What Is the Mortgage Interest Deduction? And How Does It Work?

By

By

If you’re on the hunt for a new home, we’ve got some good news and some bad news. Let’s get the bad news out of the way first. The days of super low mortgage rates are long gone, and they’re probably not coming back anytime soon.

But there is a little bit of good news that can soften the blow of higher mortgage rates—and that’s the fact that you can deduct your mortgage interest on your tax returns. That’s a huge deal, because your mortgage interest could lower your tax bill by hundreds or even thousands of dollars!

But how does this deduction work? And how can you take advantage of one of the biggest tax benefits that come with home ownership? Let’s dive into it.

What Is the Mortgage Interest Deduction?

A home mortgage interest deduction is a tax deduction that allows homeowners to lower their taxable income by the amount of interest they paid on their home loan during the year.1

You’re not going to hear us say this often without sarcasm, but . . . thanks, IRS. (Yuck, that felt wrong!)

But remember, you need to itemize your deductions on your tax return if you want to claim the mortgage interest deduction. If you take the standard deduction like most taxpayers do, then you won’t be able to claim most itemized deductions, which, you guessed it, includes mortgage interest.

How the Mortgage Interest Tax Deduction Works

In most cases, you can deduct all of your home mortgage interest. But how much mortgage interest you can write off depends on several different factors, including what you used the mortgage for, how big your mortgage is, and when you got the mortgage.

In most cases, interest on mortgage loans that you use to buy, build or improve your home qualify for the deduction.2 But there are some limits to this tax break.

The deduction is only available for interest paid on the first $750,000 of your mortgage debt. If you’re married filing separately, that limit drops to $375,000.3 If your mortgage is smaller than that, you’re good to go. But any interest paid on mortgage debt above that amount won’t be tax deductible.

However, if you bought a house with a mortgage before December 16, 2017, you can deduct interest on the first $1 million of the mortgage ($500,000 if you’re married filing separately).4 The Tax Cuts & Jobs Act lowered the deduction limit to where it stands now when it was signed into law on December 17, 2017, but mortgages taken out before then are grandfathered into the old deduction limit.

And if you took out a mortgage on or before October 13, 1987, you could deduct all of the interest you pay.5 But unless you have one of those crazy 50-year mortgages on your hands (yes, these loans that leave you with 600 months of monthly payments exist), this probably won’t apply to you.

