Are Unemployment Benefits Taxable?

By

By

Key Takeaways

- The federal government treats unemployment benefits as taxable income, so you’ll likely owe federal income tax on any benefits you receive.

- Some states don’t tax unemployment benefits because they don’t tax income, and others offer an exemption. But in most states, unemployment benefits are taxed, so you’ll pay tax on part of your benefits.

- To help ease your tax burden, we recommend withholding taxes for your unemployment benefits from the get-go—because Uncle Sam always gets his share. Don’t make a hard season of life even harder by kicking the tax can down the road.

- If you’re unable to pay the taxes on your unemployment benefits, you can apply for a tax filing extension and/or sign up for a payment plan with the IRS.

- The best thing to do if you’re not sure how unemployment benefits will affect your taxes is to talk to a tax pro.

Listen, nobody wants to be on the receiving end of unemployment benefits. But if your company suddenly downsizes, a worldwide pandemic strikes, or AI renders your job “obsolete,” it’s nice to know there’s a safety net to catch you if you end up out of work.

At the beginning of September 2025, nearly 2 million Americans filed claims to receive unemployment benefits.1 So if that’s you, you’re not alone. But as Tax Day approaches, you’re probably wondering, Will I have to pay taxes on my unemployment benefits? Fear not. We’ve got the answers that can help you figure this thing out.

Let’s start with the basics.

Do I Have to Pay Federal Taxes on Unemployment Benefits?

Short answer? Yes. For the 2025 tax year, unemployment benefits are taxable.

Since the government considers unemployment benefits taxable income, you have to report them to the IRS just like any other taxable income. When you file your taxes, you’ll report unemployment income from IRS Form 1099-G showing the amount of unemployment benefits you received for the tax year.

Pro Tip: You have the option to make tax time less painful if you plan ahead with IRS Form W-4V, which allows tax withholding on your unemployment benefits. We’ll go into more detail on that in a sec.

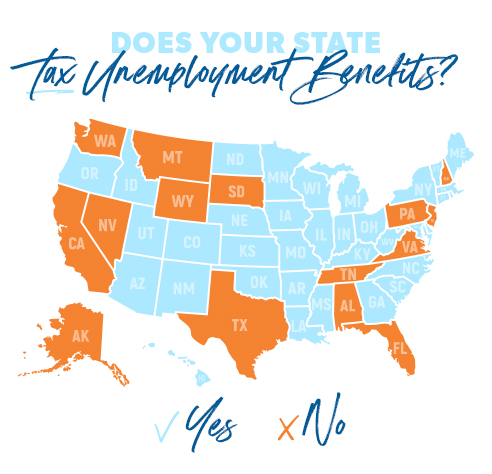

Do I Have to Pay State Income Taxes on Unemployment Benefits?

Unless you work in a state with no income tax or a state that makes an exception for unemployment benefits, your unemployment benefits will most likely be subject to state income taxes too.

Here’s a state-by-state breakdown of which states do—and don’t—tax unemployment benefits:

Who Is Eligible to Receive Unemployment Benefits?

Eligibility for unemployment benefits is determined by guidelines at the state level. In most states, you’ll qualify for unemployment benefits if you become “unemployed through no fault of your own.” That usually means there’s a lack of available work.2

If your job got cut in a round of layoffs or you resigned because of unsafe working conditions (restrictions apply here), you’ll probably qualify for unemployment benefits. But if you just decided to quit, you probably won’t qualify.

Some states also say you must have worked a certain amount of time at your last job or received a minimum amount of earnings from your previous employer to qualify for unemployment benefits. It all depends on where you live.

Pro Tip: Check with your state’s unemployment office to learn whether you’re eligible for unemployment benefits and to get more information about how those benefits will be taxed.

How Do I Pay Taxes on My Unemployment Benefits?

Now that we’ve covered the basics on how unemployment benefits are taxed, let’s look at your options for paying those taxes (when applicable). Here are a couple of options to consider:

- Withhold taxes from your unemployment benefits. When you sign up for unemployment benefits, you’ll fill out IRS Form W-4V. You’ll be able to choose to have 10% of each unemployment check withheld (you can’t withhold more or less) to help cover federal income taxes. You may still owe a little at tax time, but withholding may help reduce the size of your tax bill when tax season rolls around.

