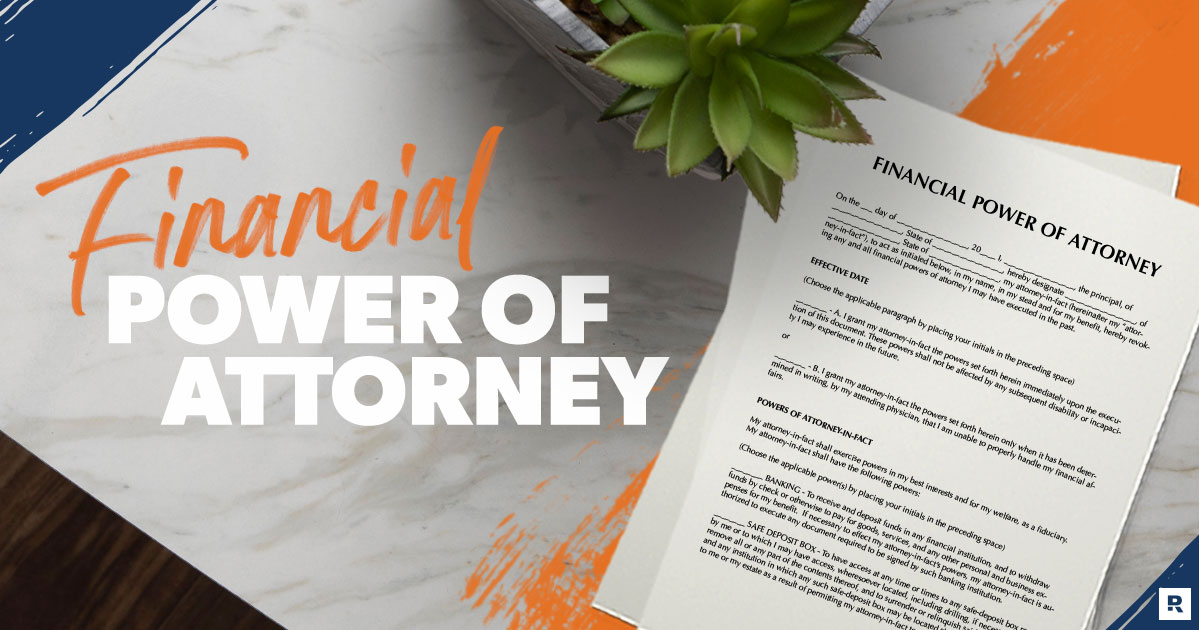

What Is a Financial Power of Attorney?

11 MIN READ | JUL 24, 2024

By

By

Sometimes legal terms sound like gobbledygook. But even though a financial power of attorney sounds like some tricky thing you’d read about in the fine print of a contract, it’s really simple. Let’s dig into the details so you can decide if you need one.

- What Is a Financial Power of Attorney?

- How Does a Financial Power of Attorney Work?

- When to Consider a Financial Power of Attorney

- When Does a Financial Power of Attorney Take Effect?

- When Does a Financial Power of Attorney End?

- What Your Financial Power of Attorney Agent Can Do

- How to Choose Your Agent

- Other Types of Power of Attorney

- How to Make Your Financial Power of Attorney Form

What Is a Financial Power of Attorney?

A financial power of attorney (POA) is a legal document that gives someone else the power to make money decisions for you. A financial POA is written specifically to let someone else act as your legal rep for financial matters.

Just like a medical power of attorney, the person who creates a financial POA is known as the principal—that’s you if you make one. No, being the principal doesn’t mean you’re putting anyone in detention—a financial POA principal is just the person whose money is being protected.

And the person you choose to do things with your money when you can’t do them yourself is known as the agent or attorney-in-fact. (In case you’re wondering, your agent does not have to be an attorney.) We’ll explain how to pick the right agent in a minute—for now though, let’s focus on how a financial POA works.

Don't Know Where to Start With a Will?

Download our will worksheet to get started.