Mortgage Interest Rate Deduction Example

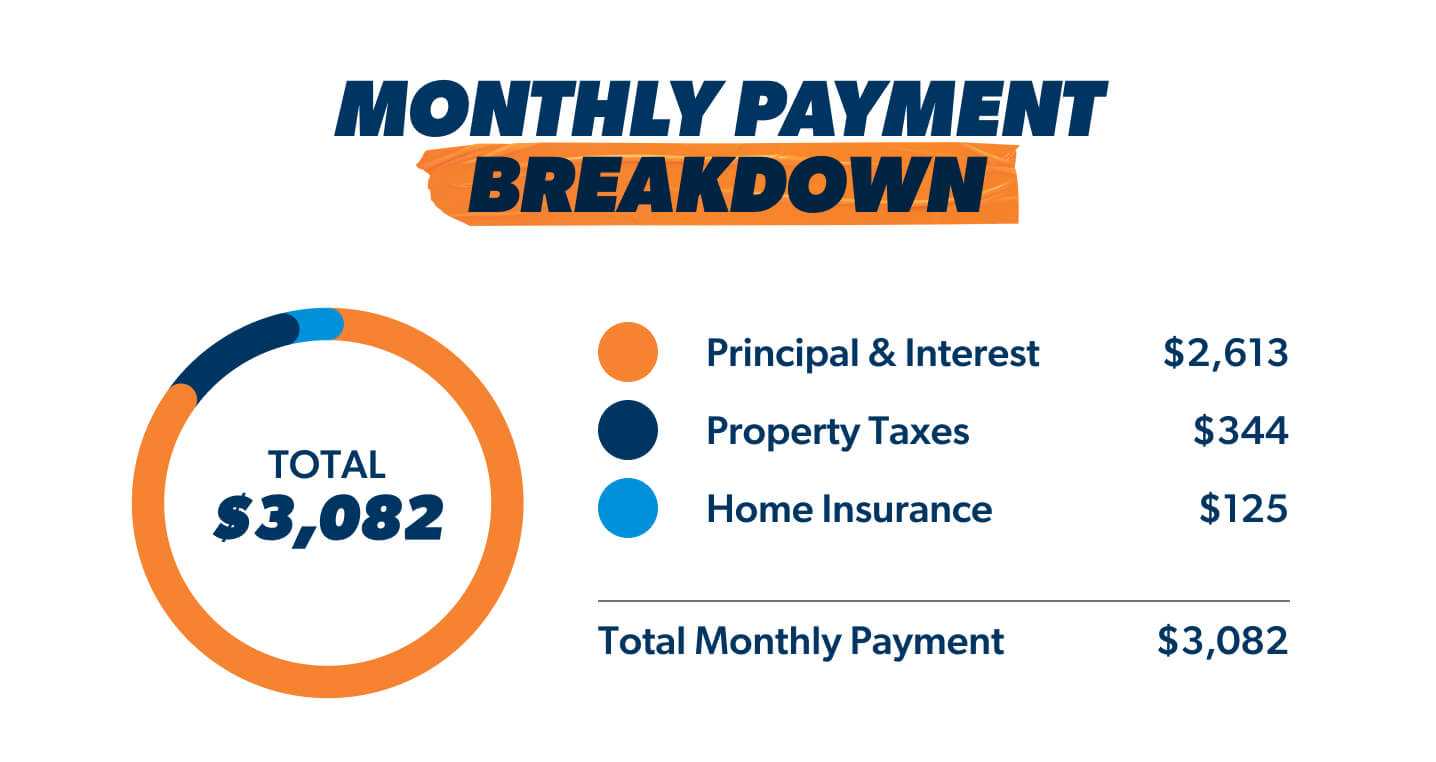

Let’s say that you bought a $375,000 house with a 20% down payment and 15-year mortgage loan (which is the only mortgage we recommend when buying a house). That means you took out a $300,000 mortgage at roughly a 6.5% interest rate, according to current interest rates.

Now, using our Mortgage Calculator, here’s how your monthly payment might break down:

For this exercise, let’s focus on the “principal and interest” portion of your monthly payment. The principal is the original chunk of money you borrow from your lender to buy a house, and part of your monthly payment goes toward paying off that amount. The interest is basically the amount the bank is charging you to borrow the money you needed to buy that house.