- Wait until tax season. If you’re currently unemployed, we get it—cash is tight until you land your next job, and you may decide not to opt for withholding. But our advice is to pay taxes on income as you go rather than wait till tax season to pay the whole bill at once. Procrastination has never been your friend, and that’s especially true whenever taxes are involved.

What if I Can’t Pay My Taxes?

Making every dollar count until you find a new job isn’t exactly a walk in the park. If you’re unable to pay your taxes (including taxes on your unemployment benefits) this year, don’t panic. Everything’s going to be okay as long as you keep communicating with the IRS.

The worst thing you can do is to try to ignore the problem by not filing a tax return or trying to hide from the government. Keep your chin up—you still have options if you owe and can’t pay.

First of all, even if you have to apply for an extension, you still need to file your return on time (if you don’t, you’ll get hit with a penalty). So even if you can’t pay a dime, file your tax return by the Tax Day deadline. And if there’s anything you can pay by the deadline, awesome. Pay that amount.

Next, contact the IRS about setting up a payment plan (they offer both short- and long-term plans).

If you’re waiting to start a new job in the next few weeks and can pay your taxes pretty soon, their short-term option offers a payment period of 120 days or less (as long as the total amount owed is less than $100,000).3

But if you’re not feeling great about your job prospects and you can’t pay the total amount of taxes owed that quickly, you could go with a long-term payment plan. It comes with a payment period longer than 120 days, but you must owe less than $50,000.4

Owing the IRS money while you’re still busy paying off debt can be really discouraging. What do you do? Simply add that tax payment to your debt snowball plan, but give the highest priority to knocking out what you owe the IRS first (no one wants the tax man on their back!). Then you can plow through your other debts, smallest to largest.

File Your Taxes With Confidence

If you’re stressing about how unemployment benefits affect your taxes—do you pay now, do you pay later, how much do you pay, how do you pay?—you can always reach out to a tax pro for help.

Nothing takes the stress out of Tax Day like having a tax advisor in your corner who eats, sleeps and breathes all this tax stuff on a daily basis. So if you still have questions about the taxes on your unemployment benefits, get in touch with a tax pro!

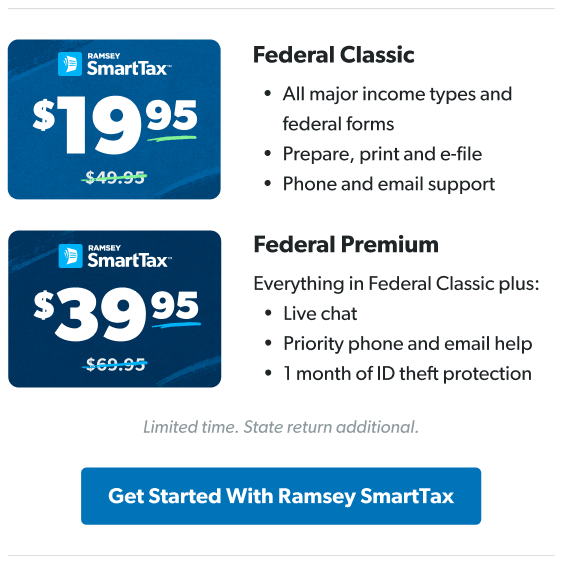

And if you’d rather file your taxes on your own, we’ve got you covered there too. Ramsey SmartTax makes filing your taxes easy.

File your taxes with Ramsey SmartTax today!

Next Steps

- Need a better idea of how much you’ll owe in taxes? Take a look at the latest federal tax brackets and tax rates to find out which tax bracket you’re in and calculate how much you’ll owe.

- If your situation seems complicated, you can always find a RamseyTrusted® tax pro to help you file your tax return. That way, you can have peace of mind and more time to do the stuff you want to do this spring.

- If you’re confident you can handle things on your own, check out Ramsey SmartTax. Our easy-to-use tax filing software will guide you through your tax return and help you claim all the deductions and credits you qualify for (so you won’t pay more than owe).

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.