How Does a Financial Power of Attorney Work?

A financial POA is most often used during a medical emergency. When you’re medically impaired, your daily financial needs might not be top of mind. But do those needs just disappear because you’re in a hospital bed? Of course not. Your bills still need to be paid and accounts need to be managed—like paying your rent or house payment and insurance premiums.

The key word here is financial. Just as a medical POA only applies to medical choices, a financial POA can only make money decisions if and when you’re unavailable to do so yourself.

Like most legal docs, the main purpose for creating a financial POA is to protect yourself and your family from a legal battle. In this case, the idea is to be sure there’s always someone trustworthy available to decide what should happen to your money.

When you’re out of commission, the last thing you want is someone you don’t know messing around with your financial future! But that’s exactly what can happen when you’re unavailable to make a decision about your money and don’t have a financial POA. At that point, going through courts to get control back might be unavoidable.

When to Consider a Financial Power of Attorney

You know that crystal ball some fortune tellers think can see into the future? Sorry, we wish it were reliable, but it’s not—there’s no way to predict when (or if) you’ll ever be incapacitated and need someone to manage your finances for you.

Our advice? Create your financial POA now. You can always adjust it as your life plays out. That way, all the bases are covered, and you’ve got what you need if you need it.

When Does a Financial Power of Attorney Take Effect?

It’s completely up to you when your financial POA becomes effective. It will depend on how you spell it out in your document. There are two ways to time this.

Effective Immediately

In this first case, the financial POA lets your agent act on your behalf even if you’re available and not incapacitated. (No, incapacitated doesn’t mean getting your head chopped off. It’s actually just a ten-dollar word for losing the power to tell people what you want to do.)

If you’re married, you’ll probably want your spouse to be able to make financial decisions if you face a medical emergency. In that case, making the document effective immediately is a smart move. In general, the more closely related the agent is, the more likely you would be to choose to have the POA effective immediately.

Making it immediately effective could also be a good option if you’re frequently on the road and you have lots of financial needs that require your official approval to get done. Or maybe you expect to be unavailable for a particular transaction that can’t wait for your return.

Tied to an Event

The second way to shape your financial POA is to specify that you only want it effective when an incapacitating event happens. This is known in the attorney world as a “springing power of attorney”—maybe because it kicks in when the principal has lost a spring in their step. Some of the certifiable conditions that could cause a financial POA to spring into effect include:

- Coma

- Onset of Alzheimer’s disease

- Mental illness

- An inability to communicate

When a financial POA is tied to an incapacitating event, your agent’s power is only effective when one or more doctors have certified that you’re physically or mentally unable to make decisions.

Thinking of naming one of your children or someone more distantly related to serve as your agent? Creating a springing power of attorney is a great option.

So, whether it’s effective immediately or tied to a potential future event, your agent only gets the power to handle your finances when you grant it. But when do they lose it?

Interested in learning more about estate planning?

Sign up to receive helpful guidance and tools.

When Does a Financial Power of Attorney End?

Good question! Several things can make a financial POA kaput:

- The death of the principal

- The principal choosing to revoke the power at any time

- A court ruling it invalid

- The principal’s agent becoming unable to fulfill their duties as financial POA (this can be avoided by naming a successor agent in the document)

- In some states, when the principal has both 1) named their spouse as the agent, and 2) later divorced their spouse

- And generally speaking, if the principal becomes incapacitated (unless the POA is worded to say that the agent’s authority should continue anyway)

Imagine this scenario. You fall into a coma and your family has a lot on their plate dealing with your affairs. Along with making heart-wrenching medical decisions, they also want to have say-so into your finances.

The great news is that you can write your financial POA specifically to say that your agent’s power continues even in the event of your incapacity. This is a type of POA known as a durable power of attorney (DFPOA), and it’s the kind of document Dave Ramsey recommends.

What Your Financial Power of Attorney Agent Can Do

As the principal, you have the power to grant your agent any financial privileges you wish. But you’ll want to think about the agent’s actual abilities and knowledge. In other words, your uncle the CPA may be a great candidate to handle paying your taxes, but don’t put him in charge of minding the family shop if he has zero business know-how.