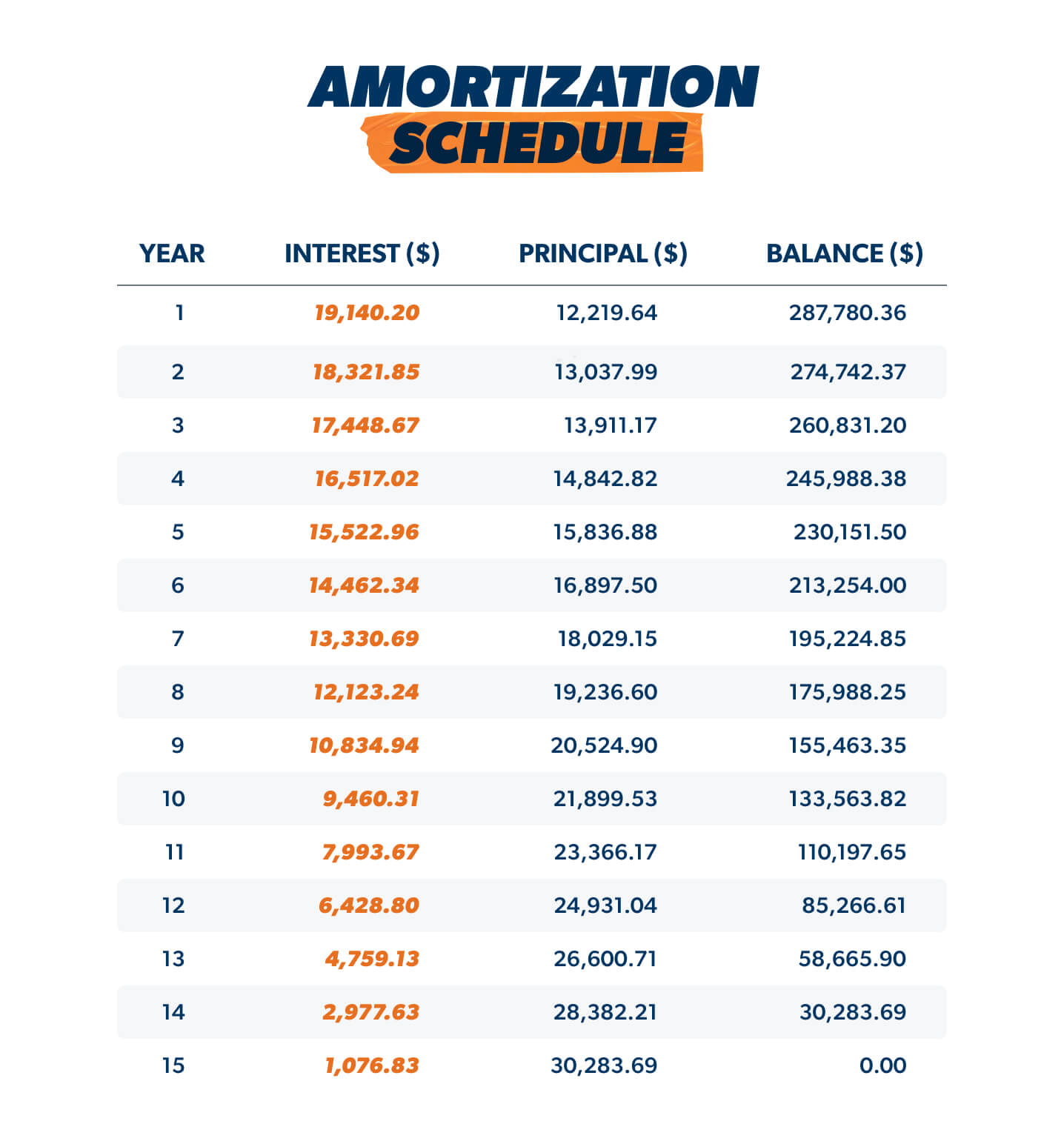

The way that these payments are set up is called an amortization schedule, which is essentially a countdown to the end of your mortgage. It shows you how much of each payment will go toward interest and principal—until you pay off the house!

At the beginning of the amortization schedule you’ll pay more in interest than on the principal. But as time goes by, you’ll start paying more toward the principal and less on interest.

As you can see, during the first year of your mortgage, you’ll pay $19,140 in mortgage interest. By the end of your mortgage term, that number will dwindle to less than $2,000 as more of your monthly payment goes toward paying down the principal (which also means a lower tax benefit).

And since your mortgage was used to buy your primary residence and is less than $750,000, you can deduct that entire amount from your taxable income as long as you itemize your deductions. Woo-hoo!

If you’re in the 32% tax bracket, that mortgage interest tax deduction alone would lower your tax bill by $6,124. Not a bad deal!

What Qualifies for a Mortgage Interest Deduction?

You can deduct your home mortgage interest if your mortgage is a “secured debt,” and your mortgage is a secured debt if you put your home up as collateral to protect the lender who loaned you the mortgage in the first place.6

Translation? If you can’t pay your mortgage for whatever reason, the lender can take back the house as payment for your mortgage debt.

Here’s a rundown of three common types of mortgage interest that qualify for the mortgage interest tax deduction.

Mortgages on Your Primary Residence and Second Home

The mortgage you took out to buy your main home—the one that you live in for most or all of the year—is eligible for the mortgage interest deduction.

But if you happen to have a mortgage on a second home—maybe a cabin in Wisconsin that you go to for summer family vacations or a beach house in Florida that you fly down to for the winter—then you can write off that mortgage interest on your tax returns too. That’s right—even if you don’t live there throughout the year, you can still get the tax break.7

But listen, it is never a good idea to buy a second home with a mortgage—especially if you have an existing mortgage or other debts. Whenever you buy real estate that’s not your primary home—like an investment property or a second home—you should always pay for it in cash.

Home Equity Loans and HELOCs

You can also deduct interest from things like home equity loans and home equity lines of credit (HELOCs) if they meet the “buy, build, improve” criteria above.8 But we have to stop for a minute and mention that those loans, also known as home acquisition debt, are a terrible idea.

