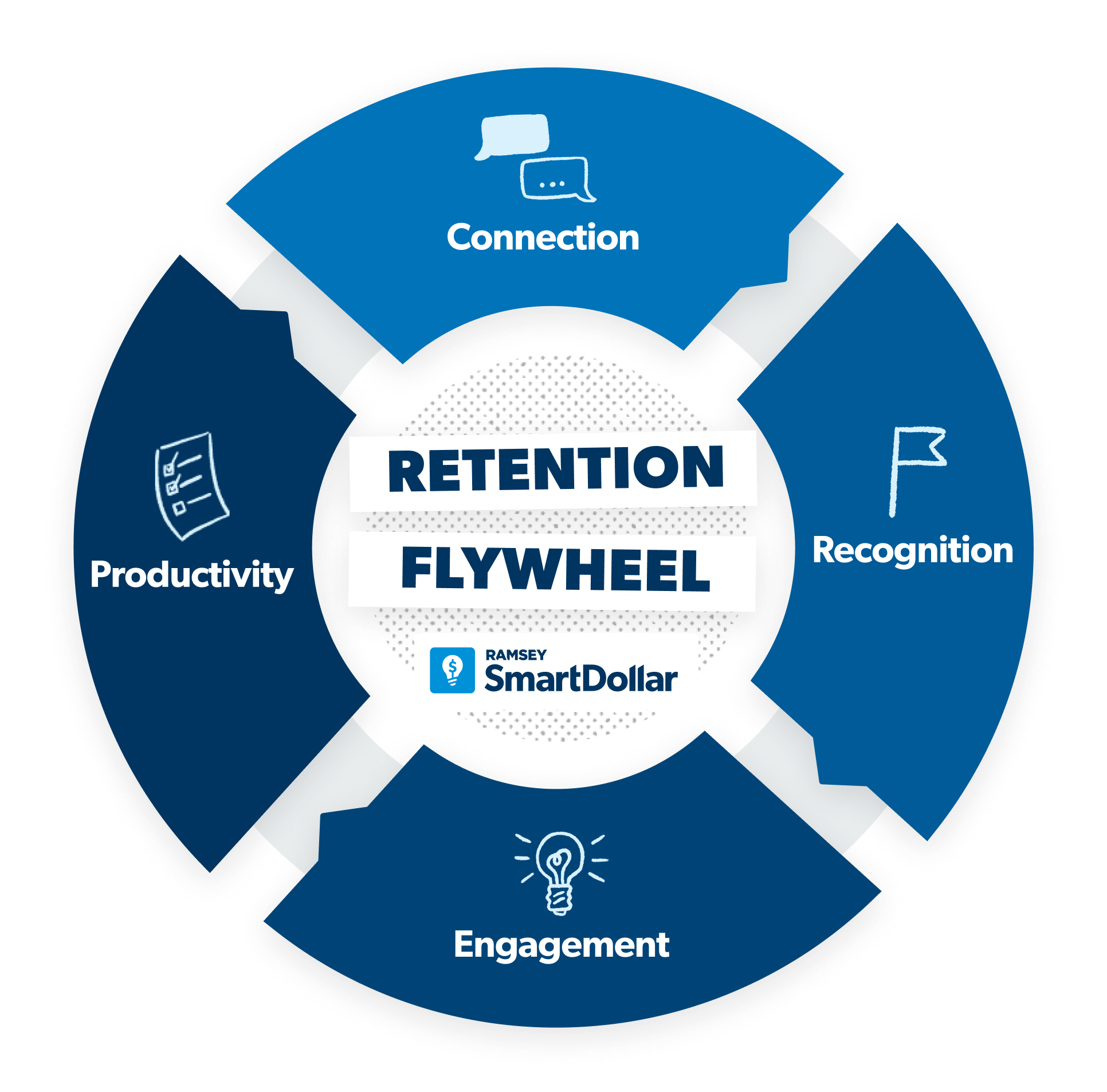

Recognition is an essential part of the retention flywheel, our tool for helping you keep great team members longer. So make it a habit. When employees know their contributions matter, engagement goes up, productivity improves, and retention gets stronger.

5. Support the work environment.

Employers are already comfortable supporting their on-site employees with the tools, training and one-on-one time they need to be successful. But now, hybrid and remote work employees are introducing new challenges to those tried-and-true methods. If you’re not careful, out of sight can turn into out of mind.

Here at Ramsey Solutions, we have everyone on-site. Even though this is what works best for our work environment, every company needs to decide what is best for their unique situation. Many companies have remote and hybrid employees. And those folks are just as interested in growing their careers and making a contribution to the business as on-site employees are. So whatever your work environment is, make it a top priority to find creative ways to support and engage those employees.

6. Conduct stay interviews.

Stay interviews are way more fun than exit interviews. Figure out what’s working for your employees and how you can improve. Don’t wait to dig into problems when people leave. Learn about them early so you can keep that from happening.

A stay interview can easily be an elevated one-on-one, like getting lunch or coffee. Here are some helpful questions to ask an employee during this time together:

- What’s important to you?

- What would it take for you to leave for another job?

- What can I do for you?

- What can I do to help you grow?

Your employees want to feel valued. And by taking this extra step, you show how much you care about your team.

7. Build trust.

Business moves at the speed of trust. And it’s a two-way street. You need to trust your employees, and they need to trust you. But it doesn’t happen overnight. Here are some good questions to ask yourself to see if you’re taking the right steps to build trust with your team:

- Do you set your employees up for success with the tools and training they need to do their jobs? Did you (or their leader) support them as they learned the ropes?

- Once they proved they were capable, did you set them free to do the work without micromanaging?

- Can your team trust that your yes is yes and your no is no?

- Are you honest with your team, even when it’s hard to tell the truth?

- Do you pour into your employees as individuals and get to know them and their families?

- Is your team bought in to your company mission? Do they understand how their work contributes to that mission?

If you can answer yes to all these questions, you’re well on your way to building a culture of trust—and that’s a culture employees will want to stick around for.

After You Hire an Employee . . .

Everything you do from day one shapes how long your team members stick around. That’s why it’s so important to start strong with a solid employee retention plan—one that’s built on real relationships, holistic benefits and support that goes beyond the job description.

One powerful way to do that? Offer a financial wellness benefit like SmartDollar. It gives your team the tools and coaching they need to take control of their money—without needing to switch jobs to find relief. When employees feel secure financially, they’re less stressed, more focused, and more likely to stay.

Visit SmartDollar to get started!

Next Steps

- Honestly evaluate where your company’s retention efforts stand today—look at your turnover, engagement and morale.

- Identify which retention strategies make the most sense for your team and take the first step toward implementing one this week.

- Sign up for SmartDollar to give your employees the financial tools they need to feel secure and stay long term.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.