Here are some of the powers you’re able to grant a financial POA agent to do for you:

- Collect retirement benefits

- Invest

- Log into financial accounts

- Manage real estate

- Operate a business

- Pay bills

- Pay medical expenses

- Pay taxes

- Purchase insurance

- Sell assets

It’s completely up to you how much authority you give your agent. You can give them total control of your finances or limit them to specific dates and/or transactions.

Okay, we need to state the obvious here. Your agent is required to act in your best interests, maintain accurate records, keep your property separate from his or hers, and avoid conflicts of interest.

How to Choose Your Agent

First let’s deal with the bare-minimum legal requirements. Your agent is required to be of sound mind and at least 18 years old. Yes, those rules eliminate tons of people. But you still need to narrow it down some more!

When it comes to picking someone to decide what should happen to your money, the main ingredient is trust. Family members can be great agents. They can also be disasters.

Before you give this job to your Aunt Gloria, maybe think about the fact that she’s always trying to borrow money from everyone in your family . . . so she’s probably not the best option for your financial POA. But there is your cousin Joe, who’s really good at helping everyone in your family find sweet deals on used cars. Yeah, Joe could be an awesome agent.

For many people, the obvious choice is their spouse. If either of you travel a lot for work, appointing the other as an agent in your financial POA makes a lot of sense.

Or maybe you know someone outside your family who just has good character and financial smarts. They’d also be an outstanding candidate. Either way, pick someone you’d be comfortable giving access to everything you’ve worked so hard to build over the years.

Other Types of Power of Attorney

A financial POA is just one type of POA. There are others, depending on the purpose:

Durable Power of Attorney

We touched on this phrase earlier—let’s dig deeper.

A durable power of attorney typically means that power of attorney rights are effective for the duration of the principal’s disability. That authority could end when the principal passes away or when the agent’s authority is revoked for some other reason.

But depending on where you live, durable power of attorney rules can differ on how long your agent’s authority is effective. Some states automatically consider all power of attorney documents to be durable, meaning that your agent’s authority to manage your financial affairs is automatically effective for the duration of your disability.

In other states however, if you want a durable power of attorney, you need to spell out the duration of your agent’s rights in the power of attorney document. If it’s not spelled out, as soon as your doctor declares that you’re unable to make decisions on your own, the rights of the financial POA are no longer valid.

Limited Power of Attorney

A limited POA is when the agent’s rights are (you guessed it) limited to certain financial decisions or one-time transactions. For example, you might have a limited POA to close a specific real estate deal for you. Or maybe you know you’ll be out of the country for the month of May, and you grant limited POA for that time period.

Medical Power of Attorney

A medical POA gives the agent authority to make important medical decisions about the principal's health care, especially when they become severely ill or incapacitated.

Now let’s go over the logistics of filling out a financial POA form.

How to Make Your Financial Power of Attorney Form

To be binding, a financial POA needs to be signed in front of a notary public. In some situations, the document may also require a witness at the time of signature. And in some states, the agent must sign to prove they accept the assignment.

In general, filling out your state’s official form is a good start to making a financial POA. But in order for your agent to conduct business on your behalf, keep in mind that some banks require you to use their own specific forms.

Similarly, some lenders, title insurance companies and closing agents have unique forms you must fill out before they’ll accept an agent’s actions. In the end, some people wind up with more than one financial POA. What a headache!

Do Yourself and Your Family a Favor

Nobody should be sticking their nose into your most important financial decisions unless you give them say-so. That’s why making your financial power of attorney along with your will is an essential step. It guarantees your hard-earned funds stay under your control (or someone you trust) at all times. We’ve put together a super easy bundle to give you peace of mind. Create your POA and will with RamseyTrusted provider Mama Bear Legal Forms!

Complete Last Will Package for Married Couples

Complete Last Will Package for Individuals

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.