Lots of folks take out home equity loans and HELOCs to renovate their homes or if they’re in a pinch and need cash. But both of those options come with a ton of risk, because if you miss multiple payments you could end up losing your house. Friends, no tax break is worth putting your home at risk. It’s okay to take advantage of the tax write off while you have the loans, but pay them off ASAP!

Mortgage Points

Mortgage points are the charges some borrowers pay to get a home mortgage at a lower interest rate by prepaying the mortgage. We’re not fans of mortgage points since most people don’t stay in their homes long enough to break even on the points. But if you already bought a home with points, you might be able to get some kind of tax break out of it.

They go by a bunch of different names—like origination points or discount points. But no matter what they’re called, you generally can’t deduct the full amount of points in the year you paid for them, but you still might be able to get a partial tax discount . . . so that’s something!

Because points are basically prepaid interest (meaning you are paying the interest up front), you can usually deduct them little by little over the life of your mortgage loan as long as the loan was used to buy, build, or improve your home.9

How to Claim the Mortgage Interest Deduction on Your Tax Return

Alright, now it’s time to find out how to claim all that mortgage interest on your tax return so you can save some money on Tax Day! Here’s a step-by-step process to help you get the mortgage interest tax deduction.

1. Itemize your deductions.

Like we mentioned earlier, since the mortgage interest deduction is an itemized deduction, you must choose to itemize your deductions if you want to claim it.

We’re going to shoot it to you straight: Most taxpayers are better off taking the standard deduction and calling it a day. But if you add up all your itemized deductions and the amount is greater than your standard deduction, then it’s worth taking that extra step to itemize!

2. Get your Form 1098 from your mortgage lender.

Around the end of January, your mailbox should start to fill up with tax forms from your employer, your bank, and anyone else who might owe you a tax form—that includes your mortgage lender.

You can expect your lender to send you a Form 1098 that gives you a rundown of the amount of mortgage interest you paid during the previous year.10 That’s the number you’ll usually be able to claim as a deduction on your tax return!

3. Enter the amount of mortgage interest on a Schedule A.

If you itemize deductions, you’ll need to report your mortgage interest on Schedule A (Form 1040)—that’s the form used to claim all your itemized deductions.11

On your Schedule A, you’ll enter the total amount of mortgage interest you paid during the tax year in the appropriate section. This amount should match the information provided on Form 1098.

4. File your tax return.

Once you’re done completing Schedule A and any other relevant tax forms, you’re ready to file your tax return with the IRS and be done with tax season. Hallelujah!

But before you shut down your laptop and forget about taxes until next year, make sure you keep a copy of any and all relevant tax documents (which includes Form 1098) for your records just in case the government comes looking for you to back up your mortgage interest claims.

Should I Keep The Mortgage Just for the “Tax Benefit”?

There’s this tax myth that you should not try to pay off your home faster (we call that Baby Step 6) because then you’d lose the “benefit” of being able to write off the mortgage interest.

Listen, while the mortgage interest tax deduction is a nice tax benefit that comes with homeownership, those tax savings don’t come close to matching the freedom of having a paid-for house. Let’s break this down.

Take the example above. You have a monthly mortgage payment (principal and interest only) of about $2,600 per month, and $1,600 of that is interest during that first year of the mortgage. That means you spent close to $19,200 in interest that year, which creates a tax deduction.

If, instead, you have a debt-free home, you’d lose the tax deduction . . . so the thinking goes that you should keep your mortgage for the tax advantages. This situation is an opportunity to find out if your tax professional can add.

If you’re in the 32% tax bracket, that $19,200 tax deduction during the first year of your mortgage (which is when this tax benefit is the largest, by the way) leads to about $6,120 in tax savings. According to the myth, we should send more than $19,000 in interest to the bank so we don’t have to pay $6,000 in taxes to the IRS. In what world does that math make sense?

Personally, we think it’s better to pay off that house and experience the joy and freedom of living completely debt-free.

Next Steps

- Want to secure a great rate on your next mortgage or refinance? Our friends at Churchill Mortgage can help give you a competitive edge on the market and find a great rate on your home.

- For those of you who want to tackle tax season yourself, check out Ramsey SmartTax. It’s an easy-to-use tax software that can show you how to claim your mortgage interest deduction and help you file your return with confidence.

- If your tax situation is a little more complicated than usual this tax season, ask a RamseyTrusted tax pro for help. They can walk you through all your tax deductions and credits so you don’t miss out on any tax savings.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.